The Net-Zero Industry Tracker

Aluminium Industry

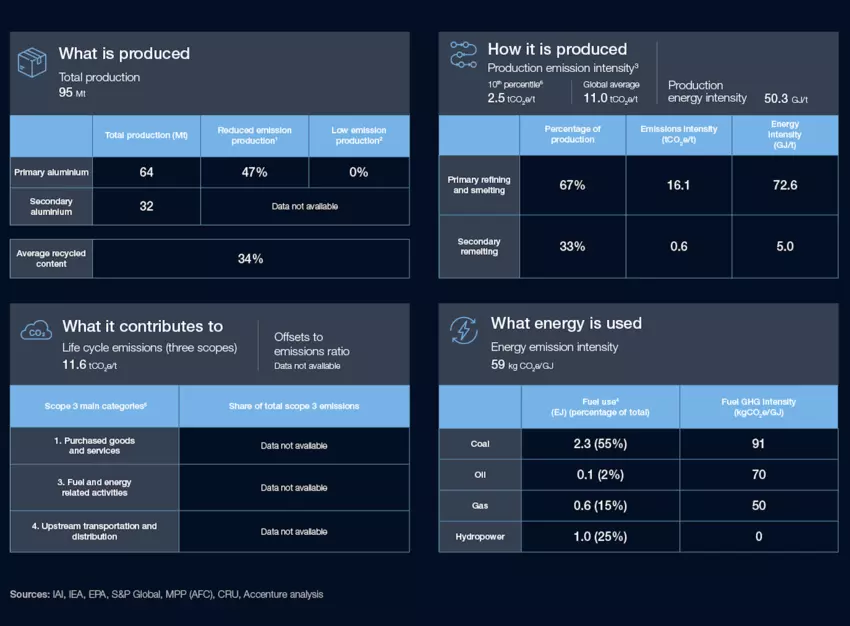

Aluminium is a lightweight, corrosion-resistant, highly malleable and infinitely recyclable material which finds usage in multiple industries, including construction (25%), transport (25%), electrical equipment, machinery and packaging; it has no scalable substitutes today, and its use in the renewable energy industry makes it a critical material for achieving net zero. Manufacturing aluminium requires highly energy intensive processes to extract alumina from bauxite and turn it into aluminium. More than70% of the energy used comes from fossil fuels, largely to produce captive electricity to run smelters (primary aluminium) and electric induction furnaces (recycled aluminium). Almost 50% of aluminium is made in China.

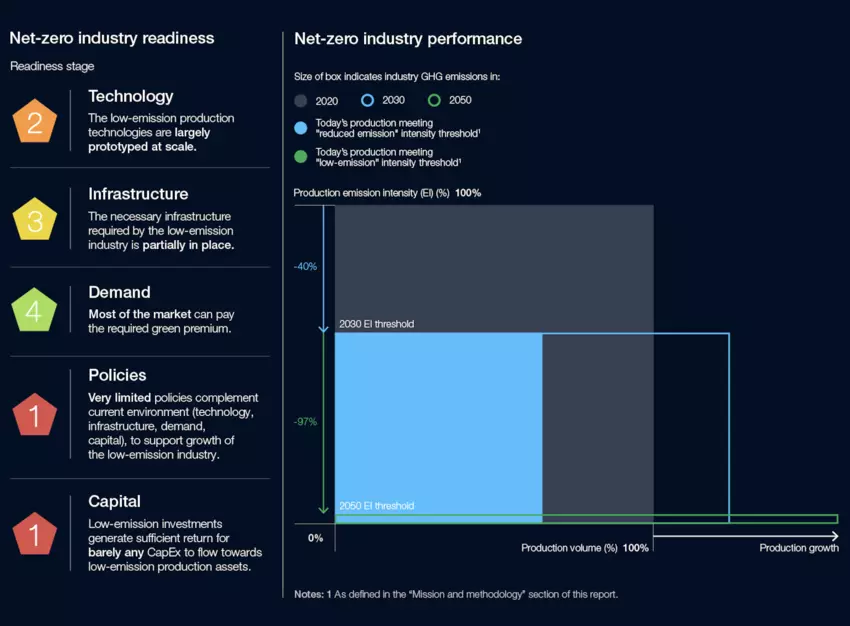

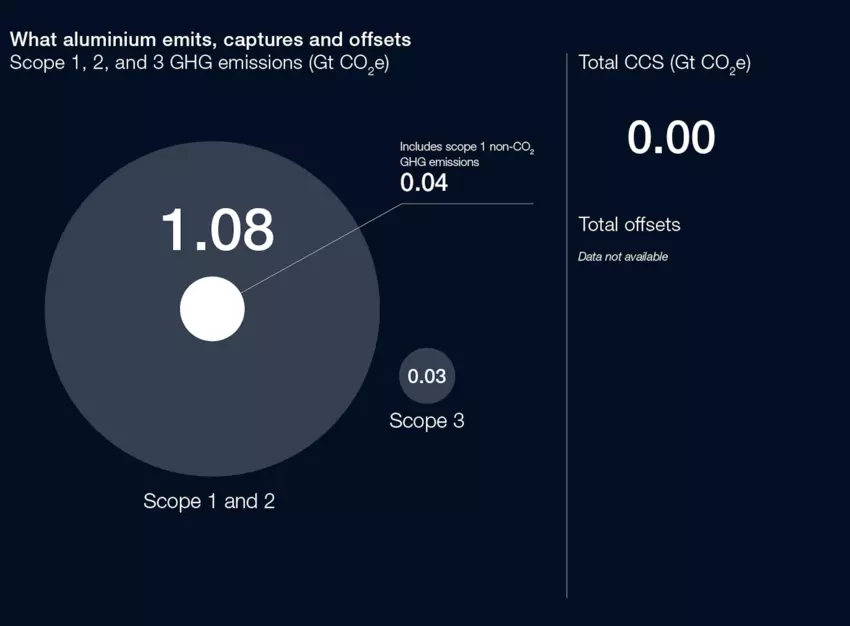

The aluminium sector generates about 2%of all man-made emissions – aluminium is one of the most emission-intensive industrial materials today (seven times that of steel). Partly because aluminium is bound to play a role in reducing emissions of other sectors (such as light-weighting cars and trucks), its demand is projected to rise by 80% by 2050. Aluminium recycling, i.e. secondary aluminium production, can be nearly carbon neutral if powered by renewable electricity; hence it will be essential to decarbonize electricity supply. Demand cannot be met with recycled aluminium alone. Primary aluminium is projected to meet at least 50% of aluminium demand in 2050and must be decarbonized.

The challenge for primary aluminium is twofold:decarbonize energy for refining and smelting and prevent CO₂ release to the atmosphere during the smelting process. The decarbonization pathway combines two building blocks:electrification with low-carbon power for refining and smelting, and hydrogen use for high heat. Carbon capture is also being explored but faces significant challenges (e.g. low CO₂ concentration). Today, decarbonizing power can already cut emissions by 60%, and upto 85% could be achieved with future electric boilers and inert anodes. Cost estimates for aluminium low-emission technologies are largely unknown due to their early stage of maturity, except for the use of CCUS for thermal energy and process emissions, which is estimated to raise production costs by 40%.

Aluminium is one of the most emission-intensive manufacturing sectors-generating 2% of all man-made emissions. More than 70% of its energy consumption comes from fossil fuels.

Besides investments in production assets, atleast $510 billion in infrastructure investments in low-emission power generation, hydrogen production, and carbon transport and storage will be required. Low-emission aluminium is expected to reach the market by 2030 with a green premium of up to 40%. To incentivize investments, demand signals for low-emission aluminium from wholesale buyers should be multiplied. This will require strengthening aluminium buyers’ confidence in their ability to pass the premium to end consumers, which shows encouraging signs.

Public policies and international cooperation on carbon pricing, carbon border adjustment mechanisms or product specification standards can help create a differentiated and economically viable market for first movers into the low emission aluminium industry. The low maturity of most technologies makes it hard to size the investment required to transform the industry asset base. Moreover, current business case and projected returns on low-emission assets do not encourage mainstream investments.

We emphasize five priorities for the sector:

1. Promote and further expand aluminium recycling networks.

2. Boost the number of low-emission projects to accelerate the learning curve, drive costs down and bring forward the commercial readiness of clean technologies.

3. Develop the low-emission power capacity, clean hydrogen production and CO₂ transport, and storage infrastructure required to enable low-emission aluminium production.

4. Multiply demand signals for green aluminium to incentivize producers and investors to direct capital towards low-emission production assets.

5. Develop policies to support the four priorities above and strengthen the business case for low-emission aluminium production