Larry Summers: Advanced economies are sick. How can we fix them?

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

Economic Progress

This article is published in collaboration with Washington Post.

An e-book containing the papers and presentations from the European Central Bank’s central banking forum conference in Sintra, Portugal, is now available. ECB President Mario Draghi and his colleagues are to be greatly commended for running a forum that is so open to profound challenges to central banking orthodoxy.

The volume contains a paper by Olivier Blanchard, Eugenio Cerutti and me on hysteresis — and separately some of my reflections asserting the need for a new Keynesian economics that is more Keynesian and less new.

Here, I summarize these two papers.

Hysteresis effects

Blanchard, Cerutti and I look at a sample of over 100 recessions from industrial countries over the last 50 years and examine their impact on long-run output levels in an effort to understand what Blanchard and I had earlier called hysteresis effects. We find that in the vast majority of cases, output never returns to previous trends. Indeed, there appear to be more cases where recessions reduce the subsequent growth of output than where output returns to trend. In other words “super hysteresis,” to use Larry Ball’s term, is more frequent than “no hysteresis.”

This finding does not in-and-of-itself establish the importance of hysteresis effects. It might be that when underlying growth rates fall, recessions follow, but that recessions have no causal impact going forward. In order to address this issue, we look at the impact of recessions with different precursors. We find that even recessions that are associated with disinflationary monetary policies or the drying up of credit have substantial long-run output effects suggesting the presence of hysteresis effects.

In subsequent work, Antonio Fatas and I have looked at the impact of fiscal policy surprises on long-run output and long-run output forecasts, using a methodology pioneered by Blanchard and Daniel Leigh. Because fiscal policy effects operate primarily through aggregate demand, this provides a way to avoid the causation question. We find that fiscal policy changes have large continuing effects on levels of output suggesting the importance of hysteresis.

I was struck that in a vote taken at the conference, close to 90 percent of the participants indicated that they believe there are significant hysteresis effects. While there is much more work to be done, I believe that, as of right now, the right presumption is in favor of hysteresis effects, despite their exclusion from the standard models used in almost all central banks.

Toward a new macroeconomics

My separate comments in the volume develop an idea I have pushed with little success for a long time. Standard new Keynesian macroeconomics essentially abstracts away from most of what is important in macroeconomics. To an even greater extent, this is true of the dynamic stochastic general equilibrium (DSGE) models that are the workhorse of central bank staffs and much practically oriented academic work.

Why? New Keynesian models imply that stabilization policies cannot affect the average level of output over time and that the only effect policy can have is on the amplitude of economic fluctuations, not on the level of output. This assumption is problematic at a number of levels.

First, if stabilization policies cannot affect average levels of employment and output over time, they are not nearly as important as if they can. Beginning the study of stabilization with this assumption takes away much of the motivation for doing macroeconomics.

Second, the assumption is close to absurd. It is surely reasonable to assume that better policy could have avoided the Depression or the huge output losses associated with the financial crisis without having shaved off some previous or subsequent peak.

Third, contrary to the now common view that macroeconomics is best understood by studying the stochastic properties of stationary time series, the most important macroeconomic events are in some sense one off. Think of the Depression or the Great Recession or the high inflation of the 1970s.

The problem has always been that it is difficult to beat something with nothing. This may be changing as topics like hysteresis, secular stagnation, and multiple equilibrium are getting more and more attention.

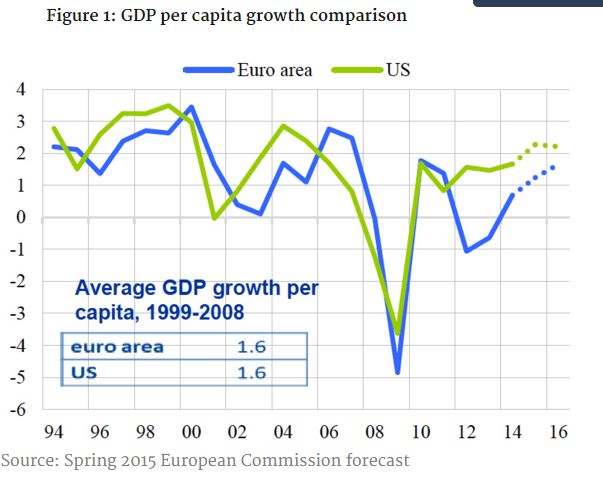

As well they should. U.S. output is now about 10 percent below a trend estimated through 2007. If one attributes even half of this figure to the effects of recession and assumes no catch up on this component until 2030, the cost of the financial crisis in the U.S. is about one year’s gross domestic product. And matters are worse in the rest of the industrial world.

As macroeconomics was transformed in response to the Depression of the 1930s and the inflation of the 1970s, another 40 years later it should again be transformed in response to stagnation in the industrial world.

Maybe we can call it the Keynesian New Economics.

Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Lawrence H. Summers is the Charles W. Eliot university professor at Harvard.

Image: A man walks past buildings at a central business district. REUTERS/Nicky Loh.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on Economic ProgressSee all

Joe Myers

April 19, 2024

Joe Myers

April 12, 2024

Joe Myers

April 5, 2024

Pooja Chhabria

March 28, 2024

Kate Whiting

March 28, 2024

Joe Myers

March 28, 2024