You’ll probably live to be 100. Here’s how you need to prepare for it

Image: REUTERS/Brendan McDermid

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

Values

Ageing is a key topic at this year's World Economic Forum Annual Meeting. Watch the Raising Life Expectancy and Expectations session here.

Here’s a shocking insight: we’ll all live 100 years, and we’re not at all prepared for it.

That is, in a nutshell, the message of Lynda Gratton and Andrew Scott of the London Business School in their new book, The 100 year life. But there’s a silver lining, too. If you change your lifestyle now, you’re likely to live a happy century after all.

So what do we need to do?

First, let’s see why the authors think we’ll all live 100 years. The answer is pretty simple, actually: statistics and medical progress.

At the outset, it appears as though they have their statistics wrong. Today, the official average life expectancy of a newborn is around 80 years in most Western countries, not 100. But there is a catch to this statistic: it is only valid “if prevailing patterns of mortality at the time of its birth were to stay the same throughout its life”. And they don’t.

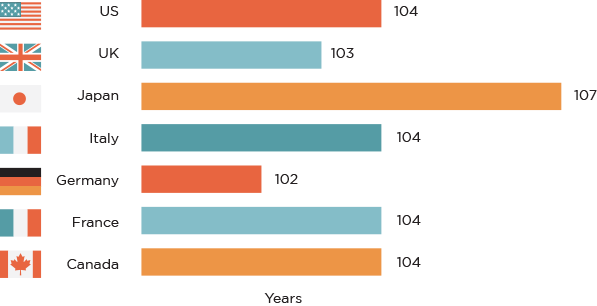

On average, people today die when they’re about 80. Thirty years ago, the average person died at 74. Sixty years ago, it was 66. And 100 years ago, the average person died at 56. Extrapolating that growth to the future would mean that people born today will die at an average of 104. And most of us who are in our twenties or thirties today would still reach an average of 100 years.

Source: Human Mortality Database

There are medical reasons for a 100-year life, too. The progress we have made in the past 50 years in healthcare is mind-blowing. Diseases that were prevalent 100 years, such as TB, are all but eradicated. The same is bound to happen again. In the next decades, science will make huge leaps in the fight against diseases like cancer, dementia and Alzheimer’s, which are a major cause of death today still. Once that barrier is removed, there is virtually no reason to assume we would not all live to 100.

That brings us to the next question: are we prepared for this longevity?

The answer is sadly no. Most of us today live as if we’ll retire at 60 and die at 80. We put in long hours at work, take too little vacation time, and often get sick as a result, either physically or mentally. We assume the government will pay our pension, as it has for our parents and grandparents. And we simply don’t think about what life will be like when we’re older, when someone will probably need to take care of us.

It is a naïve and even dangerous lifestyle. The reality is that we’ll likely have to work until we’re 80, rather than 60. We’ll have to pay for our own retirement, as the government will be broke long before we’re retired. And if we keep ignoring our duties as parents and friends, it is very likely we’ll be by ourselves just at the time we need company the most.

So, how should we live our life instead?

The most important things, the authors say, is that we shouldn’t look at those extra 20 years as simply being added at the end of our life. We should look at them as if they were an extra day every week, or an extra 3-4 hours every day. We should, in other words, change the pace of our life today.

In terms of work, we should consider alternating years of high-intensity work with periods of low-intensity work or even sabbaticals. This way, we’ll have more mental freshness to keep on working for 60, rather than 40 years.

In terms of finances, we should set aside a far larger chunk of our earnings than we currently do. Saving 30% of our income should be the standard, not 10% or 20%. We should rely on our personal savings and investments, rather than those provided by the state.

And in terms of relationships, we should spend more time with our family and friends, realizing we – and they – will be around for much longer than we anticipated. We need to invest in our relationships, because they will last longer than we thought possible.

Some years ago, the Colombian writer Gabriel Garcia Marquez won the Nobel Prize for his book 100 Years of Solitude. It was praised for introducing the genre of magical realism, or the appearance that the story was real, while it was a complete fantasy. Today, though, we know that living to 100 will no longer be a fantasy. It is up to us to not make it solitary, either.

The 100-Year Life, Living and Working in an Age of Longevity, by Andrew Scott and Lynda Gratton, is on sale now. This post is part of a leadership series from the World Economic Forum's Global Leadership Fellows programme.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on Health and Healthcare SystemsSee all

Katherine Klemperer and Anthony McDonnell

April 25, 2024

Vincenzo Ventricelli

April 25, 2024

Shyam Bishen

April 24, 2024

Shyam Bishen and Annika Green

April 22, 2024

Johnny Wood

April 17, 2024