The future of global competitiveness: 4 decision-makers reveal their strategies for surviving uncertainty

Today’s turbulent times are forcing companies and countries to rethink their strategies to secure competitiveness. Image: Tom Fisk/Pexels

- The World Economic Forum has published a new white paper, Global Economic Futures: Competitiveness in 2030, in collaboration with Accenture.

- It explores how geopolitics and business regulations could shape the future of competitiveness and lays out strategies to help leaders navigate uncertainty.

- Decision-makers from different sectors here offer their thoughts on the disruptive forces impacting their industries and strategy responses to heightened uncertainty.

The global economy is in flux, with uncertainty reaching historic heights.

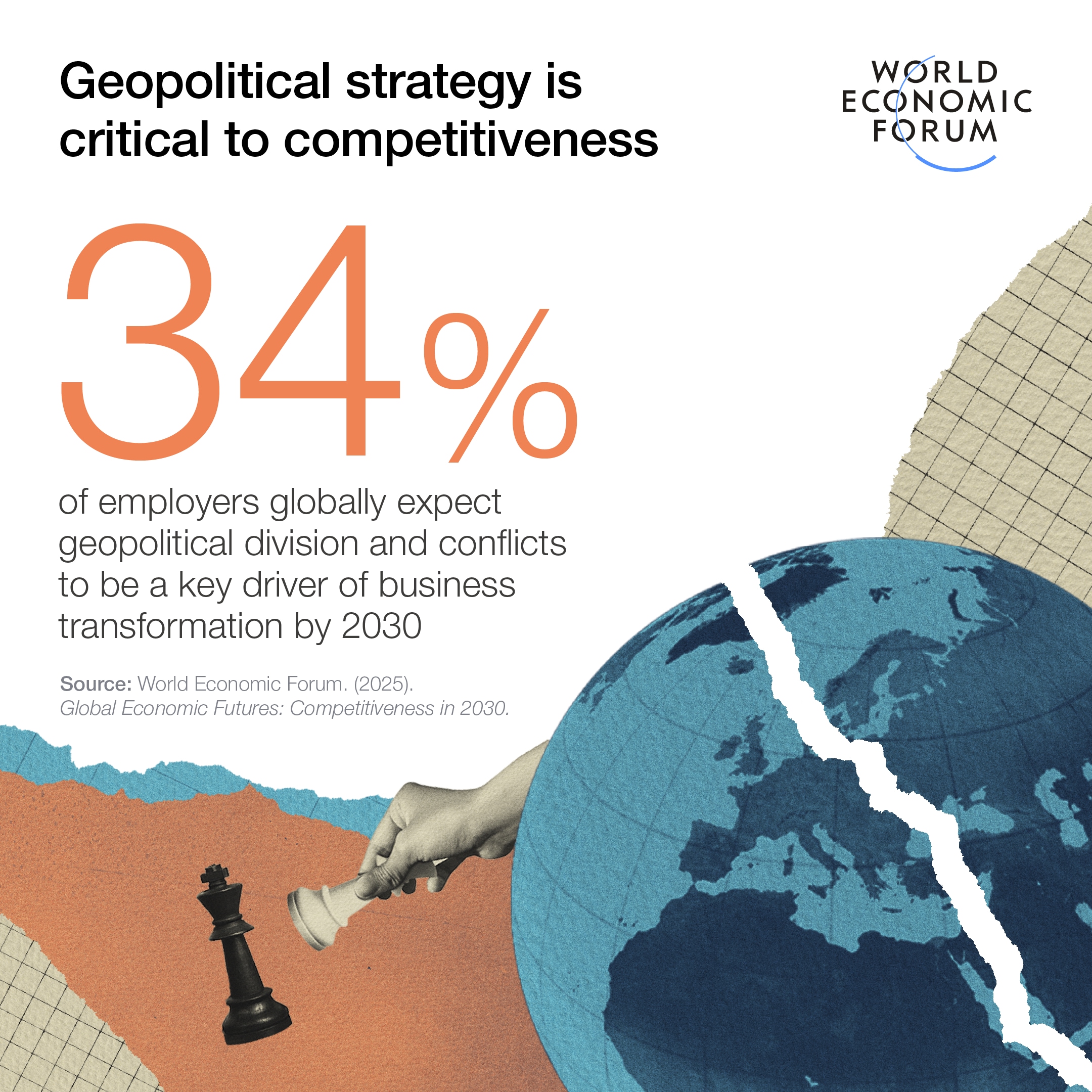

Geopolitical rifts are widening and decision-makers are grappling with slow growth, tight financial space and mounting trade-offs between national and global priorities.

Fast-changing technologies, shifting demographics and growing climate vulnerabilities are set to further reshape the global landscape in the coming years.

Remaining competitive in such an environment is becoming increasingly difficult, but also increasingly essential. Identifying problems is one thing, finding solutions is much harder. Being able to pinpoint strategies to deal with heightened geopolitical and economic uncertainty is what will enable companies and countries to retain – and hone – their competitive edge.

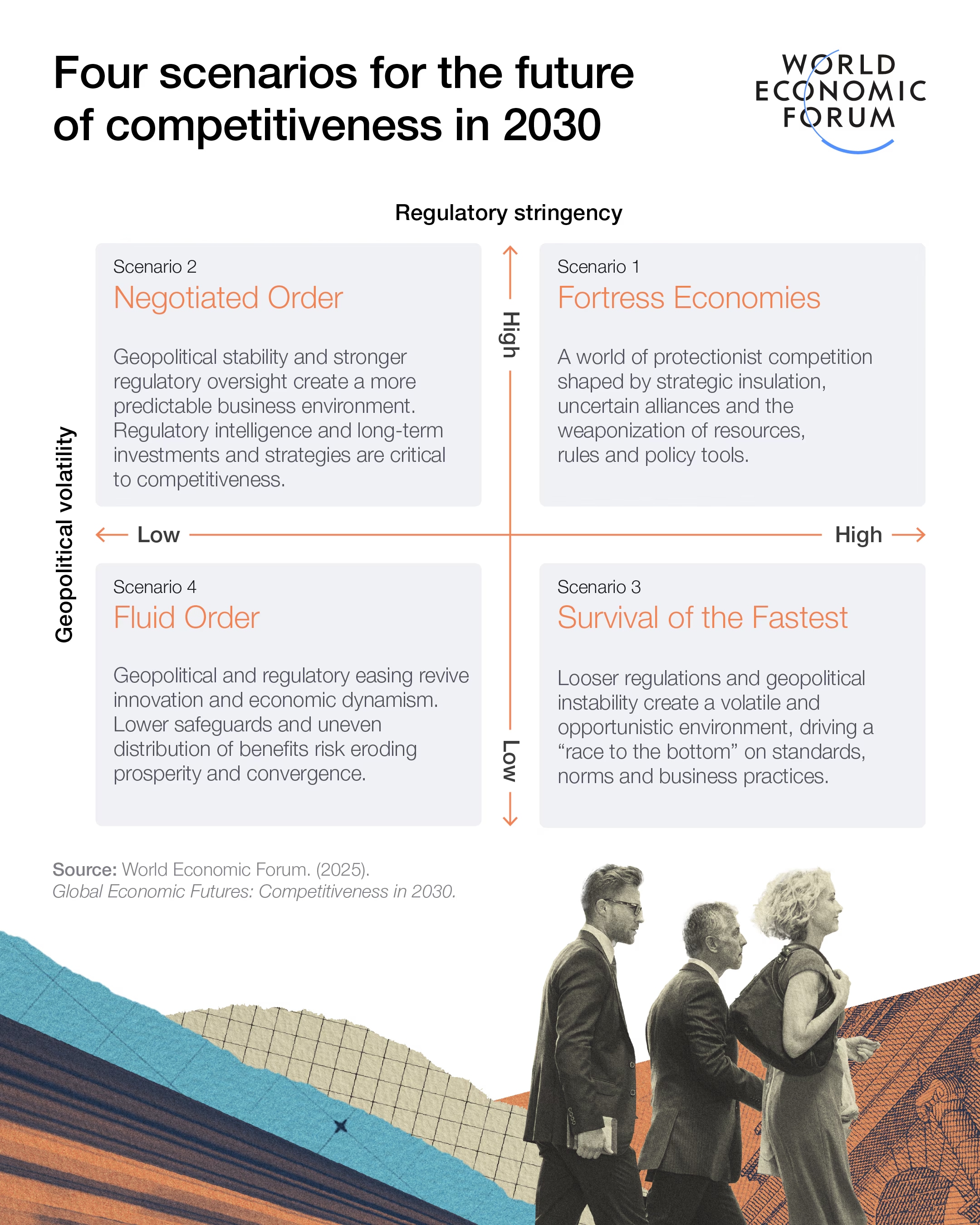

The second edition of the World Economic Forum’s Global Economic Futures series, developed in collaboration with Accenture, sets out four scenarios for competitiveness that could unfold over the next five years. Each of these futures has the potential to reshape sectors and strategies.

We asked top executives what is the single most disruptive force shaping competitiveness in their sector and why? And what is the most significant strategy shift they're seeing in response to heightened geopolitical and economic uncertainty. Here's what they said.

Bart Brouwer, Head of Corporate Development, ING Group

The most disruptive force currently shaping competitiveness in the European banking sector is geopolitical risk. This includes ongoing conflicts like the war in Ukraine, rising tensions with global powers such as the US and China, and growing uncertainty around supply chains and trade tariffs.

These dynamics generate financial instability and disrupt cross-border operations, while also increasing regulatory fragmentation. As a result, compliance becomes more complex and costly for banks operating across multiple jurisdictions. Geopolitical shocks also influence macroeconomic variables, such as interest rates, inflation and credit conditions, which directly affect banks’ profitability and risk exposure.

An increasingly critical dimension of geopolitical risk is cybersecurity. Heightened tensions have led to a surge in cyber threats, compelling banks to invest heavily in digital resilience and operational continuity.

While other forces like AI-driven innovation, climate regulation and talent shortages are shaping the banking sector, geopolitical risk stands out to me for its capacity to trigger sudden, systemic disruptions. These events can rapidly disrupt economies and the banking landscape, making it the most urgent and unpredictable challenge facing European banks today.

In general, banks are responding by embedding geopolitical risk assessments into their core risk management frameworks, strengthening their capital and liquidity buffers where needed and investing heavily in cybersecurity and operational resilience.

Jean-Pascal Clémençon, Senior Vice-President, Strategy and Markets, TotalEnergies

Resource availability is crucial for the energy sector. For years, Middle Eastern oil producers led on oil and refined products exports due to [their access to] vast, low-cost, onshore reserves. In the span of a decade, the US transitioned from an oil and gas importer to a leading LNG [liquefied natural gas] exporter and gained an edge in the petrochemical sector through the shale revolution, thanks to its unique ecosystem of abundant resources, incentive-based regulation and a dynamic services industry.

The Ukraine war prompted a significant strategic shift as Europe had to replace Russian pipeline gas with US LNG. A tight LNG market where Europe now imports, coupled with historic [highs in] Asian demand, caused gas and electricity prices to spike.

Energy price increases have reduced Europe's industrial competitiveness, creating a strong burden for energy-intensive sectors and straining state budgets, impacting the energy transition through reduced support for emerging, low-carbon technologies. Security of supply has become a new priority, helping to revive the nuclear industry in some countries and promoting renewables in others.

Renato Lulia Jacob, Group Head of Corporate Strategy, Corporate Development & Investors Relations, Itaú Unibanco

The most profound force reshaping our financial sector today is technological innovation. While global instability carries long-term implications, it is technology that represents the most immediate and disruptive agent of change. This transformation offers both a formidable opportunity and a significant threat to organizations worldwide – enabling new levels of efficiency and insight, while demanding agility, responsibility and structural adaptability in equal measure.

Brazil has emerged as a leader in digital finance, driven by increasingly intelligent platforms and a culture of rapid adoption. We are contributing to this evolution through the deployment of generative artificial intelligence [GenAI], with more than 500 use cases developed – including over 100 already in production. Our super app integrates over a thousand AI models to offer clients highly personalized experiences, and we were the first to launch a fully conversational investment adviser. Together, these technologies are ushering in a new era – one that is more consultative, empathetic and centred on long-term financial well-being.

The current global context – characterized by geopolitical tensions, currency volatility and fluctuations in commodity prices – requires robust and forward-looking strategies. In Brazil’s financial sector, this has prompted a multidimensional response combining disciplined credit allocation, a relentless pursuit of operational efficiency and a deep commitment to innovation.

We have embraced a client-centric model powered by digital solutions that enhance both the customization of our services and the resilience of our results. A key pillar of this strategy is our proprietary GenAI framework, which is being embedded across transactional and financial management tools to support decision-making for individual and corporate clients alike.

We’ve also established the Itaú Institute of Science and Technology, which is currently conducting over 50 research projects in artificial intelligence and quantum computing, in collaboration with academic institutions such as Stanford University and MIT.

Yin Zou, Executive Vice President of Corporate Development, DHL Group

AI is the most disruptive force reshaping competitiveness in the logistics sector. It is driving efficiency to new heights, transforming how companies operate. Generative AI, for instance, optimizes routing and inventory management in real time, significantly reducing costs and addressing labour shortages through automation.

Moreover, AI fosters innovative business models, such as predictive shipping, which enhances resource-sharing ecosystems. This approach can boost asset utilization by as much as 60%, providing companies with a sustainable competitive edge. Unlike external factors such as geopolitics or trade policies, AI offers firms a controllable competitive advantage. By utilizing proprietary data and rapid innovation cycles, companies can maintain a competitive edge in their landscape. In essence, AI not only streamlines operations but also opens up new avenues for growth and efficiency in logistics.

The key strategic shift we're seeing is diversification of the supply chain. Geopolitical volatility has forced three critical adaptations: geographic rebalancing, multi-sourcing networks and tech-enabled resilience. We are seeing that companies are expanding their supply chains across different regions instead of relying on a single location.

This is helping them avoid risks from geopolitical tensions and keep their operations running smoothly. At the same time, businesses are working with multiple suppliers for the same products. This approach reduces reliance on a single source, enhances negotiation power and enables quicker responses to changes in demand. Lastly, firms are utilizing technology such as AI and data analytics to strengthen their supply chains. These tools enhance visibility and enable companies to respond more quickly to disruptions, thereby improving the efficiency of their operations.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Contents

Bart Brouwer, Head of Corporate Development, ING Group Jean-Pascal Clémençon, Senior Vice-President, Strategy and Markets, TotalEnergiesRenato Lulia Jacob, Group Head of Corporate Strategy, Corporate Development & Investors Relations, Itaú UnibancoYin Zou, Executive Vice President of Corporate Development, DHL GroupForum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.