What can the Fed learn from the history of global inflation?

Carmen M. Reinhart

Minos A. Zombanakis Professor of the International Financial System, Harvard Kennedy School of GovernmentInflation – its causes and its connection to monetary policy and financial crises – was the theme of this year’s international conference of central bankers and academics in Jackson Hole, Wyoming. But, while policymakers’ desire to be prepared for potential future risks to price stability is understandable, they did not place these concerns in the context of recent inflation developments at the global level – or within historical perspective.

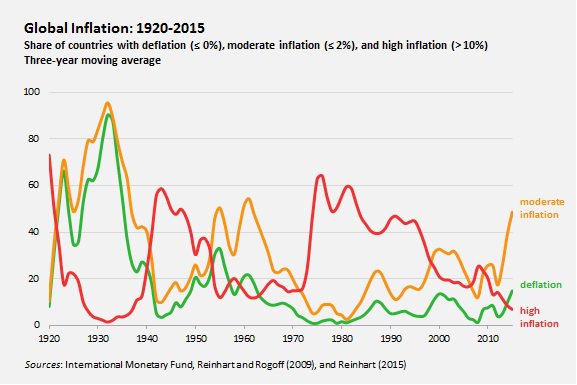

For the 189 countries for which data are available, median inflation for 2015 is running just below 2%, slightly lower than in 2014 and, in most cases, below the International Monetary Fund’s projections in its April World Economic Outlook. As the figure below shows, inflation in nearly half of all countries (advanced and emerging, large and small) is now at or below 2% (which is how most central bankers define price stability).

Most of the other half are not doing badly, either. In the period following the oil shocks of the 1970s until the early 1980s, almost two-thirds of the countries recorded inflation rates above 10%.

According to the latest data, which runs through July or August for most countries, there are “only” 14 cases of high inflation (the red line in the figure). Venezuela (which has not published official inflation statistics this year) and Argentina (which has not released reliable inflation data for several years) figure prominently in this group. Iran, Russia, Syria, Ukraine, and a handful of African countries comprise the rest.

The share of countries recording outright deflation in consumer prices (the green line) is higher in 2015 than that of countries experiencing double-digit inflation (7% of the total). Whatever nasty surprises may lurk in the future, the global inflation environment is the tamest since the early 1960s.

Indeed, the risk for the world economy is actually tilted toward deflation for the 23 advanced economies in the sample, even eight years after the onset of the global financial crisis. For this group, the median inflation rate is 0.2% – the lowest since 1933. The only advanced economy with an inflation rate above 2% is Iceland (where the latest 12-month reading is 2.2%).

While we do not know what might have happened were policies different, one can easily imagine that, absent quantitative easing in the United States, Europe, and Japan, those economies would have been mired in a deflationary post-crisis landscape akin to that of the 1930s. Early in that terrible decade, deflation became a reality for nearly all countries and for all of the advanced economies. In the last two years, at least six of the advanced economies – and as many as eight – have been coping with deflation.

Falling prices mean a rise in the real value of existing debts and an increase in the debt-service burden, owing to higher real interest rates. As a result, defaults, bankruptcies, and economic decline become more likely, putting further downward pressures on prices.

Irving Fisher’s prescient warning in 1933 about such a debt-deflation spiral resonates strongly today, given that public and private debt levels are at or near historic highs in many countries.

Especially instructive is the 2.2% price decline in Greece for the 12 months ending in July – the most severe example of ongoing deflation in the advanced countries and counterproductive to an orderly solution to the country’s problems.

Median inflation rates for emerging-market and developing economies, which were in double digits through the mid-1990s, are now around 2.5% and falling. The sharp declines in oil and commodity prices during the latest supercycle have helped mitigate inflationary pressures, while the generalized slowdown in economic activity in the emerging world may have contributed as well.

But it is too early to conclude that inflation is a problem of the past, because other external factors are working in the opposite direction. As Rodrigo Vergara, Governor of the Central Bank of Chile, observed in his prepared remarks at Jackson Hole, large currency depreciations in many emerging markets (most notably some oil and commodity producers) since the spring of 2013 have been associated with a rise in inflationary pressures in the face of wider output gaps.

The analysis presented by Gita Gopinath, which establishes a connection between the price pass-through to prices from exchange-rate changes and the currency in which trade is invoiced, speaks plainly to this issue. Given that most emerging-market countries’ trade is conducted in dollars, currency depreciation should push up import prices almost one for one.

At the end of the day, the US Federal Reserve will base its interest-rate decisions primarily on domestic considerations. While there is more than the usual degree of uncertainty regarding the magnitude of America’s output gap since the financial crisis, there is comparatively less ambiguity now that domestic inflation is subdued. The rest of the world shares that benign inflation environment.

As the Fed prepares for its September meeting, its policymakers would do well not to ignore what was overlooked in Jackson Hole: the need to place domestic trends in global and historical context. For now, such a perspective favors policy gradualism.

This article is published in collaboration with Project Syndicate. Publication does not imply endorsement of views by the World Economic Forum.

To keep up with the Agenda subscribe to our weekly newsletter.

Author: Carmen Reinhart is Professor of the International Financial System at Harvard University’s Kennedy School of Government.

Image: The United States Federal Reserve Board building is shown in Washington. REUTERS/Gary Cameron

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Geo-economics

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Equity, Diversity and InclusionSee all

Sofiat Makanjuola-Akinola and Dr Zainab Shinkafi-Bagudu

May 19, 2026