Portugal's economy has turned a corner. This is how it happened

Portugal has experienced a true economic rebirth. Image: REUTERS/Rafael Marchante Picture Supplied by Action Images

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

European Union

In the run-up to introduction of the euro in 2002, perceptions about Portugal’s economic prospects and investment risk changed, resulting in a substantial increase in private debt and a mild domestic demand-led boom. The boom gave way, in the 2000s, to a decade of protracted growth, worsening labour market conditions, steady accumulation of external imbalances, and rising debt. Since then, the Global Crisis and the European sovereign debt crisis conspired to push the economy into a severe recession and led the country to embark on an adjustment programme overseen by a troika of creditors.

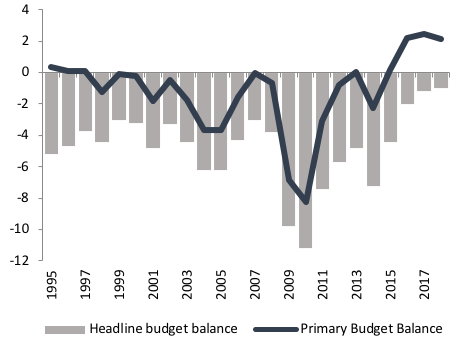

GDP fell 7.9% from peak to trough, while employment declined 13.4% (Figure 1). Unemployment peaked at 17.5% in 2013 (youth unemployment hit 40%). Fiscal deficits rose to around 10% of GDP (Figure 2). Portuguese sovereign bonds were downgraded to ‘junk’. Nearly 500,000 people emigrated between 2011 and 2014 – the largest emigration the country had experienced in 50 years.

Figure 1 GDP growth and unemployment

Figure 2 Budget balance (% GDP)

Early signs of recovery in 2014 and 2015 turned out to be feeble and short-lived. Growth would eventually pick up with renewed strength in 2016Q3, and accelerated further to 2.7% in 2017 (Figure 1) on the back of a 9% real increase in investment and 7.9% growth in exports. Employment rose 3.5% in 2017Q4 (year-on-year), while unemployment receded to 7.4% by 2018, its lowest level since 2004, and the labour force resumed an expansionary trend. This is now a sustainable recovery.

Fiscal deficits plunged to 2% of GDP in 2016, and 0.9% in 2017, the lowest in Portugal’s democratic history. In structural terms, this implied a reduction of 1.4 percentage points in two years, above what is envisaged in the Stability and Growth Pact. The stock of public debt fell 4.3 percentage points in 2017, the most significant drop in 20 years, while private sector debt (i.e. for non-financial corporates and households) declined to 163.5% of GDP, down from a peak of 210.3% in 2012.

Against this backdrop, the performance of the Portuguese economy in the last two decades is often framed as a process of steady deterioration of price competitiveness and accumulation of imbalances, culminating in a severe recession and a regenerative adjustment programme (Chen et al. 2012, ESM 2017, IMF 2017, European Commission 2016). According to this view, the adjustment programme set in motion a domestic deflationary process that helped restore external competitiveness and, thus, improve economic performance. These improvements, together with tail winds from a synchronised recovery in the euro area, would go a long way in explaining Portugal’s current macroeconomic performance, including the rebalancing of its public finances.

We argue this view is fundamentally at odds with existing empirical evidence on the fundamentals of the Portuguese economy and how they have evolved over time (e.g. Gouveia and Coelho 2018). In our view, Portugal’s turnaround is not a simple by-product of a purportedly competitiveness-enhancing adjustment programme, let alone of the vagaries of the external macroeconomic environment. There were elements of the adjustment programme that played important roles, but they are not the be-all and end-all of Portugal’s turnaround.

The steady, solid recovery of the Portuguese economy is, in fact, grounded in lasting structural changes in skills, investment, export orientation, and in the labour market, spread across the last two decades. These changes have been supplemented by recent policy initiatives aimed at restoring business and consumer confidence, including measures to repair the Portuguese financial system, policies to support internal demand, and counter-cyclical, rigorous, and prudent management of the public finances. All together, they have made great strides in addressing key structural weaknesses in the Portuguese economy, and have thus helped lay the foundations for a more resilient and prosperous economy.

Two decades of structural changes

Let us look at the main features of the structural changes that have been taking place under the surface.

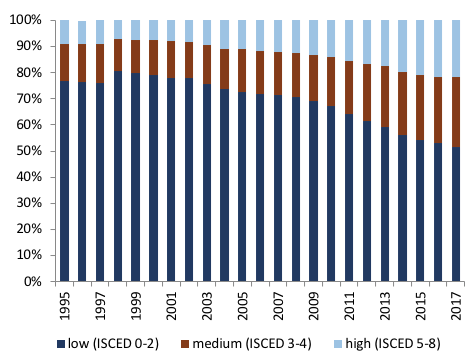

We start with human capital. While Portugal’s qualification gap vis-à-vis its European partners remains large (the stock of low skilled workers is 26 percentage points above the EU28), it is falling quickly (10 percentage points since 2004) and is largely related to the legacy of older generations with lower educational profiles (Figure 3). Between 2004 and 2016, the share of adults (15–64 years old) with at most lower secondary education decreased 21 percentage points (from 74% to 53%), while both medium- and high-skilled rose around 10 percentage points (from 16% to 26%, and from 11% to 22%, respectively). Assuming the current flow of the low-skilled into the labour force is kept constant (which is a relatively conservative assumption), one would expect the share of the low-skilled to reduce further from 53% to 42% in ten years’ time, and to boost potential GDP by around 7% (Gouveia and Coelho 2018).

Figure 3 Evolution of education levels

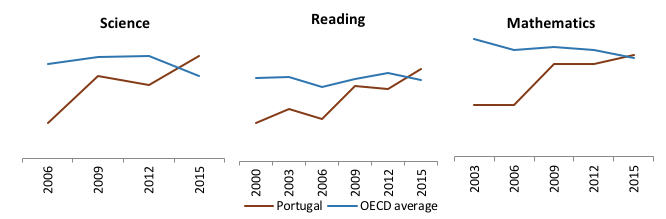

Changes in human capital have not been confined to quantity aspects, but have also included quality improvements. Portugal is part of a very small group of countries that have made steady, broad-based progress in the various rounds of the OECD PISA assessments (Figure 4). The results from the latest round (2015) place the country above the OECD average in all areas of assessment (science, reading, and mathematics). These indicators alone portray a society that has been able to cope with structural adjustment in an effective way. This stands in clear contrast to previous periods of structural change, such as that of the 1980s. In 1982 only 2% of private sector salaried workers had a college degree. This figure is now close to 20%. This signals a remarkable increase in skills, and an opportunity that cannot be missed.

Figure 4 PISA results

Moving on to investment. This was the main driver of labour productivity growth in Portugal in the decade before the crisis (e.g. Corrado et al.2016). Business investment, in particular, was systematically above the EU28 average (about 5 percentage points) throughout the 2000s (Figure 5). The crisis took its toll on investment, but there are clear signs that it is recovering well. Gross fixed capital formation increased 9% in real terms in 2017. Business investment is growing again above the EU average. A strong pipeline of EU co-funded investment projects for the next four years is expected to provide an additional boost to investment. These are mostly competiveness-enhancing projects, focused on transport infrastructure, urban regeneration, healthcare and education services, and R&D and innovation.

Figure 5 Gross investment rate of non-financial corporations, EU28 vs Portugal (4 year moving average, percentage of the sector’s gross value added)

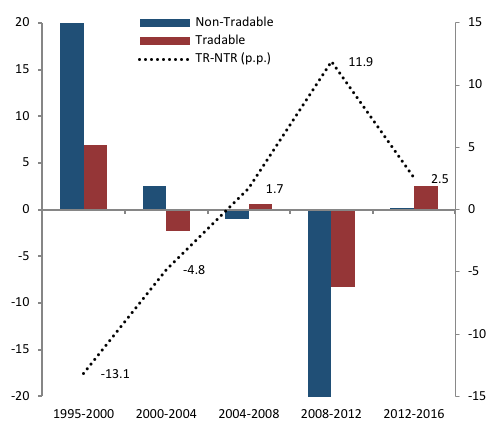

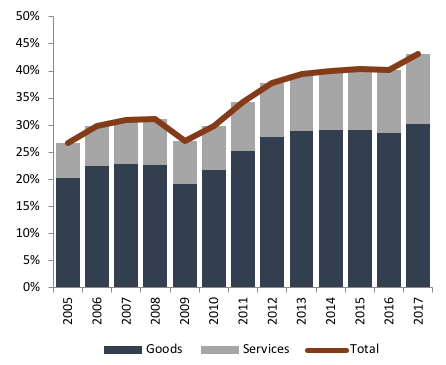

In the wake of the adoption of the euro, abundant capital inflows were channelled to relatively unproductive non-tradable projects, significantly harming economic performance (Dias et al. 2015). Yet, there are clear signs this pattern has reversed in the last decade (Figure 6). The weight of total exports in GDP increased 16 percentage points to 43%1 from 2005 to 2017 (Figure 7). This increase reflects a structural business restructuring process towards tradable sectors, which began well before the international financial crisis. Furthermore, it is largely unrelated to changes in price competitiveness. Real effective exchange rates increased from 1995 to around 2005, but remained fairly stable until recent years, when a slight decline became noticeable (Figure 9). This is in stark contrast to the conventional view discussed above.

Figure 6 Employment growth in Portugal, percentage and difference in percentage points

Figure 7 Nominal exports (% GDP)

Figure 8 Real export market share of goods (year-on-year, %)

Figure 9 Real effective exchange rates, export prices deflator (1995=100)

Portugal’s turnaround has also been supported by important changes introduced in employment legislation over the past 15 years. There have been multiple reforms that have targeted the internal flexibility of firms, such as the adjustment in hours worked, unemployment insurance, restrictions on firing, and the ability to sign temporary contracts, making the labour market more flexible and adaptable to shocks. In the 2001–07 period, worker flows in Portugal, including job creation and destruction rates, were remarkably close to those prevailing in the US. The same applies to wage flexibility. The Portuguese labour market has levels of wage flexibility similar to other advanced economies.

More recently, efforts made to stabilise the Portuguese banking system and reform its governance have played a critical role in restoring growth after the crisis. Strengthening the banking system was key to increasing credit flows and to improving the efficiency of capital allocation (Castro et al. 2004, Amador and Nagengast 2015). Those efforts included strengthening banks’ capital bases, changing shareholder structures, clarifying the mechanics for resolution procedures, and helping create appropriate conditions for bank’s operational results to return to positive ground.2 In 2017, the Portuguese banking system returned to positive results. Impairments costs and provisions declined sharply. Banks’ capital base improved (the Common Equity Tier 1 ratio stood at 13.9% at the end of 2017, 2.5 percentage points higher than at the end of 2016). The stock of non-performing loans (NPLs) fell from €50 billion in mid-2016 to € 37 billion in 2017. The NPL ratio is now at 13.3%, having dropped 3.9 percentage points from late 2016 and 4.6 percentage points from June 2016.

The crisis produced damaging effects on the public finances, which came on top of problems accumulated in the 2000s. Yet, Portugal has shown great resilience in the way it has committed to and persevered in restoring the balance of the public finances, through reforms designed to deliver structural fiscal consolidation. The current government’s strategy relies on rigorous, prudent management of public expenditure, able to respond flexibly and effectively to changes in the macroeconomic environment. It aims to strike the right balance between the debt-reduction goal and the need to protect growth. To improve public spending efficiency, the government has been conducting an expenditure review designed to help line ministries generate genuine, long-lasting efficiency gains that can work towards containing expenditure, while at the same time ensuring that inevitable demand pressures on public services can still be accommodated effectively within the existing fiscal envelope.

Challenges ahead

Portugal has turned a corner. Having gone through a mild boom, a slump, and a severe recession, all packed in less than two decades, the Portuguese economy has re-emerged with a newfound strength. Important challenges remain. Some are burdensome legacies from the crisis. The stocks of private and public debt are still high. Increased savings, both internal and external are required. Youth unemployment and long-term unemployment have not yet returned to pre-crisis levels. The financial sector still has some way to go on its way to full health. To keep the public finances on a consolidating trajectory, public expenditure will have to continue to be very carefully managed. Crucially, though, Portugal’s ability to rise to these challenges is considerably stronger today than at any time in the last few decades. The current combination of robust economic growth, powered by investment and exports, balanced external accounts, and public finances on a consolidating path, is a far cry from the experience of the late 1990s and 2000s, and bodes well for the performance of the Portuguese economy in incoming years. However, further reforms, demand, and patience are still of the essence.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on European UnionSee all

Kimberley Botwright and Spencer Feingold

March 27, 2024

Simon Torkington

February 8, 2024

Mirek Dušek and Andrew Caruana Galizia

January 17, 2024