What’s happening to EU inflation outside of the Eurozone?

Inflation has been falling sharply across Europe since 2012 (see Charts 1 and 2). Across Central and Eastern Europe (CEE), inflation expectations have also drifted down especially among countries who peg their currencies to the euro (Bulgaria, Croatia, as well as Lithuania, which adopted the euro on January 1, 2015), but also in those that target their inflation rate (the Czech Republic, Hungary, Poland, and Romania).

The recent drop in world oil prices has re-ignited the debate about good vs. bad disinflation. For the euro area, risks from low inflation have been discussed in the March 2014 iMFdirect post. Our blog examines the causes and potential consequences of falling inflation from the perspective of EU countries outside the euro zone.

Disinflationary dynamics

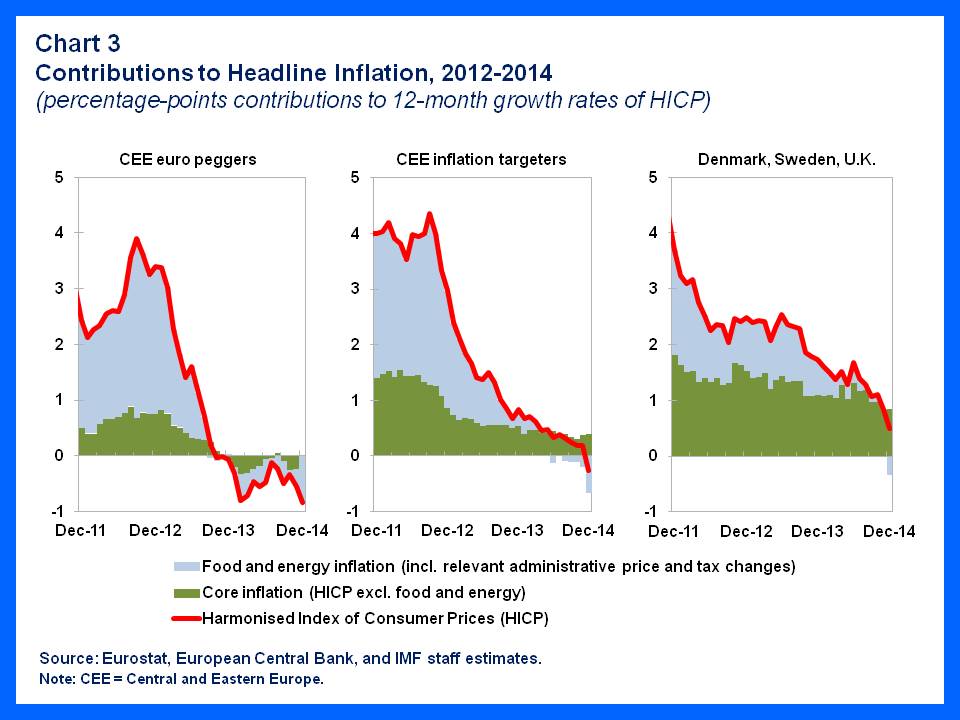

Falling world food and energy prices, and where relevant, cuts in administered prices of energy have been an important driver of disinflation across EU countries outside the euro zone (see Chart 3).

Furthermore, core inflation – overall inflation excluding the volatile food and energy prices – has also drifted down, tracing price trends in the euro area, and increasingly diverging from developments in the rest of the world (see Chart 4). This suggests possible disinflationary spillovers from the euro area to other EU countries, in light of their close trade links.

Our recent IMF Working Paper (Iossifov and Podpiera, 2014) confirms the dominant role of these factors (see Chart 5):

- Falling world food and energy prices and related cuts in administered prices account for the largest share of the inflation decline in non-euro area EU countries in Central and Eastern Europe.

- Falling euro area core inflation spills over through lower prices of imports to countries with currencies pegged to the euro and, to a smaller extent, to inflation targeters with higher foreign value-added content in domestic demand.

- In contrast, the domestic economic cycle – measured by the unemployment gap – has had a marginal impact in the recent disinflationary episode. In addition, the nominal effective exchange rate has been proportionately more important in inflation targeters.

Immediate gains, but medium-term costs

With rapidly falling world oil prices, disinflation pressures are unlikely to abate any time soon. According to the latest WEO forecasts and our estimates, headline inflation is expected to stay low through 2015 in euro peggers and remain below targets in Hungary, Poland, and Sweden.

In fact, the sharp decline in oil prices since June 2014 will drag inflation lower, as the commodity price drop filters through to domestic prices. Is this good or bad for the economy?

The prospect of lower cost-of-living and production costs is undoubtedly a positive development in the short-run:

- Lower energy prices boost the purchasing power of households and businesses. Given the still negative output gaps throughout the region, a pick-up in demand would be a boon for domestic producers.

- The lower consumer and firm outlays on goods and services would also ease the liquidity strains of debt service for heavily indebted firms and households, reducing the risk of default and the related negative effect on consumption and investment.

But, low inflation/deflation raises the possibility of “second-round” disinflationary effects in the medium-term that have proven difficult to reverse and this increases debt sustainability risks:

- The prospect of falling prices could suppress domestic demand, if it prompts households and firms to revise down expectations for wages and profits and thus to cut consumption and investment. These “second-round” disinflationary effects can trigger a self-feeding, vicious feedback loop between inflationary expectations and prices—a deflationary trap.

- Persistent disinflation and particularly deflation can complicate the process of deleveraging by heavily indebted firms and households, as it increases the real debt burden. This can be further exacerbated by stagnating nominal incomes, to the extent that the loss of income is not offset by the pass-through of lower inflation via nominal interest rates to debt servicing costs.

Policymakers’ predicament

Overall, the fall in oil prices will likely boost growth in the short-run. But, it poses challenges to monetary policy making, which focuses on medium-term risks. A prolonged undershooting of the inflation objective could damage central banks’ credibility, which would make it much harder to escape the deflation trap. What should policy makers do?

Countries that peg to the euro do not have independent monetary policies and would have to rely on the ECB’s quantitative easing (QE) policy response to persistently low inflation in the euro area. Where fiscal space allows, countries could also stimulate demand through fiscal policy.

Inflation-targeting central banks strive to keep inflation close to target over the medium-term. Consequently, when faced with renewed disinflationary pressures, they should aim at bringing inflation closer to its target, by stamping out “second-round” disinflationary effects of falling energy prices.

However, this could be challenging. With policy instruments at historical lows or at the zero lower bound, further easing by inflation-targeting central banks would need to weigh the benefits of normalizing price pressures with potential concerns about the impact on financial stability and capital flows and hence exchange rates. Easing monetary policy too much may prompt capital outflows and while this may help depreciate exchange rates and raise inflation, there is always a risk that the process may go too far. This is of particular concern for countries with high share of debt in foreign currencies, which are more exposed to changing investors’ risk appetite, geopolitical concerns, and global financing conditions. Fortunately, the recently announced QE by the ECB opens additional space for monetary easing by inflation-targeting central banks outside the eurozone.

On balance, the greater concern at present appears to be very low inflation and the possibility of sliding into a deflationary trap than financial instability on account of capital outflows, but policymakers will need to keep a watchful eye on markets.

This article is published in collaboration with IMF Direct. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Plamen Iossifov is a Senior Economist in the IMF’s European Department. Jiří Podpiera is an Economist in the IMF’s European Department.

Image: A worker adjusts a 150 metre-square European flag. REUTERS/Francois Lenoir – RTR1E8JX

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.