Going cashless: is India ready for digital?

India is gearing up towards going cashless. Image: REUTERS/Adnan Abidi

Bhaskar Chakravorti

Senior Associate Dean, The Fletcher School of Law and Diplomacy, Tufts University“Time has come for everyone, particularly my young friends, to embrace e-banking, mobile banking and more such technology”. So said Narendra Modi, doubling up as the nation’s digital evangelist-in-chief. Appropriately, he “said” this via a tweet.

PM Modi’s November 8 surprise demonetising Rs 500 and Rs 1,000 notes, effectively took 86 per cent of cash out of circulation in an economy that is close to 90 per cent reliant on cash. Unsurprisingly, chaos has ensued. And e-wallet companies, Paytm, Mobikwik and Freecharge have experienced a nice bump. Global payments technology players are enjoying a nice “buy” recommendation from analysts.

Meanwhile, the buying has stalled at kirana stores and subzi mandis around the country. Supply chain transactions, real estate deals and even wedding projects have been frozen. Consumers are coping with frustrating lines, inconsistent information and empty ATMs. The crisis has been hardest on the poor.

Disruption is fashionable in digital circles, but usually the target of disruptive moves is a lazy incumbent. Disrupting the consumer is generally not cool. The demonetisation disruption — and the PM’s nudge towards cashlessness — provides an opportunity to ask fundamental questions.

Does using cash cost money? If so, how does India fare in comparison with the rest of the world?

Cash, alas, is not free; its use comes at a significant cost. I have studied the cost of cash in over 70 countries, in research outlined in a recent article in the Harvard Business Review, titled ‘The Countries that Would Profit Most from a Cashless World’. Typically, these costs include costs to consumers (including ATM fees, money changers, etc. and the implicit cost of time spent to collect cash), costs to businesses (for handling cash and ensuring its security and transportation to safe locations), costs to banks and other institutions (for moving and storing cash, operating and maintaining ATMs) and costs to the government (from foregone tax revenues and because of costs of printing money). India’s costs of cash score among the highest in a global comparison.

We found that the costs of cash vary widely across countries. These costs do not correlate with levels of economic or political development. Consider a few tidbits: The costs of cash to consumers are high in some of the world’s most populous countries. Unsurprisingly, cost to Indian consumers is among the highest. When weighted for population, India fares poorly in terms of ATM access compared to even lesser-developed countries, such as Kenya, Nigeria, or Egypt. Moreover, smaller cities in India have larger problems. Long before the current crisis, we found that residents of Delhi spent 6 million hours and Rs. 9.1 crore to obtain cash, while residents of Hyderabad spent 1.7 million hours and Rs 3.2 crore to do the same. Hyderabadi consumer costs were about twice as high as that of Delhiites on a per capita basis. ATM maintenance costs to banks are disproportionately high in many developing countries, particularly in sub-Saharan Africa and Latin America, with myriad security and infrastructure challenges, as well as in large, sparsely populated countries, such as Canada, Russia, and Australia, where the logistics are costly. On balance, India fares well on this score.

The cost of cash to the government in terms of foregone tax revenues is highest in developing countries, with their shadow economies as large as 30-44 per cent of GDP. While India was not among the worst offenders, its costs to the government are high; India’s tax gap has been estimated at two-thirds of overall taxes owed.

So, Modi is onto something; is it time to follow his nudge and go cashless?

Despite the high costs of cash, telling people to go cashless is putting the cart before the proverbial horse. The horse in this case is the digital infrastructure and establishing a threshold of trust in the system. Money requires two parties across a transaction to believe in it. If there is a shadow of doubt that one party is not ready to go digital, the other will only deal in cash.

India’s digital state, unfortunately, does not engender the trust needed for cashlessness to take hold in a meaningful way. Despite a billion mobile phone subscriptions, just about 30 per cent of Indian subscribers use smartphones. A little over a third of the population has internet access. India lacks the infrastructure to reliably expand access. Connections are patchy and there is great disparity in connectivity: Seventy per cent of those with mobile internet access are in cities; only 17 per cent of Indian women use the internet, according to the Pew Research Center. With women responsible for much of household purchases, this does not provide a strong foundation for the spread of digital payments.

Cold hard cash, the kind that has not been demonetised, is acceptable everywhere. We learnt in our study that India stood out in its cash intensity even among developing countries. Consider: The value of notes and coins in circulation as a percentage of GDP in India was 12.04 per cent, compared to 3.93 per cent in Brazil, 5.32 per cent in Mexico, and 3.72 per cent in South Africa. The ratio of money held in bills and coins to the amount held in demand deposit and savings accounts in India was 51 per cent, as compared to Egypt (29.3 per cent), South Africa (8.9 per cent), and Mexico (8.7 per cent).

Our consumer research partner, ICE 360° found that most consumers see three main benefits of cash: Self-control, speed and guarantee of exact payment. Of course, cash has the advantages of being untraceable and universally accepted (except in some circumstances). For many users, cash gives a sense of security and for others it conveys a sense of independence from government oversight. On the flipside, digital alternatives are not entirely fool-proof as yet. It will take a lot to disentangle the “cash equilibrium” and re-build a new cashless equilibrium.

Should Modi give up on cashlessness?

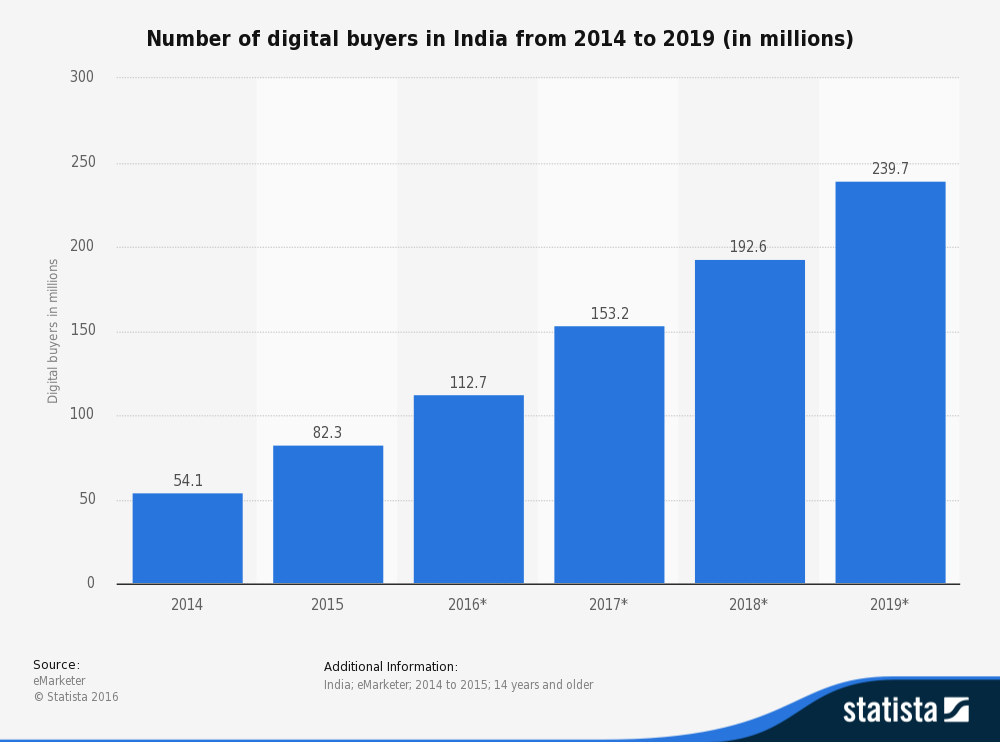

According to Google India and The Boston Consulting Group, by 2020, digital transactions will happen at 10 times the current level. Demonetisation may serve as the catalyst. But cash will stubbornly resist wholesale digital disruption. We should plan for a slow erosion of cash addiction at best.

At the same time, let’s not demonise the demonetiser. Modi’s war on cash in a high cost environment follows international precedent. Singapore, for example, withdrew its largest currency two years ago. The European Central Bank recently eliminated the 500-euro bank note. South Korea plans to eliminate paper money by 2020. The key is that each of these countries had a digital strategy in place.

The demonetiser’s dilemma is a real one. Smoking out the underground economy — at least the parts not in gold or in offshore accounts — is commendable. Yet, a switch to digital in a digitally under-evolved country such as India is anything but digital — you cannot go directly from zero to one. It is bound to be a journey of many small increments. This journey should have been anticipated. The pain to the common man should have been better managed. Digital and physical infrastructure and logistics should have been in place in advance of the November surprise.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

India

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Rebecca Geldard

May 19, 2026