Circularity: A key enabler to reach net-zero in cement and concrete

Net-zero in the cement and concrete industry is achievable through circularity. Image: Getty Images

Yvonne Leung

Private Sector and Philanthropy Engagement Manager – Forest Future Alliance, World Economic ForumSebastian Reiter

Partner, McKinsey & CompanyListen to the article

- Carbon emissions in the cement industry will reach 3.8 billion tons of CO₂ a year by 2050, versus 2.7 billion tons today.

- But cement and concrete are absolutely essential for construction and the wider economy.

- Circularity could help solve this problem by keeping emissions to a minimum while enabling the construction of homes and infrastructure.

Cement, and by extension concrete, is the linchpin of the built environment. Global demand for it has nearly tripled in the last 20 years, and estimates suggest it will continue to grow through 2050 if no action is taken.

But despite its ubiquity, cement’s surrounding economy has a significant environmental impact, accounting for approximately 7% of global CO₂ production.

The sector is difficult to decarbonize due to both the emission of CO₂ during the chemical process and the high volume of energy required to make cement.

Without action, carbon emissions in the cement industry will reach 3.8 billion tons of CO₂ a year by 2050 in a business-as-usual scenario, versus approximately 2.7 billion tons in 2020. This is a major obstacle in the global effort to limit global warming to 1.5°C.

Circularity is one option to deal with this issue. It can help by both addressing increasing emissions by reducing the need for the production of new virgin components, and potentially holds further benefits such as cost-savings or offering a solution for waste legacy.

Making circularity work in cement for net-zero

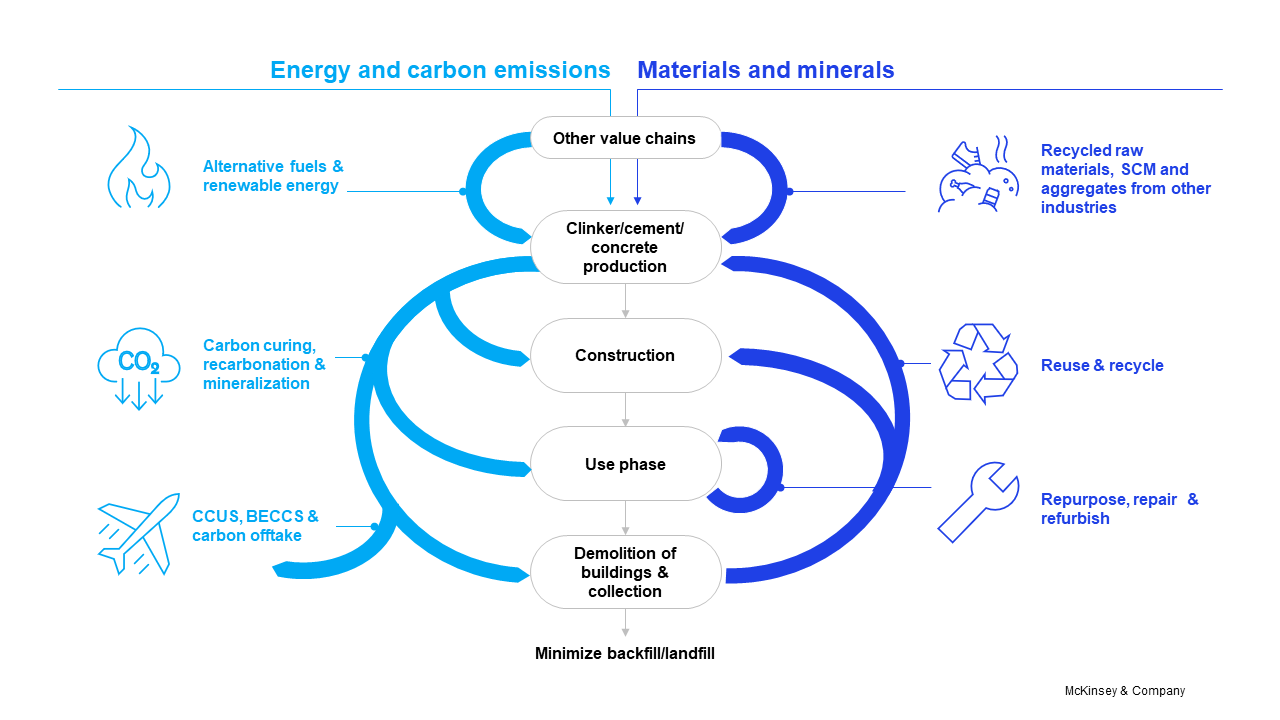

Circularity in concrete and cement has two angles. One is the recirculation of materials or minerals from waste (of the own value chain or from other value chains). The other is the recirculation of energy (through alternative fuels or renewable energy), or of captured emissions.

Players within the building and construction ecosystem can take immediate action to help the industry reach its decarbonization targets by deploying three circularity strategies: redesign, reduce and repurpose.

Redesign buildings and infrastructure

Redesign requires us to rethink the way buildings and structures are used to reduce the total volume of materials needed.

Modular design and design for deconstruction — a closed cycle of use and reuse — can contribute to circularity. Designers and architects reduce the need for new structures by harnessing existing structures through repairs or refurbishment.

This approach requires a shift in mindset toward a more customer-oriented perspective to address the needs of end users. For example, modular design can fulfill end-users need for flexible spaces that can be readily adapted to the purpose of use.

Reduce emissions of materials

Alternative fuels from waste can help tackle both carbon emissions and waste legacy.

The Global Cement and Concrete Association (GCCA) net-zero roadmap predicts more than 20% of energy for cement and concrete production will come from alternative fuels such as biomass, which includes industrial, municipal and agricultural waste, by 2030, and more than 40% by 2050.

Renewable power and waste heat recovery present further opportunities. Energy recovery is a real opportunity for countries with high plastic waste leakage, because plastic waste can be a key source for alternative fuels.

Byproducts of other industries can be directly recycled into the concrete and cement value chain, making the industry part of the solution to waste treatment. For example, raw materials can be extracted from mineral waste or the ashes of incinerated fuels through coprocessing. Blast furnace slag from the steel industry and fly ash from power plants are currently used in the cement production process.

These technologies can generate savings in landfill taxes for waste producers and cost benefits on material input in cement and concrete manufacturing. Replacing clinker, a component in the production of cement, also helps to reduce CO₂ emissions, as around 830kg of CO₂ is emitted per ton of clinker produced.

Another tactic to create circularity loops within the value chain is using recycled concrete paste generated from construction and demolition waste (CDW) as supplementary cementitious material. Currently, only one-third to two-thirds of CDW generated is recycled, primarily for use as low-quality aggregates in road construction. Digital solutions, recycling services and collaboration across the industry can help overcome such challenges.

Repurpose captured carbon

CO₂ emissions captured from production processes can be reintroduced into the value chain — for example, during the production of recycled clinker (mineralization) or fresh concrete (carbon curing). A significant amount of CO2 is absorbed by concrete structures during their lifetime (recarbonation).

A significant amount of CO₂ is absorbed by concrete structures during their lifetime. The remaining carbon captured during the process can be stored or used for other purposes. Carbon capture, utilisation and storage (CCUS) represents the biggest decarbonization lever on the path toward net zero, creating a massive opportunity for innovation.

In fact, CCUS projects at advanced stages of planning represent a total estimated investment of more than $27 billion, almost doubling commissioned projects since 2010.

How stakeholders can take action for net-zero

Now is the time for the industry to translate these strategies into opportunities for sustainable value creation and growth. Some manufacturers are still facing challenges to deploy circularity solutions at scale — for example, because of the local conditions and varying regulations of landfill, waste treatment and product standards.

With the right approach, players across the value chain can help unlock both decarbonisation potential and additional value pools from circularity solutions. Applying one or both of the following approaches presents potential business opportunities.

Focus on materials for production

Companies could invest in new technologies to recycle and decarbonize construction and demolition waste or other materials. This approach also includes taking a broader perspective on materials and exploring alternative building materials by partnering and collaborating with other industries.

Respond to evolving consumer preferences

Another option is to explore customer needs for each material and step across the value chain. Stakeholders range from designers to construction companies to end users. This comprehensive perspective could identify opportunities for new business models such as “building materials as a service” — for example, precast building modules could be provided to customers in a lease-like mechanism for flexible use.

The World Economic Forum is joining forces with McKinsey & Company to bring a full understanding of the economics, the costs and the potential benefits of the main circularity levers and present a compelling business case for each of the stakeholders to engage in this critical transition. In line with that goal, the Forum builds upon its collaboration with key industry stakeholders, including GCCA as co-lead of the Mission Possible Partnership’s (MPP) Concrete Action for Climate (CAC) initiative.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

COP28

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Circular EconomySee all

Clemence Schmid

July 23, 2026