Why financial health should be a global priority

Financial inclusion is rising, but financial resilience has not kept pace. Image: Jonas Leupe/Unsplash

Tamara Cook

Director, Office of the UN Secretary-General's Special Advocate for Financial Health (UNSGSA)- Financial inclusion is rising globally yet financial resilience remains stagnant for over half of adults.

- Policy-makers must shift focus from basic account access to comprehensive measures of long-term financial wellbeing.

- Building responsible digital ecosystems and fit-for-purpose savings tools is essential to strengthening household financial health.

By many measures, financial inclusion is rising. Seventy-five percent of adults in low- and middle-income economies have an account as of 2024, according to the latest Global Findex — an 80% increase since 2011. Usage is also up, with about 40% of adults now saving formally.

Unfortunately, financial resilience has not kept pace. Only 56% of adults in these economies say they could reliably access extra money within 30 days to cope with a shock — such as job loss, illness or an accident — a figure unchanged since the data was last collected in 2021.

This highlights a missing link between basic financial access and broader financial health, of which resilience is a core dimension. The G20’s Global Partnership for Financial Inclusion and the UN Secretary-General’s Special Advocate for Financial Health define financial health as “the extent to which a person or family can smoothly manage their current financial obligations and have confidence in their financial future.” In this framing, success is measured not only on access to and use of financial services, but also by people’s overall financial wellbeing.

The Global Findex survey captures several of these dimensions, including day-to-day financial stress and the ability to manage shocks. Here’s what the data show.

Financial worry cuts across income levels

Financial concerns are remarkably consistent across income levels, though they vary somewhat by region and country context. Thirty percent of adults cite monthly expenses as their top concern, and 26% identify medical expenses as their primary worry. Fourteen percent worry most about school fees or money for old age (see figure below on financial worries).

Monthly expenses and medical bills rank as the leading financial concern among both lower- and higher-income adults. This suggests that financial vulnerability is not confined to the poorest households, underscoring the need to assess financial health beyond income alone.

Adoption of financial health tools remains low

Despite widespread concern about these issues, uptake of products designed to manage financial risks remains low. Only about 10% of adults in low- and middle-income countries make payments to an insurance provider (excluding China, where more than half of adults do so). In many countries, insurers offer both traditional insurance and savings products, so these payments may not all represent insurance premiums. Low uptake may also reflect gaps in product availability and design.

Uptake of formal savings for old age is similarly low. Although 14% of adults in low- and middle-income countries (excluding China, where data was not collected) report worrying about income in old age, less than one in three save formally for this purpose. Limited incentives may help explain this pattern: just 9% of adults in these countries earn interest on formal savings (again excluding China, where more than half of formal savers receive interest).

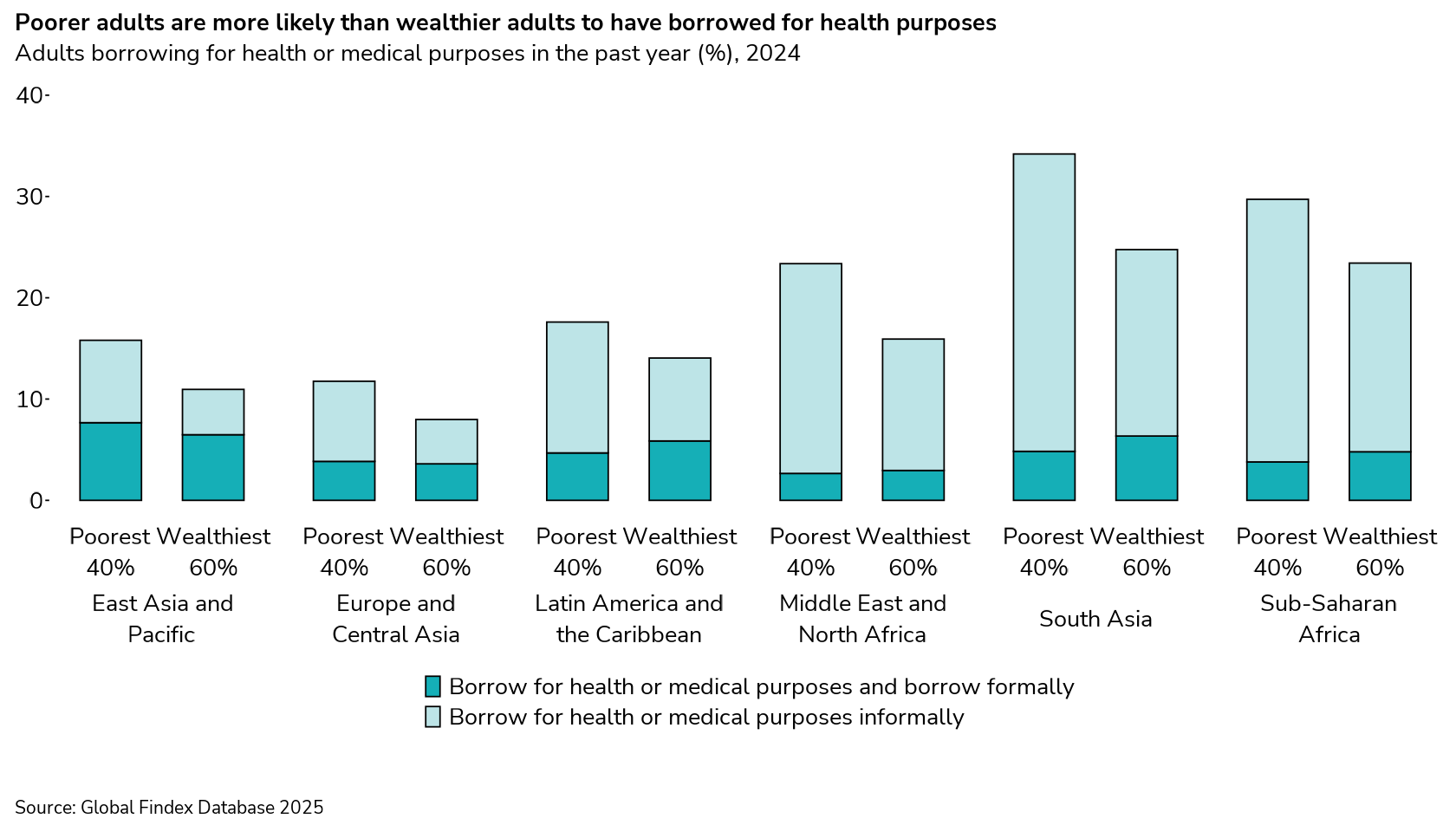

Formal borrowing to manage financial stress is also rare. Most borrowing for medical or business expenses is informal, especially for adults in the poorest households (see figure below on borrowing for health purposes), by household income and formal borrowing). So, too, is borrowing to cover monthly expenses, reflected in the 32% of adults who report buying groceries on credit.

Financial resilience through savings buffers remains a challenge

These patterns of coping with financial stress might help explain why financial resilience has remained unchanged at 56% since the Global Findex 2021 (see figure below on sources of emergency money).

Furthermore, just one-third of adults could cover more than two months of expenses if they lost their main source of income.

At the same time, Findex data also shows that people who rely on savings to manage shocks are more likely to be financially resilient. Yet competing financial pressures, from school fees to business expenses, can quickly erode even the most committed savers’ balances, and it’s understandable why increases in formal saving have not been sufficient to build resilience at scale. Overcoming those hurdles will require more fit-for-purpose savings and insurance solutions.

Responsible digital ecosystems can support resilience and financial health

Financial health requires not just access, but also greater use of diversified financial services, supported by an ecosystem that incentivizes digital transactions. That ecosystem is still incomplete. Although three-quarters of government payment recipients and half of private-sector wage earners in low- and middle-income countries receive funds into accounts, about half immediately withdraw the money in cash. Often this is because daily transactions, from groceries to small-business suppliers, still require cash. This limits opportunities to keep money in accounts and build savings buffers.

At the same time, expanding digital use carries risks. In fast-growing online markets, digital platforms can accelerate spending and encourage impulsive financial behaviour. Without strong consumer protection and thoughtful product design, digital tools can undermine, rather than strengthen, financial health. Fully digitalizing payment value chains — from suppliers to merchants to consumers — can strengthen financial resilience, but only when safeguards and incentives support saving and responsible use.

Advancing financial health therefore requires deliberate leadership. Expanding access remains essential for the 1.3 billion adults who still lack an account, but policy-makers and providers must go further — making financial health an explicit policy and business objective. This means aligning regulation, product design and digital ecosystems to help households manage everyday risks through simple insurance products, goal-based and interest-earning savings, pension solutions and responsible, affordable credit. With these elements in place, access can translate into stronger, financially healthier households.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Financial and Monetary Systems

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.