How US firms are driving Europe’s economic growth

Trends in technology are highly dependent on use by large companies. Image: REUTERS/Denis Balibouse

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

Digital Communications

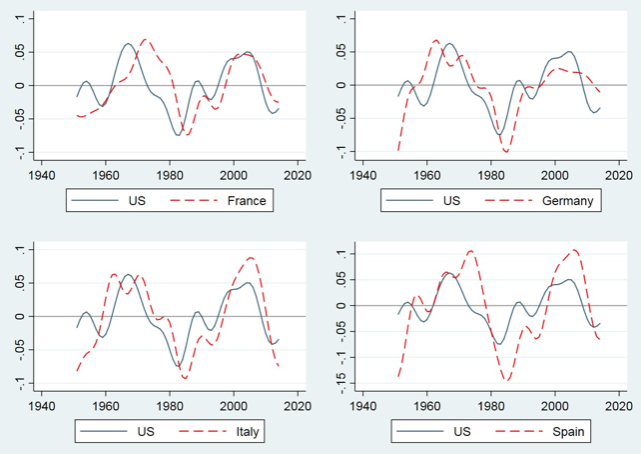

Since the end of WWII, advanced economies have experienced long-lasting swings in economic activity (e.g. Crafts and Toniolo 1996, Temin 2002). These swings have given rise to business cycles of stronger volatility and persistence than conventionally analysed. In a seminal contribution, Comin and Gertler (2006) characterise them for the US economy and term them “medium-term cycles”. In a recent paper (Correa-López and de Blas 2018), we take a closer look at the historical data, uncovering that, over the medium term, output and investment fluctuations among European countries have been even more volatile and persistent than in the US. In addition, US output, investment, and embodied productivity1 show a lead and a strong correlation with, respectively, European output, investment, and embodied productivity at medium frequencies, as Figure 1 illustrates. To understand what drives such co-movements, we present evidence of international diffusion of US technologies via trade. Furthermore, we show that larger US firms may play a significant role in explaining the observed cross-country aggregate patterns through their relevance in trade. Building on Comin and Gertler (2006), we develop a quantitative macroeconomic model of two advanced economies in an attempt to match the stylised facts found in the data.

Figure 1 Medium frequency component of GDP per working age population

Note: Using the band-pass filter to extract the medium frequency component, the vertical axis measures the percent deviation, in unitary terms, of output per capita from trend.

Stylised features of international medium-term co-movement

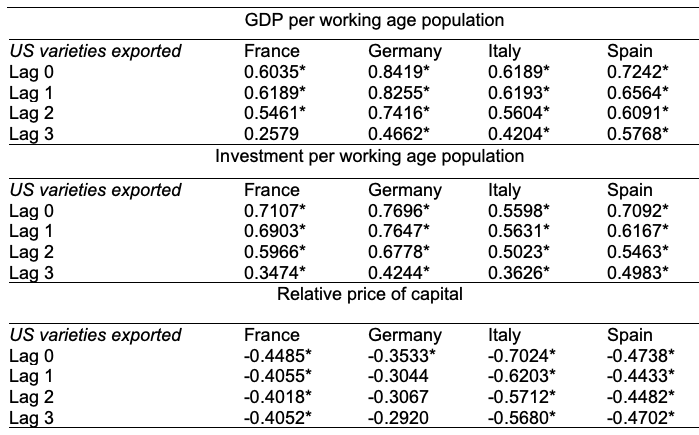

The international medium-term co-movement pattern identified is suggestive of an important role for persistent US shocks in generating medium term fluctuations across the advanced world. In particular, at the medium frequency, US R&D spending and patents lead and strongly correlate with the output and investment cycles of Europe. Furthermore, there are strong medium frequency co-movements between, on the one hand, the volume of bilateral exports and the number of intermediate varieties exported from the US and, on the other, the output and investment cycles of its main European trading partners, as illustrated in Table 1. The medium frequency fluctuations in US bilateral trade variables display a small lead over Europe’s medium-term cycle, suggesting that, once exported, these technologies diffuse rapidly in advanced economies.

Table 1 Number of varieties traded and the European medium-term cycle

Note: Correlation coefficients in the medium-frequency component. Varieties are measured as the non-filtered number of SITC rev. 2 categories up to the 5-digit disaggregation in manufacturing (excl. consumption goods) with a traded value greater than $1m as reported by the importer. Correlations are computed for 1980-2014 and their significance is reported at the 5% level.

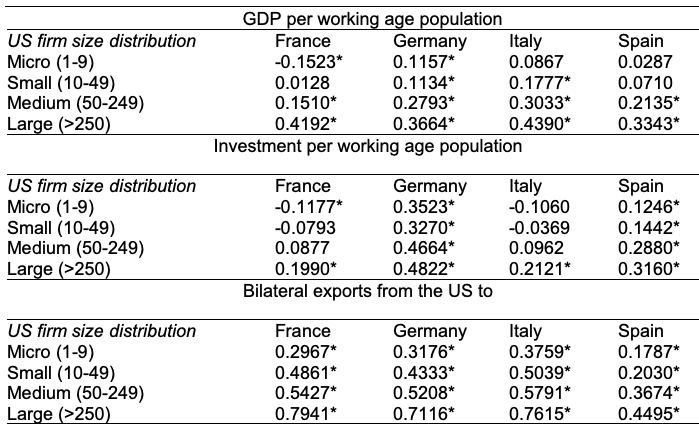

Importantly, it appears that large firms affect the transmission of US technology cycles. The evidence presented in Table 2 shows that fluctuations in size of medium and large firms are significantly more correlated with the European output and investment cycles than fluctuations in size of smaller firms over the medium term. In addition, medium-sized and, especially, large manufacturing firms in the US drive the medium-term cycle of US bilateral exports, placing them at the forefront of international technology diffusion.

Table 2 US manufacturing firm size and the European medium-term cycle

Note: Size is proxied by the number of employees (i.e. micro firms are those with 1 to 9 employees and so on). Period 1977-2014. Contemporaneous correlation coefficients in the medium-frequency component, where significance is reported at the 5% level.

Taken together, the evidence suggests that larger US firms, by diffusing embodied technology through trade in manufacturing intermediates, may determine Europe’s output at relatively low frequencies. These stylised features reinforce the importance of exploring the role of firm heterogeneity in the international transmission of shocks via traded intermediates in the capital goods sector, a key driver of embodied growth.

The model

To account for this evidence, in our paper we propose a two-country, asymmetric macroeconomic model with three distinctive elements. First, endogenous growth is driven by embodied technical change in new intermediate varieties for the capital goods sector (e.g. Romer 1990, Comin and Gertler 2006). Second, there is cross-country firm heterogeneity in the production of such intermediates (e.g. Melitz 2003, Ghironi and Melitz 2005). And third, countries trade in varieties (e.g. Comin et al. 2014, Santacreu 2015). Newly developed intermediates in the capital goods sector are the result of innovation and adoption investments that both countries may undertake. Disembodied technical change in the production of final output is the second source of growth that, for simplicity, is exogenous.

The model introduces firm heterogeneity in the production of specialised intermediates adapting the framework pioneered in Melitz (2003), where firms differ in their productivity level and use labour in production. Productivity cut-offs respond to demand (negatively) and cost (positively) variables, and select firms into producing either for the domestic market or for both the domestic and the exporting markets. In turn, the domestic and the exporting productivity cut-offs determine the probability of exporting. Holding the other productivity cut-off constant, an increase in the domestic (exporting) one, increases (reduces) the probability of exporting. The number of varieties produced domestically together with the probability of exporting determine the number of traded intermediates. In a model of endogenous growth in varieties such as this, productivity cut-offs exhibit long-term dynamics associated to the steady-state growth rate of the economy and short- to medium-term dynamics of adjustment after exogenous disturbances. The latter turns out to be critical for the international transmission of shocks.

Calibration and balanced growth

The model is calibrated for two advanced economies, where the US features as the leader, and its dynamic response assessed after embodied and disembodied technological disturbances, often considered the main drivers of short-term fluctuations (e.g. Backus et al. 1992, Fisher 2006). The benchmark calibration implies that 59% of growth in output per working age person in the long-run is explained by embodied technical change, and 41% by disembodied technical change, consistent with the quantitative evidence from steady-state US growth decompositions (Greenwood et al. 1997, Cummins and Violante 2002).

Macroeconomic adjustment over the medium term

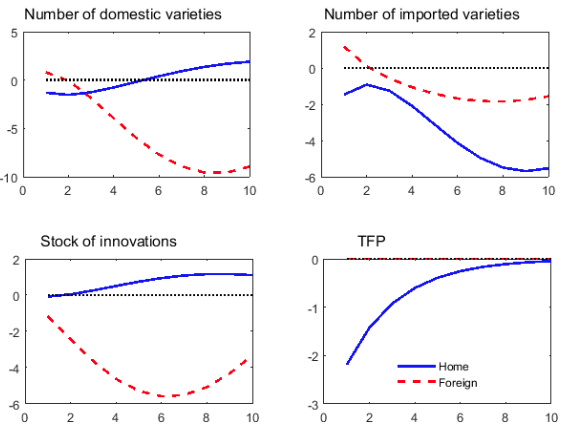

The model produces productivity cut-offs that vary noticeably across the ten-year horizon, countries, and shocks. Consider a negative TFP shock in the US. As the US real wage falls, the number of US varieties (or innovations) exported initially rises since some intermediate manufacturers, facing a domestic recession, become exporters. That is, the probability of exporting and the number of exported varieties by US firms increase. This adjustment turns out to be critical for the follower country. Newly imported varieties from the leader produce efficiency gains in the production of investment in the follower, which staves off the recession in the intermediate goods sector and redirects resources to domestic adoption. The latter, however, makes the recession in the follower economy very pronounced and, especially, persistent. The follower reduces investment on innovation substantially, prompting a large fall in the number of new domestic varieties that are, after all, the engine of recovery and future growth.

As shown in Figure 2, over time the US recession turns into a protracted foreign downturn, caused mostly by the long-lasting effects of lower embodied technology in the production of intermediates for the capital goods sector. All in all, the model predicts that trade, in quantities and varieties, stays below trend over a significantly long horizon.

Figure 2 Impulse response functions to a negative TFP shock in the leader economy (home)

Note: The solid (blue) line depicts the adjustment of the Home country (US) while the dashed (red) line depicts the adjustment of the Foreign country (Europe) to a negative TFP shock in the US. The magnitude of the responses is reported in percentage point deviations from the balanced growth path over a ten-year horizon

On the other hand, our framework produces a distinct US adjustment after an embodied technological disturbance. In particular, the model predicts that a negative investment-specific shock can impart a very prolonged recession in the US since the productivity cut-offs may fall below trend beyond the ten-year horizon. On this occasion, the domestic productivity slowdown is highly protracted due to the gradual adjustments of both the relative price of capital (persistently above baseline) and, especially, the real wage (persistently below baseline). The former supports investment activity in real terms, while the latter keeps exerting a downward pressure on costs, both allowing low productivity firms in manufacturing. This is suggestive of a protracted procyclical shift in the US firm productivity distribution occurring after a shock that directly impacts the investment sector, which may provide an additional explanation to the sustained productivity slowdown recorded in the US during the recent financial crisis (Reifschneider et al. 2015, Anzoategui et al. 2017).

Does the model fit the evidence?

The proposed model economy is simulated taking into account both types of technological shocks. Quantitatively, the framework outperforms standard international business cycle models in reproducing data-like cross-country correlations in most macroeconomic aggregates. Among the novelties, the simulations show that large US exporters contribute strongly to the dynamics of the follower's GDP and investment over the medium term. These findings are consistent with the empirical evidence. Given our ‘modelisation’ of trade in new intermediate varieties produced by heterogeneous firms as the link across countries, a policy lesson calls for reconsidering the medium-term effects of an excessive reduction in innovation spending after a slowdown.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on Equity, Diversity and InclusionSee all

Annamaria Lusardi and Andrea Sticha

April 24, 2024

Claude Dyer and Vidhi Bhatia

April 18, 2024

Julie Masiga

April 12, 2024

Alex Edmans

April 12, 2024

John Hope Bryant

April 11, 2024