Why the panic over China’s markets?

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

Financial and Monetary Systems

What is currently happening in China is entirely predictable. I’m not referring to the bursting of the stockmarket bubble – this had to happen – but to China’s economic slowdown. The reasons behind China’s slowdown are many: the country has been moving up the value chain rapidly, the sources of productivity gains are drying up, the population is aging, and capital investment yields are falling. But whatever the chief cause, it suffices to look at empirical evidence to understand why the slowdown was bound to happen.

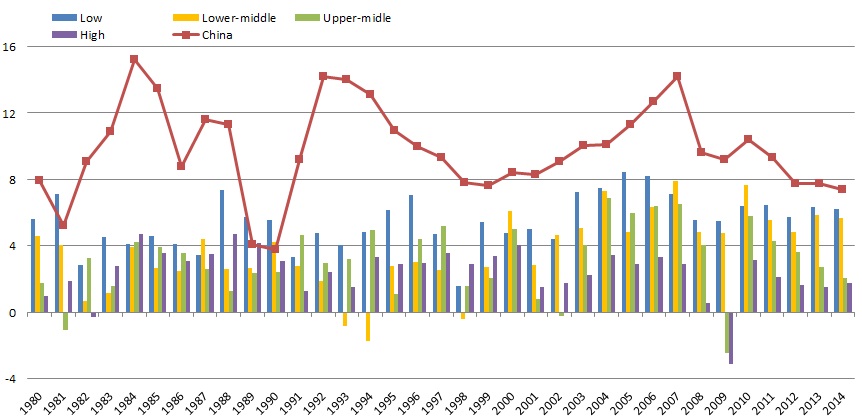

In the chart below, the red line depicts China’s annual real growth rate since 1980, which corresponds roughly to the beginning of market reforms in China. On the X- axis, the income group to which China belonged in each year (i.e. low in 1980-1996 and 1998; lower-middle in 1997 and 1999-2009; upper-middle since 2010). The green line reports the GDP-weighted real growth rate of that income group excluding China. Since 1991, China has outperformed the income group to which it belonged each and every year. For several years in the 1990s, the gap was almost 10 percentage points. Since being promoted to upper-middle status in 2010, the differential has been around 5 percentage points.

Figure 1: Real GDP growth (%)

Sources: Author’s calculations based on IMF and World Bank data

In light of this data, what is happening in China is not surprising: there are no upper-middle income countries growing at 7%-plus for more than a couple of years. And for those who have doubts about growth rates for China: even if Chinese or IMF figures had been overestimated by 100%, China would still have outperformed its income group peers in recent years.

Of course, some will say that because of China’s uniqueness, history is not a good indicator. China is indeed in uncharted territory. But sheer size should be an indication that double-digit growth cannot be sustained. Export-led growth that powered the development of Korea and other Asian Tigers and that of China until the early 2000s will not work now that China accounts for 16% of world GDP. The world’s capacity to absorb “made in China” products is limited. Even at its peak, Japan accounted for “only” 8%.

Despite the considerable challenges and uncertainties it faces, I do not believe in a hard landing for China – bar a cataclysm. The results of the The Global Competitiveness Report 2014-2015 reveal that the fundamentals of its economy are pretty strong and should prevent such a hard landing. But as China gets richer, its economy will grow more slowly. Just look at the chart below.

Figure 2: Growth (%) for China and income groups

Sources: Author’s calculations based on IMF and World Bank data

Have you read?

6 must-reads on the Chinese stockmarket slump

What was China’s aim in devaluing its currency

Author: Thierry Geiger, Head of Analytics and Quantitative Research, Global Competitiveness and Risks, World Economic Forum

Image: Employees work at the A320 family final assembly line of Airbus factory in Tianjin, China, August 12, 2015. REUTERS/Damir Sagolj

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on Financial and Monetary SystemsSee all

Joe Myers

July 26, 2024

Gregory Van

July 25, 2024

Andrew Howell and Pavel Laberko

July 25, 2024

Lena Haas

July 19, 2024

Joe Myers

July 19, 2024

Meagan Andrews and Hallie Spear

July 17, 2024