A yellow card for the global economy

We've been warned: 2017 saw the largest debt increase in fifteen years Image: REUTERS/Peter Nicholls

The latest figures on the state of the global economy have led investors and economists to use the term “synchronised growth” as a signal of a healthy, robust improvement in the worlds’ economies in 2017, with almost every country in the planet improving its economic output.

Indeed, 2017 was a year in which we saw upgrades to global growth driven by developed markets, with surprisingly stronger U.S. and Eurozone figures, and emerging markets shrugging off commodity volatility to deliver above-consensus growth figures. The world seemed to be finally exiting the risk of stagnation and delivering a promising 2018.

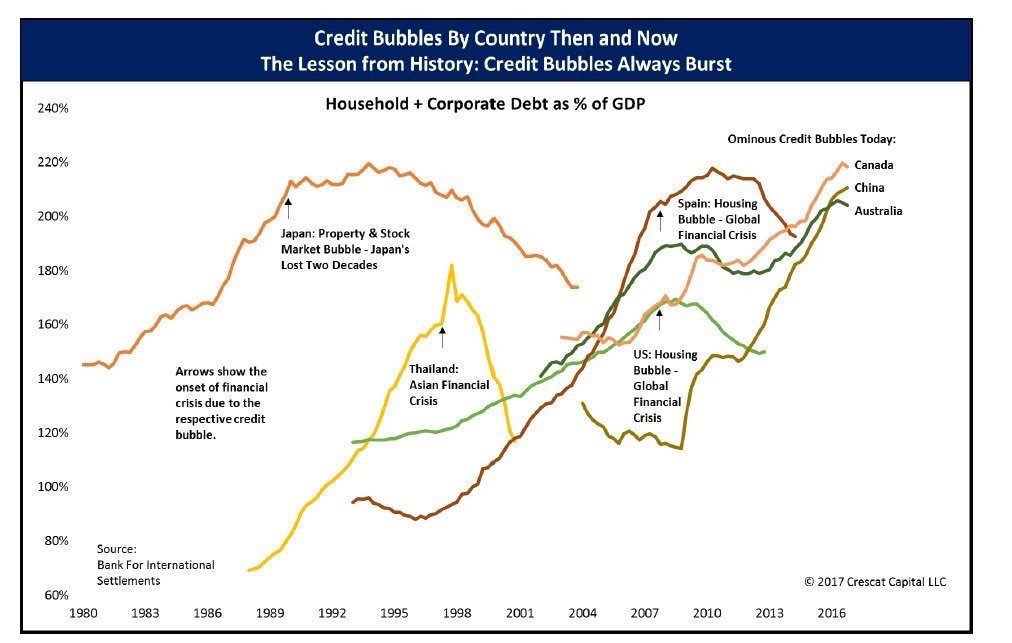

However, synchronised growth arrived with a less attractive partner: synchronised debt. 2017 showed the largest debt increase in fifteen years, and global debt exceeded 325% of GDP.

The dangers of excess debt were all but ignored throughout the year in favour of messages of market confidence and investor demand. Countries such as Argentina were able to issue 100-year bonds at historic low yields with strong demand. China gave up the reform agenda and deleverage policies to increase its debt more than in previous years. Eurozone countries grew accustomed to the abnormal negative rates on 3 to 5-year maturities. Governments started to abandon structural reforms and return to messages of “more deficit spending”. Interest rates were very low: why not?

The rise of the zombie company

The first signs of trouble came with the abnormal rise in zombie companies and the perpetuation of non-performing loans. The number of zombie companies - those unable to cover interest expenses with operating profits - rose above crisis levels, according to the Bank of International Settlements. Low rates did not give companies time to recover solvency, but made many into the “living dead”. At the same time, and despite nearly 2 trillion euro of stimulus from the ECB, non-performing loans in the Eurozone stood above 1 trillion euro.

Moody’s and Standard and Poor’s warned that solvency and repayment capacity ratios were not improving significantly despite ultra-low rates. Furthermore, a worrying signal also started to emerge. Debt for very risky investments with no relevant real economic returns was also on the rise. In some developed countries, up to 80% of investment growth came from the recycling of capital.

With excess confidence in debt markets, we saw an accumulation of more than $7.5 trillion in negative-yielding bonds, more than $11 trillion yielding less than local inflation, and high-yield bonds issued at the lowest rates in thirty-five years.

After eight years of extremely low rates, yield-chasing had become a concern.

The environment of euphoria was exacerbated by a massive rise in financial assets of emerging and developed markets at the beginning of 2018. Maybe we were missing something if we were cautious. Could it be higher inflation finally arriving? Could it be more growth upgrades? Then it burst abruptly.

The party is over

The accumulation of funds in assets that we perceive as “low-risk” is always behind the great corrections and financial crises. What we have seen in the first weeks of February 2018 is a warning sign. An alarm bell that tells us that the party of low rates and debt binges is over. It also tells us that the dangerous bet on zero volatility and low rates forever should not be extended. An alarm that should be taken by government and debt issuers as an opportunity.

Economic agents must take these market events as an opportunity to recover financial sanity while estimates of growth remain positive, industrial indices show expansion and consumer confidence is elevated. 2018 must be a year to strengthen growth and improve sustainability, not to extend imbalances and create a much larger crisis than the previous one.

The opportunity for all economic agents is enormous. The positives must be confirmed, as investment with real economic return at sustainable levels is increasing, as well as healthier consumption patterns driven by improving disposable income. But it is absolutely essential for all of us to understand that the days of cheap and easy money are over, and that the global economy will not be able to get out of another crisis through high liquidity and low rates. Today, we have the main central banks purchasing more than $200 billion per month with no crisis, and rates are between 150 and 250 basic points behind the curve.

The next crisis will not be solved with lower rates and more liquidity, because we are awash with it already.

Let us take this recent correction in financial markets as what it is. A very serious warning.

In soccer matches, referees present players with a yellow card as a warning. If behaviour in the field continues to be unacceptable, players get a red card and are dismissed from the match.

This recent market reaction is a yellow card that tells us to stop increasing debt and imbalances as if there is no risk at all. Let us learn from it. Volatility will rise, rates need to rise, and financial prudence must return. The global economy must avoid a red card.

Daniel Lacalle is a PhD Economist, author of Escape from the Central Bank Trap and Life In The Financial Markets. He is Chief Economist at Tressis.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Inclusive Growth Framework

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

John Letzing

July 3, 2026