Venture capital is vital. But can it fund the next wave of innovation?

Venture capital has evolved from a niche financing mechanism into a central pillar of the global innovation economy. Image: Unsplash

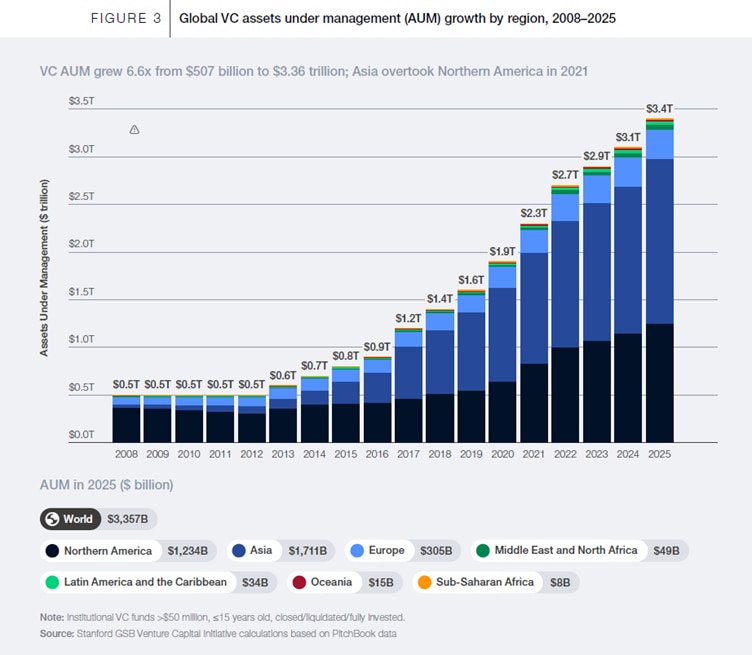

- With nearly $3.5 trillion in assets under management, venture capital has evolved from a niche financing mechanism into a central pillar of the global innovation economy.

- Companies are staying private for longer and traditional exits have slowed, locking up investment that should flow to the next generation of startups.

- A new report by the World Economic Forum and Stanford Graduate School of Business maps both the challenges the industry faces and the concrete solutions to address them.

Think about the 10 most valuable companies in the world. Seven of them – Nvidia, Apple, Alphabet, Microsoft, Amazon, Meta and Tesla – were once funded by venture capitalists willing to bet on an unproven idea. In the United States alone, companies that received early-stage venture backing before going public now account for 42% of total stock market value and 94% of all R&D spending by public companies founded in the last 50 years.

Since 2008, global venture capital assets under management have increased more than sevenfold, from $500 billion to nearly $3.5 trillion. In 2025 alone, global deal value reached an estimated $530 billion across almost 21,000 investments, with more than 250,000 companies having received venture funding worldwide over the past two decades.

A cycle under pressure

The venture model depends on a continuous cycle: investors back young companies, help them grow, and eventually sell their stakes through a public listing or acquisition.

The proceeds return to the limited partners who funded the original investments, who then recommit that capital to new funds backing the next generation of startups. That cycle is under real strain. Distributions to limited partners have fallen to historic lows, fund timelines have stretched well beyond their original horizons, and the capital that should be recycling into the next generation of startups remains locked up.

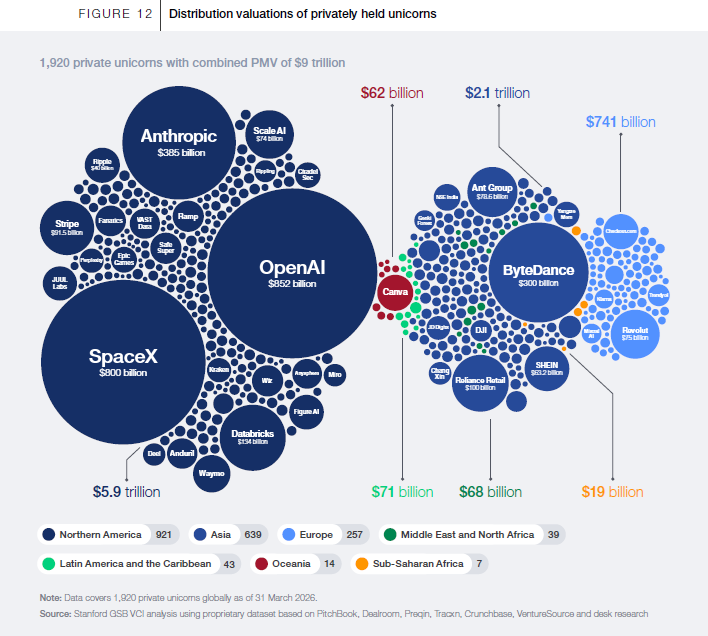

Today, around 1,920 venture-backed unicorns remain privately held globally, representing more than $9 trillion in collective valuation. An estimated $3.2 trillion in unrealized value sits in venture fund portfolios, including $1.7 trillion in funds launched in 2019 or earlier. Releasing even a portion of this value would return significant capital to limited partners, giving them the opportunity to invest in new vintages and support the next generation of companies.

Companies are staying private longer because private markets can now support their ambitions at scale. OpenAI’s latest round raised $110 billion, four times the size of the largest IPO in history. Late-stage rounds from crossover funds, sovereign wealth funds and growth equity firms now routinely match or exceed the proceeds of large IPOs.

Secondary markets: a new pillar of the ecosystem

One of the most significant structural developments in venture capital today is the rapid growth of secondary markets, which let existing investors in private companies cash out by selling their shares to other investors without waiting for an IPO or acquisition. What was once a niche instrument has become a core feature of the asset class. In 2025, secondary transaction volumes reached $106.3 billion, roughly one-third of US venture-backed exit value, compared to just 3% a decade ago.

This growth has naturally concentrated where liquidity is deepest. Today, the top 20 most-traded companies account for 86.4% of secondary transaction volume. Whether secondaries can broaden beyond these top names will determine whether they become a true source of liquidity for the asset class as a whole. New regulatory frameworks, including the PISCES initiative in the UK that completed its first trade on the London Stock Exchange in March 2026, and the DEAL Act in the US, are creating the legal foundations for deeper, more accessible private markets.

AI and new capital: a historic convergence

Artificial intelligence is moving faster, drawing in more capital and pulling in a more complex mix of investors than any previous technology cycle. In 2025, AI accounted for more than half of global venture deal value, and this concentration is intensifying. In Q1 2026, four of the five largest venture rounds ever recorded were closed by just four companies collectively raising $188 billion, representing 65% of all global venture investment in the quarter. The exit pipeline mirrors this concentration: The potential IPOs of SpaceX, OpenAI and Anthropic alone could generate more exit value than all US venture-backed IPOs since 2000 combined.

Funding rounds that once would have been left to public markets are now closing privately. The boundaries between venture capital, growth equity, sovereign wealth and corporate investment are shifting, bringing more capital, more patient capital and more strategically motivated capital into the ecosystem than ever before.

An agenda built for the moment

A new report by the World Economic Forum and Stanford Graduate School of Business, The Future of Venture Capital: Unlocking Liquidity and Growth, identifies five priorities for coordinated action by policy-makers and institutional investors to unlock liquidity and growth across the asset class.

Improve secondary market infrastructure. Secondary markets have grown rapidly, but liquidity remains concentrated among a small number of well-known companies. Expanding technology platforms, improving price discovery through better data-sharing and pricing benchmarks, and modernizing regulation can extend liquidity benefits across the wider ecosystem of companies and investors that need them most.

Mobilize institutional capital. Unlocking even a small share of the long-term capital held by institutional investors such as pension funds and insurers would meaningfully expand the venture capital base, and doing so requires modernizing the prudential and regulatory frameworks that currently constrain these allocations across several regions. European pension funds currently allocate a mere 0.12% of their total assets under management to venture capital and growth equity; increasing this allocation to a modest 1-2% would generate transformative capital flows into innovation finance.

Reduce regulatory friction. Cross-border complexity is one of the biggest drags on founders looking to build and scale across markets, and several jurisdictions are now moving to simplify and harmonize their regulatory regimes. The EU-Inc initiative, backed by over 13,000 signatures and now a formal legislative proposal, would allow startups to incorporate once and operate across all 27 EU member states.

Strengthen talent ecosystems. The recycling of talent from successful ventures is one of the most powerful compounding forces in innovation ecosystems. Founders and early employees who exit one company frequently start or back the next, creating a flywheel of capital, expertise and networks. Competitive capital gains treatment, well-designed stock-option taxation and startup visa programmes are essential building blocks for regions seeking to grow and retain their talent base.

Enable strategic government participation. The evidence shows that well-designed public capital, whether deployed through fund-of-funds structures or sovereign vehicles, can meaningfully accelerate ecosystem development when it targets market gaps, reinforces rather than distorts efficient allocation, and is built to evolve as private markets mature. The most effective programmes act as catalysts, multiplying private commitments and stepping back as ecosystems reach self-sustaining scale.

The venture capital industry has shown what is possible when capital, talent and ambition align. But the next decade will be defined less by the industry's ability to deploy capital than by its ability to recycle it, releasing the more than $3 trillion of unrealized value locked in today's portfolios so it can fund the next wave of innovation. The economies that act on this agenda first will define where the next generation of leading companies is built, financed and scaled.

How the Forum helps leaders understand change in global financial systems

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Innovation

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Genevieve Bennett

August 5, 2026