Why Asia’s economic rise will be uneven

The rise of the East will be uneven. Asia’s emerging and developing economies have coped better than most with the aftermath of the global financial crisis, growing faster than any other region in the past decade. But some are better positioned than others for further growth.

This picture of diverging trajectories in the region is confirmed by the latest edition of the World Economic Forum’s Global Competitiveness Report, which analyses the fundamental features of economies on which growth can be built. Broadly speaking, China and ASEAN (Association of Southeast Asian Nations) countries are more competitive now than in 2007; India and South Asia less so, although there are recent signs that they may be turning the corner.

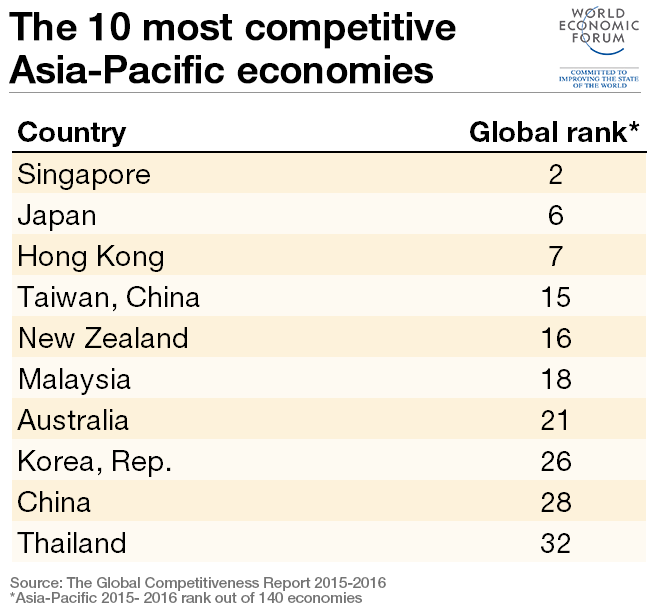

The five biggest ASEAN countries – Malaysia, Thailand, Indonesia, the Philippines and Vietnam – all feature in the top half of the overall index rankings, and all but Thailand have improved their ranking since 2007. Top performer Malaysia has particularly broad-based strengths: it ranks in the top 50 on all 12 “pillars” of competitiveness analysed by the Global Competitiveness Index, which uses a mixture of quantitative data and surveys of executive opinion.

Comparing the factors rated by executives as most problematic for doing business suggests that the best way for ASEAN’s top performers to keep making progress is to improve institutions. Governance-related issues topped the list of concerns in Malaysia (inefficient government bureaucracy), Thailand (government instability) and Indonesia (corruption, despite impressive recent progress in this area); by contrast, the concerns in Asia’s advanced economies centred on labour market regulations (Singapore), tax rates (Japan) and capacity to innovate (Hong Kong).

Capacity to innovate also topped the list of concerns in China, as the country grapples with how to manage the transition from the “efficiency-driven” stage of economic development to the “innovation-driven” model that characterizes advanced economies. With a higher GDP than all Asia’s other emerging and developing economies combined, the success of China’s transition is crucial to the region.

The index suggests that returns on competitiveness are diminishing from the factors which have driven China’s growth in recent decades, with the country’s solid overall position of 28th nonetheless reflecting stagnation in recent years. Alongside efforts to nurture a culture of innovation – such as improvements in higher education and access to technology, both areas in which China lags well behind its overall score – future gains in competitiveness will likely have to come from a focus on market efficiencies. These include reforms to help small businesses by reducing the advantages enjoyed by state-owned enterprises.

China has improved its position since before the crisis, having advanced six places from its ranking of 34th in 2007. India had gone the other way: it ranked 48th in 2007, but fell to just 71st in last year’s report. The new edition of the index, however, suggests that the decline has been dramatically reversed, with India rising 16 positions to 55th.

India’s progress reflects the reforms initiated by Narendra Modi since his election as prime minister in May 2014. Encouragingly for future prospects, these improvements are broad-based – spanning 10 of the 12 pillars in the index – and especially concentrated on the four “basic requirement” pillars: health and primary education (up from 98th to 84th), macroeconomic environment (101st to 91st), infrastructure (87th to 81st) and institutions (70th to 60th).

In one of the indicators that comprises the institutions pillar, a measure of public trust in politicians, India progressed from 50th to 31st. The challenge now is to convert that trust into further improvements in institutions, given that executives still ranked corruption as the biggest hurdle to doing business in India. Other priority areas include tackling the government budget balance (worse than all but nine of the 140 economies in the index), simplifying the process of starting a new business (only 11 other countries require more procedures), and closing the digital divide (only 27 countries have a lower proportion of their population connected to mobile broadband).

On the whole, India’s fellow members of the South Asian Association for Regional Cooperation also failed to match the leading ASEAN nations’ progress on competitiveness since 2007. Only Nepal has made significant progress in that time and only Sri Lanka (68th overall) joins India in the top half of the index.

Nonetheless, across emerging and developing Asia, most of the economies in the bottom half of the competitiveness index are on an upward trajectory. Lao PDR (83rd), Cambodia (90th), Nepal (100th), Bangladesh (107th) and Myanmar (131st) all advanced over the past year, with only Mongolia (104th) and Bhutan (105th) slipping back. While the benefits from the eastward tilt of the global economic axis may be felt unequally, the region’s trend remains on the whole positive.

The Global Competitiveness Report 2015-2016 is available here.

Have you read?

The 10 most competitive economies in Asia-Pacific

How can Europe raise its competitiveness?

How can Latin America close its wealth gap

Author: Thierry Geiger, Head of Analytics and Quantitative Research, Global Competitiveness and Risks, World Economic Forum

Image: People dine at a rooftop restaurant on a “Supertree” vertical garden structure at the Gardens by the Bay waterfront park in Singapore July 16, 2015. REUTERS/Edgar Su

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Innovation

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Rishika Daryanani, Daniel Waring and Tarini Fernando

November 14, 2025