Middle East energy crisis puts pressure on global markets, and other finance news to know

This is the "largest supply disruption in the history of the global oil market," says International Energy Agency Executive Director, Fatih Birol. Image: REUTERS

- Catch up on the key stories and developments shaping the financial world.

- Top stories: Energy shock shakes markets; Investors move to cash amid uncertainty and volatility; European corporate distress climbs.

- For more on the World Economic Forum's work in finance, visit the Centre for Financial and Monetary Systems.

1. Energy infrastructure volatility weighs on global financial outlook

Damage to key energy infrastructure during the ongoing Middle East crisis and the effective closure of the Strait of Hormuz for most commercial traffic — the route for around 20% of global oil and 21% of LNG — are driving a major shift in the global financial outlook. Analysts warn that markets may be underestimating the scale of the disruption.

International Energy Agency (IEA) Executive Director, Fatih Birol, has warned that the situation is "very severe" and that both policymakers and investors have yet to fully grasp the potential impact of what he has described as the "largest supply disruption in the history of the global oil market".

The impact of supply disruption

Brent crude rising above $110 per barrel signals a shift away from short-term, conflict-driven price spikes towards real constraints on global supply. Goldman Sachs has sharply revised its oil price forecasts for 2026, projecting that Brent crude will average $85 a barrel this year — up from an earlier estimate of $77.

These moves follow damage to critical infrastructure across the region, including Israeli strikes on Iran's South Pars gas field and retaliatory strikes on Qatar’s Ras Laffan complex, where damage to two LNG trains is expected to sideline 17% of the country’s export capacity for up to five years. While prices retreated following US President Trump's announcement of a five-day pause in attacks on 23 March, the "supply shock morphing into a demand shock" remains a primary concern for long-term stability.

Although efforts are underway to resume Iraqi oil exports through Türkiye, these volumes are unlikely to make up for disruptions linked to the Strait of Hormuz, commentators say.

Birol noted that while the IEA coordinated a record release of 400 million barrels from strategic reserves this month, and would be prepared to do so again, "if necessary", such measures can only provide temporary relief and do not address the underlying supply gap.

Signs of growing market strain

Investors are increasingly preparing for broader economic consequences as the supply shock begins to affect demand. Recent Reuters analysis points to several warning signs:

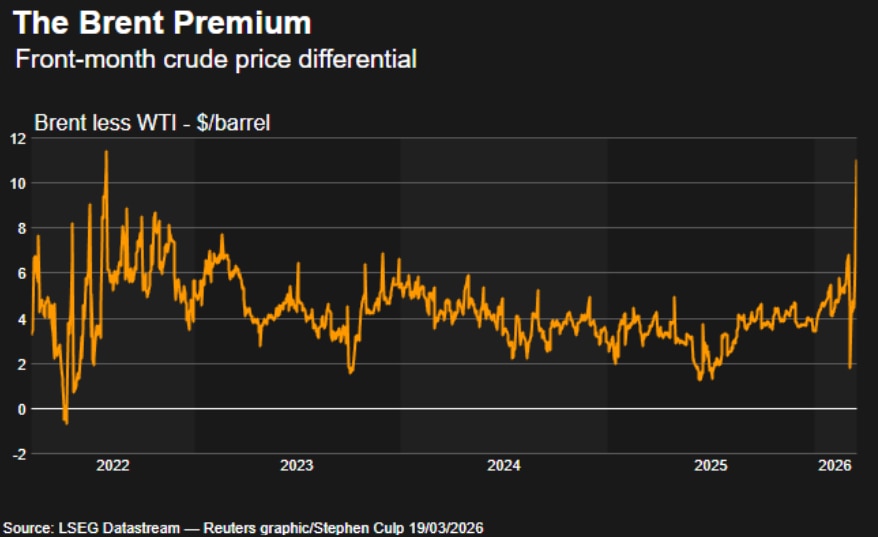

- Widening price gaps: The difference between Brent crude and US oil (WTI) has widened significantly, reflecting a more strained supply environment and increasing costs for energy-importing regions such as Europe and Asia.

- Rising bond yields: Government borrowing costs are climbing, with the US 10-year Treasury yield reaching 4.38%, a multi-month high, as investors anticipate interest rates may remain elevated for longer.

- Limited central bank flexibility: Markets are scaling back expectations for rate cuts, with some now anticipating further tightening as central banks balance inflation risks against slowing growth.

- Credit market pressure: The cost of insuring corporate debt is rising, with credit markets showing signs of strain as higher energy prices weigh on corporate balance sheets.

A structural shift in risk

Taken together, these developments suggest that energy disruption is no longer a temporary market factor. Instead, it is becoming a structural force shaping global financial conditions.

This shift is likely to keep borrowing costs elevated and increase market volatility, requiring investors to move beyond passive strategies and focus more on resilience and risk management.

2. Record migration to money market funds as investors prioritize liquidity

As geopolitical volatility and energy shocks continue to weigh on markets, investors are moving into cash-equivalent instruments at a record pace. Total money market fund assets rose by $38.68 billion in the week to 18 March, reaching a new high of $7.86 trillion, a recent Investment Company Institute (ICI) report says.

This “dash for cash” is intensifying as rising inflation linked to the Middle East crisis erodes the appeal of longer-duration assets, according to Bloomberg. In response, many investors are favouring the relatively stable yields and immediate liquidity offered by money market funds over government bonds, which have recently faced selling pressure.

The move is being led largely by institutional investors, with the ICI reporting an additional $27.77 billion flowing into government-backed funds. Analysts describe this as “wait-and-see” capital, held back until there is greater clarity on the path of interest rates and the broader economic impact of the energy shock.

This growing pool of cash is also being used as a hedge against stagflation, they suggest. With Brent crude volatile after recent spikes, holding cash offers a way to avoid the sharp swings affecting both equity and bond markets.

3. More finance news to know

Demand for cash is surging in Iran as the war fuels inflation and currency pressure, with queues forming for banknotes as fears grow over the stability of electronic payments. The rial has come under renewed strain, highlighting rising financial stress in the economy amid ongoing conflict and sanctions.

US regulators are moving to soften 'Basel III', a global set of banking rules on capital requirements, cutting required reserves by about 4.8% and freeing up billions for lending and buybacks. Trading-heavy firms such as Goldman Sachs and Morgan Stanley stand to benefit most, though the changes could strain industry unity as banks compete for favourable final terms.

European corporate distress has climbed to a four-year high, with 13.5% of companies under pressure, according to Alvarez & Marsal. The energy shock is acting as a “distress multiplier”, hitting leveraged manufacturers and retailers hardest as costs and debt burdens rise.

UK mortgage rates are edging higher as markets reassess the outlook for interest rates amid renewed geopolitical tensions. Investors are adjusting expectations for the path of policy, with focus on signals from the Bank of England. The move is feeding through into borrowing costs, putting additional pressure on households and the housing market.

Japanese firms are set to deliver an average 5.26% wage increase, according to preliminary data, reinforcing expectations of sustained inflation and a potential shift in policy from the Bank of Japan. The stronger wage growth may support a gradual move away from ultra-loose monetary settings, with implications for the yen and global rates markets.

4. Read more on Forum Stories

Gen Z’s growing “financial nihilism” is pushing more young investors toward riskier assets like crypto and prediction markets, as stagnant wages, rising debt and soaring house prices make traditional wealth-building feel out of reach. With a large share of younger investors sidelined from conventional markets, the shift could have implications for asset allocation, market behaviour and the effectiveness of monetary policy over time.

Forum experts outline 50 emerging “nature-based” investment opportunities as capital flows increasingly target climate, biodiversity and natural capital. From new asset classes to evolving market structures, the analysis highlights how investors can position for long-term value in a rapidly shifting landscape.

The economic cost of war in the Middle East is mounting, with ripple effects across energy markets, trade flows and global financial stability. Read this article to explore how rising geopolitical tensions are amplifying risks to inflation, growth and market volatility, and reshaping the global economy.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Kanni Wignaraja, Marc-André Franche and Azusa Kubota

March 20, 2026