Do firms in concentrated markets deter new entrants?

Get involved with our crowdsourced digital platform to deliver impact at scale

Stay up to date:

Japan

Do incumbent firms deter new entrants in a more concentrated market? Economic theories show both possibilities. Prospective entrants have an incentive to enter a monopolistic market because of expected high profits. On the other hand, concentrated markets could make it probable for incumbents to collude in order to deter new entrants. Empirical evidence has supported, by and large, the latter.

Less attention has been paid to two important issues, however.

- One is the analysis of the intermediate goods markets.

It is well recognised that separating final and intermediate goods markets matters, given their different nature (Katz 1989). Particularly, the important role of a vertical contract between buyers and sellers in intermediate goods markets could strengthen the relationship between market concentration and entry.1 However, previous research has ignored this point, mainly due to data limitation.

- The other issue is the definition of ‘market’, which is crucial in determining empirical results.

Many authors have simply used the market boundaries provided by the compliers of official data. However, it is difficult to choose among market definitions, and the official definitions are often inappropriate (Schmalensee 1989). In the analysis, I define market at the buyer-product level. This setting is crucial in analysing the Japanese auto parts industry, where an automaker typically keeps a relationship with two potentially competitive suppliers for each auto part (Konishi et al. 1996).

The analysis makes use of a unique dataset that tracks auto parts transactions between automakers and auto parts suppliers in Japan during the period 1990 to 2010.2 Entry is measured in gross term at the seller-buyer product level.3 The market concentration is measured by the Herfindahl index.

Is the relationship between market concentration and entry non-linear?

Before the main results, stylised facts are overviewed briefly.

- First, auto parts markets in Japan are duopolistic.

The mean number of incumbent sellers (i.e. auto parts suppliers) in the market is 2.3. The duopolistic nature can be observed when the sample is divided by types of product.

- Second, the market is highly concentrated.

The mean Herfindahl index is around 0.7.4

- Third, entry accounts for a large part of transactions.

Roughly one-third of total transactions in 2008 are comprised of new transactions that did not exist in 2002.

- Fourth, multi-product firms have a significant role.

Around 57% of sellers are multi-product firms.

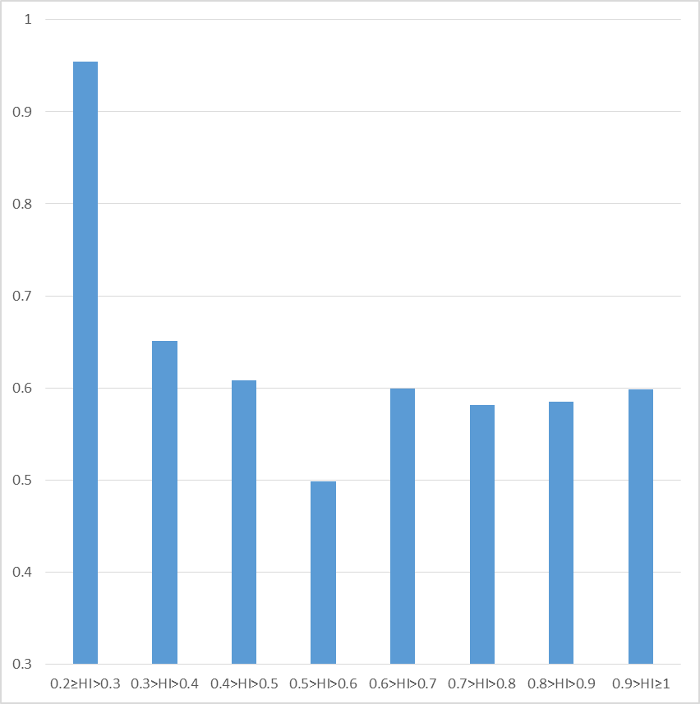

Is there a relationship between market concentration and entry? Figure 1 implies a U-shaped relationship between market concentration and entry. The x-axis is categorised according to the degree of market concentration as measured by the Herfindahl index. The y-axis shows the relative entry index (REI) as measured by the ratio of the number of new transactions that occurred during the period 2002 and 2008 to the number of markets in 2002 for each concentration degree. The results are consistent with prior research for the markets with a relatively low degree of concentrations ranging from 0.2 to 0.6. However, it seems that the relationship turns positive for the range from 0.6 to 1. To test the hypothesis of the non-linearity in a formal way, regression analyses were undertaken with various robustness checks. The results supported the hypothesis.5

Figure 1. Market concentration and entry, 2002-08

Notes: X-axis is categorized according to the degree of market concentration as measured by the Herfindahl index (HI). Y-axis shows the relative entry index (REI) as measured by the ratio of the number of new transactions occurred during the period 2002 to 2008 to the number of markets in 2002 in each concentration degree.

What causes the U-shaped relationship?

One explanation is in the negative correlation between the size of new entry and market concentration, suggesting that potential entrants in concentrated markets aim for a niche product. In a highly concentrated market, incumbent firms have less incentive to deter new entrants as long as potential competitors do not threaten their established transactions with buyers. The models produced in small volume are probably outsourced to such new entrant firms.

Another explanation is that impediments to new entrants are low because of the dominant role of the multi-product firms. As already mentioned above, more than half of sellers are multi-product. In addition, diversification of incumbent firms rather than start of new businesses accounts for a large part of entry. These facts imply that a potential entrant already sells several products to a buyer. Thus, incumbents’ cost advantages over potential entrants become small.

Does the U-shaped relationship still hold when the market is defined at a different level? I tested the product level, instead of the product-buyer level, and the U-shape relationship between market concentration and entry is completely gone.

Policy implications

The results obtained from my study have implications for operating antitrust laws, particularly concerning transactions with exclusive conditionality. Antitrust authorities employ market concentration to examine illegality, and it is recognised that the higher the market concentration, the more likely that the incident is against the law. However, the empirical results show that the relationship between market concentration and entry is non-linear, probably resulting from the multi-product nature of firms. This could draw attention to firm attributes in investigating market structure. The results also highlight the significance of defining a market. The empirical results were quite different, depending on the level of market defined. This could alarm antitrust authorities to pay careful attention to drawing a market scope in investigating the incident.

References

Aghion, P and P Bolton (1987), “Contracts as a Barrier to Entry”, American Economic Review 77, pp. 388-401.

Katz, M L (1989), “Vertical Contractual Relations”, in R Schmalensee and R D Willig (eds),Handbook of Industrial Organization, Volume II, North-Holland, pp. 655-721.

Konishi, H, M Okuno-Fujiwara, and Y Suzuki (1996), “Competition through Endogenized Tournaments: An Interpretaion of “Face-to-Face” Competition”, Journal of the Japanese and International Economies 10, pp.199-232.

Nishitateno, S (2015), “Market Structure and Entry: Evidence from the intermediate goods market”, RIETI Discussion Paper, 15-E-081.

Schmalensee, R (1989), “Inter-Industry Studies of Structure and Performance”, in R Schmalensee and R D Willig (eds), Handbook of Industrial Organization, Volume II, North-Holland, pp. 952-1009.

Yong, J-S (1999), “Exclusionary Vertical Contracts and Product Market Competition”, The Journal of Business 72(3), pp. 385-406.

Footnotes

1 For example, studies such as Aghion and Bolton (1987) and Yong (1999) show that in oligopolistic settings, a monopolistic seller can deter entry through signing exclusive dealing contracts with buyers.

2 The dataset is constructed from “Jidosha Buhin 200 Hinmoku Seisan-Ryutsu Chosa” (“Report on Production and Transactions of 200 Auto Components”) published by the Industrial Research and Consulting (IRC, hereafter), a Japanese market research company. The IRC provides specific information on the volume sold of 200 types of products by auto parts suppliers to automakers. Around 600 sellers, mainly tier-1 suppliers, are covered. Buyers are 12 automakers manufacturing automobiles including both passenger and commercial vehicles (e.g., taxi and truck) in Japan.

3 Entry is identified as a new transaction between supplier i and automaker j for product k in period tthat did not exist in previous period s (e.g., t = 2008, s = 2002).

4 The high degree of market concentration is driven partly by the important role of monopolistic transactions in the Japanese auto parts industry (i.e., one buyer procures a specific auto part from a single seller).

5 See Nishitateno (2015) for details (http://www.rieti.go.jp/jp/publications/dp/15e081.pdf)

This article is published in collaboration with VoxEU. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Shuhei Nishitateno is an assistant professor at the Department of International Policy, School of Public Studies, Kwansei Gakuin University.

Image: A worker arrives at his office in the Canary Wharf business district in London February 26, 2014. REUTERS/Eddie Keogh

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

The Agenda Weekly

A weekly update of the most important issues driving the global agenda

You can unsubscribe at any time using the link in our emails. For more details, review our privacy policy.

More on Geo-Economics and PoliticsSee all

Kiriko Honda

April 25, 2024

Pooja Chhabria and Kate Whiting

April 23, 2024

Robin Pomeroy and Sophia Akram

April 22, 2024

Joe Myers

April 19, 2024

Joe Myers

April 12, 2024

Simon Torkington

April 8, 2024