India's currency exchange: will Modi's plan work?

Rogoff discusses the controversy over India’s currency exchange. Image: REUTERS/Adnan Abidi

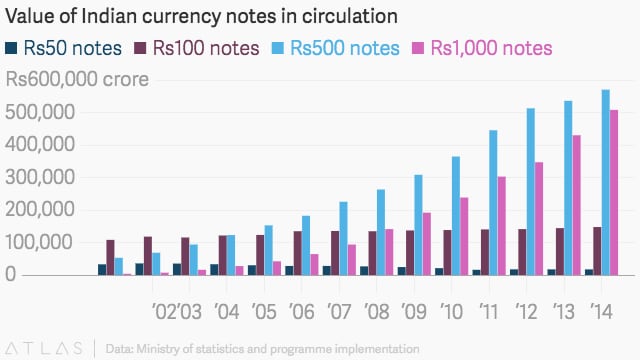

On the same day that the United States was carrying out its 2016 presidential election, India’s Prime Minister, Narendra Modi, announced on national TV that the country’s two highest-denomination notes, the 500 and 1000 rupee (worth roughly $7.50 and $15.00) would no longer be legal tender by midnight that night, and that citizens would have until the end of the year to surrender their notes for new ones. His stated aim was to fight “black money”: cash used for tax evasion, crime, terror, and corruption. It was a bold, audacious move to radically alter the mindset of an economy where less than 2% of citizens pay income tax, and where official corruption is endemic.

Motivation same as in curse of cash

Is India following the playbook in The Curse of Cash? On motivation, yes, absolutely. A central theme of the book is that whereas advanced country citizens still use cash extensively (amounting to about 10% of the value of all transactions in the United States), the vast bulk of physical currency is held in the underground economy, fueling tax evasion and crime of all sorts. Moreover, most of this cash is held in the form of large denomination notes such as the US $100 that are increasingly unimportant in legal, tax-compliant transactions. Ninety-five percent of Americans never hold $100s, yet for every man, woman and child there are 34 of them. Paper currency is also a key driver of illegal immigration and corruption. The European Central Bank recently began phasing out the 500 euro mega-note over these concerns, partly because of the terrorist attacks in Paris.

But setting and implementation is vastly different

On implementation, however, India’s approach is radically different, in two fundamental ways. First, I argue for a very gradual phase-out, in which citizens would have up to seven years to exchange their currency, but with the exchange made less convenient over time. This is the standard approach in currency exchanges. For example this is how the European swapped out legacy national currencies (e.g the deutschmark and the French franc) during the introduction of the physical euro fifteen years ago. India has given people 50 days, and the notes are of very limited use in the meantime. The idea of taking big notes out of circulation at short notice is hardly new, it was done in Europe after World War II for example, but as a peacetime move it is extremely radical. Back in the 1970s, James Henry suggested an idea like this for the United States (see my October 26 new blog on his early approach to the big bills problem). Here is what I say there about doing a fast swap for the United States instead of the very gradual one I recommend:

“(A very fast) swap plan absolutely merits serious discussion, but there might be significant problems even if the government only handed out small bills for the old big bills. First, there are formidable logistical problems to doing anything quickly, since at least 40% of U.S. currency is held overseas. Moreover, there is a fine line between a snap currency exchange and a debt default, especially for a highly developed economy in peacetime. Foreign dollar holders especially would feel this way. Finally, any exchange at short notice would be extremely unfair to people who acquired their big bills completely legally but might not keep tabs on the news.

In general, a slow gradual currency swap would be far less disruptive in an advanced economy, and would leave room for dealing with unanticipated and unintended consequences. One idea, detailed in The Curse of Cash, is to allow people to exchange their expiring large bills relatively conveniently for the first few years (still subject to standard anti-money-laundering reporting requirements), then over time make it more inconvenient by accepting the big notes at ever fewer locations and with ever stronger reporting requirements.

Second, my approach eliminates large notes entirely. Instead of eliminating the large notes, India is exchanging them for new ones, and also introducing a larger, 2000-rupee note, which are also being given in exchange for the old notes.

My plan is explicitly tailored to vast economies

The idea in The Curse of Cash of eliminating large notes and not replacing them is not aimed at developing countries, where the share of people without effective access to banking is just too large. In the book I explain how a major part of any plan to phase out large notes must include a significant component for financial inclusion. In the United States, the poor do not really rely heavily on $100 bills (virtually no one in the legal economy does) and as long as smaller bills are around, the phase out of large notes should not be too much of a problem, However, the phaseout of large notes is golden opportunity to advance financial inclusion, in the first instance by giving low income individuals access to free basic debt accounts. The government could use these accounts to make transfers, which would in turn be a major cost saving measure. But in the US, only 8% of the population is unbanked. In Colombia, the number is closer to 50% and, by some accounts, it is near 90% in India. Indeed, the 500 rupee note in India is like the $10 or $20 bill in the US and is widely used by all classes, so India’s maneuver is radically different than my plan. (That said, I appreciate that the challenges are both different and greater, and the long-run potential upside also much higher.)

Indeed, developing countries share some of the same problems and the corruption and counterfeiting problem is often worse. Simply replacing old notes with new ones does have a lot of beneficial effects similar to eliminating large notes. Anyone turning in large amounts of cash still becomes very vulnerable to legal and tax authorities. Indeed that is Modi’s idea. And criminals have to worry that if the government has done this once, it can do it again, making large notes less desirable and less liquid. And replacing notes is also a good way to fight counterfeiting—as The Curse of Cash explains, it is a constant struggle for governments to stay ahead of counterfeiters, as for example in the case of the infamous North Korean $100 supernote.

Will Modi’s plan work? Despite apparent huge holes in the planning (for example, the new notes India is printing are a different size and do not fit the ATM machines), many economists feel it could still have large positive effects in the long-run, shaking up the corruption, tax evasion, and crime that has long crippled the country. But the long-run gains depend on implementation, and it could take years to know how history will view this unprecedented move.

The goal is a less-cash society not a cashless one

In The Curse of Cash, I argue that it will likely be necessary to have a physical currency into the far distant future, but that society should try to better calibrate the use of cash. What is happening in India is an extremely ambitious step in that direction, of a staggering scale that is immediately affecting 1.2 billion people. The short run costs are unfolding, but the long-run effects on India may well prove more than worth them, but it is very hard to know for sure at this stage.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

India

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

John Letzing

July 31, 2026