When the chips are down: How the semiconductor industry is dealing with a worldwide shortage

A confluence of problems led to the semiconductor chip shortage Image: Reuters/Lim Huey Teng

Listen to the article

- Semiconductor chip shortages have been aggravated by the pandemic.

- Manufacturers are increasing chip production – but the shortfall won't be resolved immediately.

- Despite the current problems, the industry remains highly profitable.

When chip shortages first shut down automotive production lines in 2021, the semiconductor industry found itself in an unaccustomed spotlight. Suddenly everyone was talking about the tiny chips that enable so many different car functions, from interior lighting to seat control to blind-spot detection. When some high-tech and consumer-electronics companies began to experience chip shortages or voiced concerns about supply chains, the attention intensified. It’s now clear to all: We are living in a semiconductor world.

But what led to the current dilemma? And what lies ahead for the semiconductor sector and the significant economic value that it generates?

Chip shortage - less supply, more demand

A confluence of problems led to the semiconductor shortage. In addition to long-standing issues within the industry, such as insufficient capacity at semiconductor fabs, the COVID-19 pandemic introduced unprecedented challenges. For instance, automakers cut their chip orders in early 2020 as vehicle sales plummeted. When demand recovered faster than anticipated in the second half of 2020, the semiconductor industry had already shifted production lines to meet demand for other applications.

Semiconductor companies have increased throughput, which will contribute to expected revenue growth of about 9% in 2021 – up from the approximate 5% recorded in 2019, the last pre-pandemic year. Some governments are also upping their investment in semiconductor technology to lessen the impact of global supply-chain disruptions.

But the current chip shortage is unlikely to be resolved in the near future, partly because of the complexities of the semiconductor production process. Typical lead times can exceed four months for products that are already well established in a manufacturing line (see below). Increasing capacity by moving a product to another manufacturing site usually adds another six months (even in existing plants). Switching to a different manufacturer typically adds another year or more because the chip’s design requires alterations to match the specific manufacturing processes of the new partner. And some chips can contain manufacturer-specific intellectual property that may require alterations or licensing.

The value at stake worldwide

Many companies that need semiconductors are already reconsidering their long-term procurement strategies. Some, for instance, may shift from a “just-in-time” ordering model, which helps minimize inventory costs, to one in which they order semiconductors far in advance. For their part, many semiconductor companies are adjusting their long-standing strategies to remain strong.

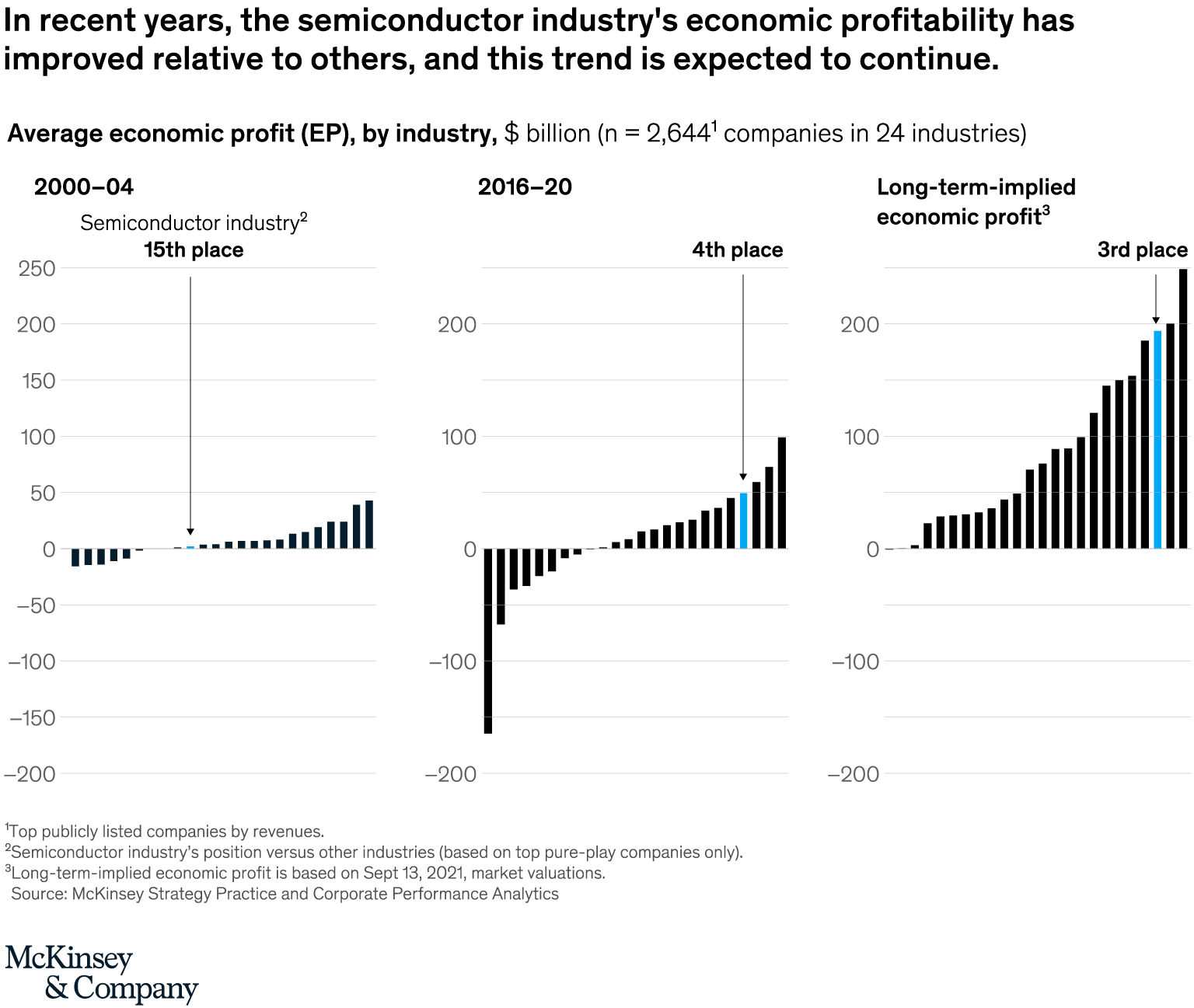

The decisions that semiconductor companies make could have enormous economic significance, both for their industry and the economy as a whole. And the stakes have never been higher. In the early 2000s, profit margins were low at semiconductor companies, with most generating returns below the cost of capital. Profitability improved during the past decade, however, spurred by soaring demand for microchips in most industries, the rapid growth of the technology sector, and increased cloud usage, as well as ongoing consolidation in many sub-segments. One consequence is that the semiconductor industry’s profitability has improved significantly relative to other industries, and this trend is expected to continue (see below).

As in any industry, value creation varies by product category, so changes in some segments could have a greater impact than others. For instance, memory has been the most profitable segment, followed by fabless companies that design their own chips but outsource their manufacture. Some regional variations are also obvious. North America, home to some of the largest fabless players, accounted for approximately 60% of the global semiconductor value pool during the 2015-19 period. Europe accounted for 4% of the industry’s total economic profit, which accrued primarily to capital-equipment companies. Asia, still the hub for contract chip manufacturing, accounted for the remaining 36%. With this geographic spread, value creation within the semiconductor industry can affect economies worldwide (see below).

Next steps for a critical industry

Capital markets have rewarded the semiconductor industry’s surging profitability, with companies in this sector delivering an annual average of 25% in total returns to shareholders from the end of 2015 to the end of 2019. Last year, shareholders saw even higher returns, averaging 50% per annum, as consumers and businesses upped their purchases of digital equipment of all kinds, partly in response to the COVID-19 pandemic. The question is whether the semiconductor industry can continue delivering such strong returns, especially as the pandemic continues to create uncertainties about demand patterns, supply chains and other issues.

Beyond increasing production capacity, semiconductor companies could consider several steps to continue their growth and meet customer demand. They could undertake more M&A deals and partnerships to gain an edge in profitable segments and expand their customer base. Semiconductor companies might also increase investments in innovative technologies that will help them develop leading-edge chips for autonomous cars, the internet of things, artificial intelligence, and other areas with burgeoning growth. Above all, more agile strategies may be important during these uncertain times.

How the Forum helps leaders connect frontier technologies to real-world challenges

No matter what tactics they implement, the decisions that semiconductor companies make will reverberate far beyond their industry to touch the high-tech, consumer goods and automotive companies that depend upon them.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Electronics

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Supply Chains and TransportationSee all

Maciej Kolaczkowski

June 26, 2026