From funding to deployment: What Asia’s investment model gets right

The Global Innovation Index 2025 outlines six economies from Asia in the top 25, with Singapore leading across 10 of 28 innovation indicators. Image: Mike Enerio/Unsplash

- Asia’s integrated investment model rapidly converts early-stage innovation into scaled solutions by connecting capital with policy.

- Western innovation ecosystems generate world-class research but lack the coordinated architecture needed for widespread market deployment.

- How promising ideas become scalable impact is a key focus at the World Economic Forum’s Annual Meeting of the New Champions, also known as Summer Davos, in China from 23–25 June.

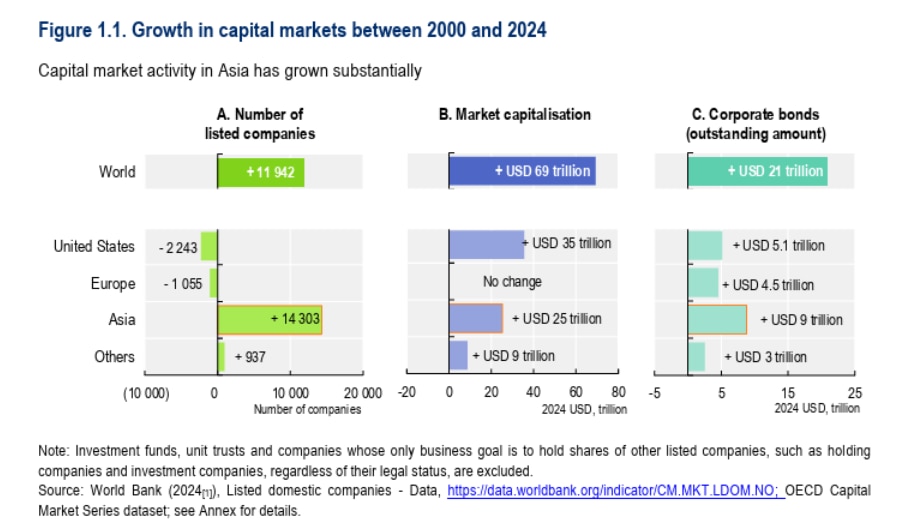

Asia is now home to 55% of the world’s listed companies and contributes over 60% of global growth. In 2025, Hong Kong overtook Switzerland as the world’s largest cross-border wealth hub for the first time, with $2.9 trillion in assets. This milestone reflects a deeper reordering of where global capital flows and who it flows towards. The Global Innovation Index 2025 outlines six economies from Asia in the top 25, with Singapore leading across 10 of 28 innovation indicators and China hosting 24 of the top 100 innovation clusters.

These figures are the output of investment ecosystems deliberately engineered to close the gap between a funded idea and a deployed one. So, what’s driving this? What structural conditions allow Asia to convert innovation into scaled solutions so rapidly – even amid geopolitical instability and the slowest global R&D investment growth since 2010?

The capital stack: Intentional by design

Across much of Asia, the focus is not just on funding companies but on building ecosystems where capital, policy and market access are connected from the outset, with a clearly defined end goal. The OECD’s first Asia Capital Markets Report finds that Asian companies use debt to finance real investment to a greater extent than companies from other regions, with capital directed towards deployment, not just financial returns.

China illustrates how this architecture operates at scale. State funding leads and private capital follows, with central grants derisking early-stage opportunities, local government equity anchoring emerging technologies, and state-owned-enterprises providing debt at more favourable rates than private markets. Government procurement demonstrates commercial viability and the 15th Five-Year Plan explicitly targets foreign capital in manufacturing, high technology and modern services. The stack is open to outside capital, provided it flows to the right sectors.

But top-down orchestration alone does not explain Asia’s results. India and Vietnam have both been innovation overperformers for 15 consecutive years, and demonstrate a different model driven by founders, angel networks and deep domestic investor participation. India registered a record 367 IPOs in 2025, proof that bottom-up approaches are substantial on their own and can also complement state-backed programmes.

Hong Kong shows how this extends to the exit side of the cycle. Under CEO Bonnie Chan, HKEX introduced Chapter 18C, a listing regime for pre-revenue specialist technology companies that expanded weighted voting rights and shortened the IPO settlement cycle from five days to two. When early-stage investors can see a clear pathway from funding to public listing, capital flows more freely into the front end. As Chan noted in April 2026, Hong Kong is seeing very good momentum on both the supply and demand sides for IPOs, with HKEX’s pipeline exceeding 300 companies.

The Western contrast: A structural gap

Western innovation systems produce world-class research and deep pools of early-stage capital. What is structurally weaker is the link between funding and deployment. In the United States, venture capital optimizes for financial returns on fund-cycle timelines, corporate R&D bends to quarterly earnings pressure, and public policy responds to unpredictable political cycles. These systems operate in largely separate lanes, resulting in solutions routinely stalling in what might be called the valley of deployment, where they are funded and validated, but are unable to reach markets at scale because the ecosystem actors are not coordinated.

For early-stage ventures, this is where promising solutions go to stall. A start-up with a validated product and willing investors can spend years navigating the gap between pilot and commercial deployment because the ecosystem around it – including procurement pathways, regulation and market access – was never designed to pull it through.

The US added $35 trillion in market capitalization between 2000 and 2024, but lost over 2,200 listed companies in the same period. Capital is concentrated into fewer firms and narrower sectors rather than broadening the base of companies converting innovation into deployment.

The bottleneck holding back global innovation is no longer the supply of ideas or capital – it is adoption at scale.

”In Europe, the challenge has a different shape but a similar effect. A start-up expanding from one EU member state to another faces a patchwork of tax codes, labour regulations, licensing requirements and compliance systems. The European Commission estimates that regulatory compliance costs for start-ups can reach 7% of turnover, roughly double what US start-ups typically spend. By Series C, roughly 30% of European tech start-ups are headquartered outside Europe entirely.

Western systems generate category-defining companies and exceptional research. But the connective tissue between innovation funding and deployment at scale is structurally weaker. That gap grows more consequential as the window for deploying solutions in climate, health and food systems narrows.

What can be borrowed

Different governance structures, political economies and market dynamics make replicating Asia’s model impractical. But there are three specific design principles that are portable.

- Strategic demand planning: policies that create clear deployment pathways rather than leave capital to speculate on market readiness. China’s shift from output targets to deployment metrics is instructive as a design choice.

- Allocation discipline: maintaining diversified investment pathways across sectors where deployment infrastructure exists or can be built, such as food systems, energy, advanced manufacturing and health, rather than letting a single narrative absorb all available capital.

- End-to-end ecosystem design: listing environments, procurement pipelines, cross-border market access and partnership structures designed around deployment milestones from the start, not bolted on once a company is stuck between pilot and scale.

The bottleneck holding back global innovation is no longer the supply of ideas or capital – it is adoption at scale. Closing that gap requires the same connector logic that underpins Asia’s success, achieved by building ecosystems that link early-stage ventures with partners, customers, capital and demand from the outset, rather than after the fact.

Through initiatives like UpLink, the World Economic Forum’s early-stage innovation engine, thematic ecosystems connect entrepreneurs, investors and industry leaders to accelerate solutions in areas where markets are primed for change – the same conditions that have allowed Asia to convert innovation into deployment at scale. The question for policy-makers and investors elsewhere is not whether these principles work. It is whether they are willing to build the systems that apply them.

The Forum is spotlighting how innovation moves from breakthrough to scale to impact ahead of Summer Davos in China, 23–25 June 2026. Follow the latest.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Banking and Capital Markets

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.