4 ways to address the gender finance gap and empower women

Improving financial literacy for women will help them take control of their finances. Image: Alexander Suhorucov, Pexels.

- Gender differences in financial inclusion put women at a further disadvantage, especially in times of crisis.

- Women are generally paid less than men and lack the financial literacy skills and confidence needed to invest their money.

- Here are four ways to become a financial feminist and advance the cause of equality.

“Nothing bad happens when women have more money” states Sallie Krawcheck, a former Wall Street executive and the CEO and founder of Ellevest, a female focussed investment platform. Sallie is one of a growing group of influential and vocal women who are espousing the idea of financial feminism, which stands for financial inclusion and equality for women, not only relating to their earnings, but also to building and keeping wealth.

The situation that women face when it comes to financial wellbeing is dire and must be addressed. Due to a number of factors including systemic inequalities, gender stereotypes and roles, women earn and save less money, and they are less likely to optimise how they invest to build wealth.

Gender differences in financial inclusion have far-reaching effects on women’s quality of life and autonomy, their families and their communities, putting them at risk of financial fragility and poverty, especially in times of crisis. Women have been disproportionately affected during the COVID-19 pandemic, as well as by the climate crisis. Women also tend to live longer than men, which has led to some estimates in Germany putting 75% of women between 35-50 years old at risk of poverty in old age.

Closing the gap on income, investing and wealth

Financial inequality starts at a young age – several studies show boys receive more pocket money than girls. For adults, according to the Global Gender Gap Report 2021, even in Iceland – the country with the smallest gender pay gap – women still earn only 86 cents to a man’s dollar for a similar role. Women’s lower income, together with lower labour market participation and other systemic biases have a compounding effect on women’s ability to build wealth.

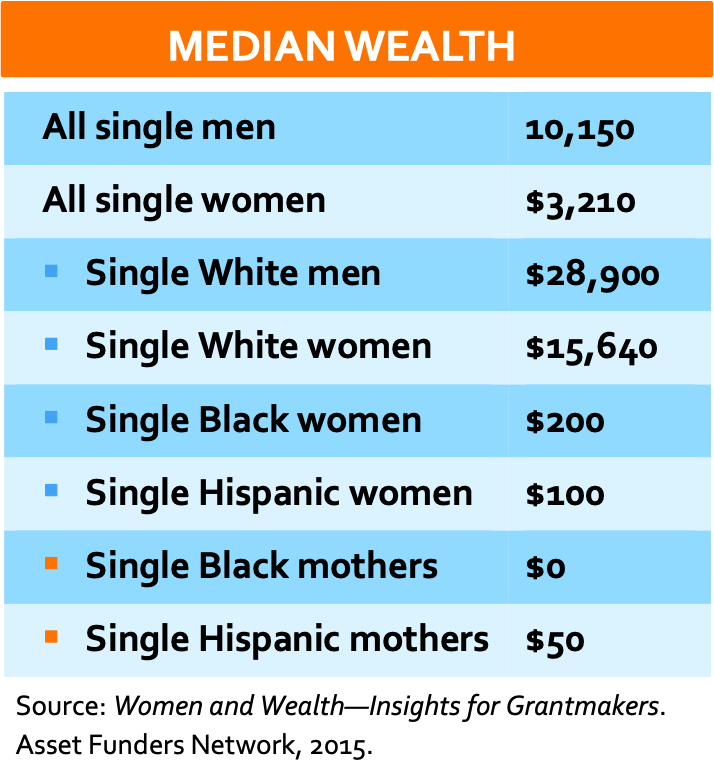

There is evidence that women across the developed world own a disproportionate amount of debt, including student debt, financial institutions charge women higher interest rates, and that women receive lower quality financial advice, for example by being offered more expensive financial products. In the US, while women on average earn 82 cents to a man’s dollar, they only own 32 cents, which drops to mere pennies when comparing black women to both white men and white women.

Financial feminism addresses the gender financial inclusion gaps by engaging, educating and encouraging more women to take control of their finances, as well as raising awareness across society to support these urgent mindset changes. Here are four ways to take part in the movement:

1. Become more fearless

Annamaria Lusardi, who heads the Global Financial Literacy Excellence Centre, is advocating that women need to become more fearless. Women universally lag behind men in financial literacy, which impacts their ability to make sound financial decisions, participate in the stock market, plan for retirement and build wealth. Her recent research found that one third of the gender financial literacy gap can be explained by women’s lack of confidence. Her paper concludes that “when it comes to financial literacy, women know less than men, but they know more than they think they know”.

What does being more fearless look like in practice? Clearly more research is needed, but Lusardi’s paper suggests creating financial education initiatives adapted specifically to women. Improving women’s experience with investing might also build more confidence, for example learning-by-doing by investing in the stock market with very low amounts (Ellevest has no minimum investment amounts). Dr Mara Harvey suggests that we start educating children about financial topics early. She has created a children’s book series that breaks down the financial jargon into easy to understand concepts with rhymes and illustrations.

2. Surround yourself with female role models

Despite a recent backlash against “finfluencers” on social media platforms, there is something to be said about surrounding oneself with role models and financial educators that make one feel part of a bigger movement towards financial equality. TikTok and social media star Tori Dunlap, believes that “having a financial education is a woman’s best form of protest”. Her podcast, aptly titled Financial Feminist reached No. 1 in Apple Business charts (in the US) within 72 hours of being launched in May 2021, highlighting the current appetite for women talking about finance. Bola Sokunbi of Clever Girl Finance wants to help women become accountable, ditch debt, save money and build real wealth. Surrounding yourself with female financial role models normalises talking about money, investing, asking for equal pay and building wealth.

3. Lean on your employer, school, local council

Today, individuals are increasingly responsible for looking after their own finances. Reductions in state-supported pensions, a shift from defined benefits pensions to defined contribution pensions and relatively easy access to credit means that the financial decisions that we make have a profound impact on our quality of life now and in the future.

Employers have a role to play in educating and empowering their workforces and thankfully they are willing to take on the challenge. A recent survey of UK employers by Willis Tower Watson found that four in five employers are looking to develop a financial wellbeing strategy in the next two years. Companies leading the way are proactively adopting financial wellness tech solutions such as nudge, or promoting financial wellbeing through their women’s networks.

Why not start asking questions on how to improve financial literacy for women at your work, school or local council?

4. Connect with and advocate for all your sisters

Women are a diverse group in their own right and we must interact with, listen to, consider and support women who are disproportionately impacted by financial inequalities. This could mean reflecting on one’s privileges and demanding that the experience of women from all parts of society are included in financial feminist efforts. The initiative Closing the Women's Wealth Gap is a great starting point that provides reports and resources to support Black, Indigenous, Latinx and other women of colour, women who are immigrants, women who are LGBTQ and other women who are economically marginalised.

There are also common grounds with women advancing other causes such as climate feminists. Katherine K. Wilkinson and Ayana Elizabeth Johnson’s book All We Can Save aptly describes feminine traits as being important to address the climate crisis, which also apply to financial feminism: collaboration, connection, compassion and creativity.

Given anecdotal evidence that women are more likely to prioritise social or ESG investing principles, linking women’s social and sustainable interests to wealth building warrants further exploration. One approach that is gaining traction is to ask employers to commit to investing pensions in a sustainable way. The UK’s Make My Money Matter initiative encourages employees to use their pension to change the world.

Financial feminism thus presents an opportunity not only to reduce the gender pay, investing and wealth gaps, but also to use women’s increasing financial power to align with the goals and actions required to build a sustainable future for all.

Victoria Mallinckrodt is a co-founder of the Finance Sisters, a social enterprise aimed at helping women take control of their finances.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Financial and Monetary Systems

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Equity, Diversity and InclusionSee all

Natalie Pierce and Christa Odinga-Svanteson

June 30, 2026