Emerging Asia faces a post-COVID inequality trap. Here's how to avoid it

Emerging Asia must act now to ensure an equitable recovery from the pandemic Image: Unsplash/Florian Wehde

Listen to the article

- Emerging Asia is in danger of falling into an inequality trap as it recovers from the pandemic.

- The region's poorest have been hit hardest by a reduction in their incomes and a lack of access to credit.

- Here are 3 ways authorities can restore some balance.

There are no elements of the global economy that have escaped the impact of the recent pandemic. From central bank chiefs to prudent individual savers, all of us have been subject to the forces of financial change.

The looming inequality trap over Emerging Asia

‘Emerging Asia’ (defined by the IMF as comprising China, India, Indonesia, Malaysia, the Philippines, Thailand and Viet Nam) is in danger of falling into an inequality trap for the following three reasons:

1. Financially disadvantaged people have been heavily affected by the pandemic.

2. Those people worst hit by the crisis now have reduced access to credit .

3. As a result, they are being forced to use unregulated vendors.

These three factors will be a concern to legislators and governments across Emerging Asia, as many economies begin to look beyond the pandemic.

The uneven impact of the global health crisis on Emerging Asia has challenged real disposable incomes and hit the region’s poorest the hardest. In South East Asia specifically, The Asian Development Bank estimates that the pandemic has pushed 4.7 million people into poverty and has destroyed over 9 million jobs.

The lack of access for poorer income households to more formal credit lines is highlighted by a recent Economist Impact report analysing COVID-19’s impact on personal finance in Asia. It shows that the countries experiencing the largest increases in household debt in 2020 were all high-income economies, with the exception of China (which has a rapidly-growing mortgage sector).

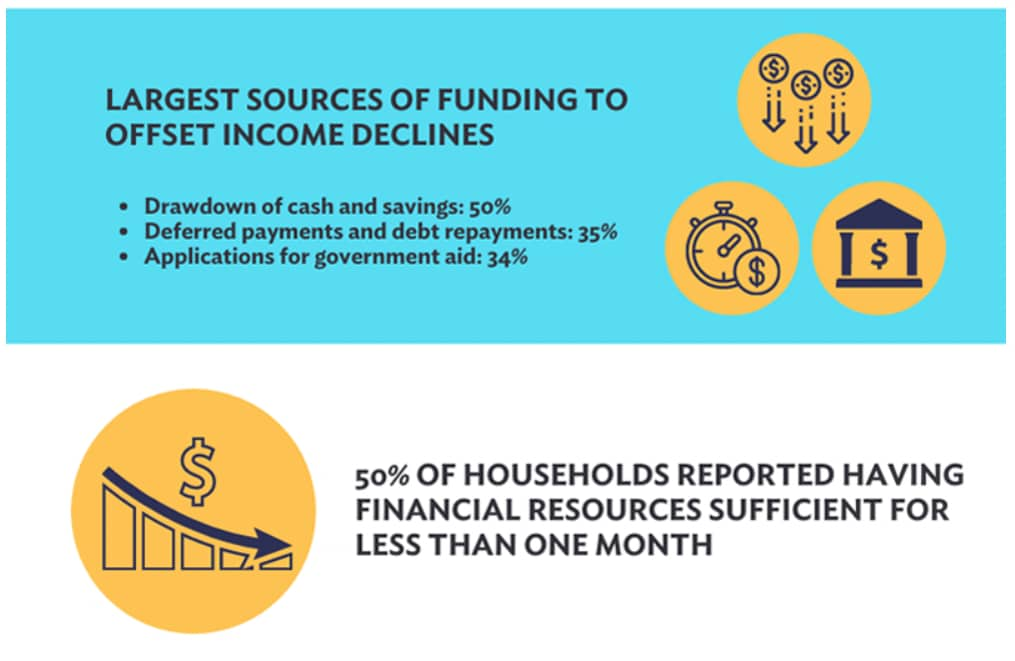

A separate OECD study of ASEAN countries revealed that half of the households that suffered a negative income shock resorted to drawing down on their savings, while more than a third deferred payments and debt repayments and a similar proportion sought government aid. This dramatic shift will have far-reaching consequences for the region’s poorest, many of whom are now having to confront the fact that they cannot access credit like before.

In this new scenario, financially squeezed consumers are often left with little choice but to seek financial relief from black-market sources. These traditionally offline operators offer predominantly unregulated, unsecured, and unfavourable financial solutions to severe debt problems. The increasing popularity of 'buy now pay later' products also present a hazard, with many of these products targeting younger, less financially savvy consumers.

Ensuring even recovery for Emerging Asia and ASEAN

If an economy is represented as a human body, the money flowing through that economy is its blood. Put simply, people need access to money if an economy is to remain healthy. In many cases across Emerging Asia, the economic patient is sick – and governments and regulators need to act quickly.

In many cases they have sprung into action, delivering elevated levels of public spending to cushion some citizens from negative pandemic-related impacts. Countries have rolled out large-scale fiscal and monetary packages. These measures are designed to stimulate the economy, ensure a minimum level of income security and protect businesses, especially SMEs.

The scale of the effort is outlined by data from Singapore’s ISEAS–Yusof Ishak Institute. It shows that ASEAN countries had authorised pandemic stimulus packages of $730 billion at the height of the pandemic in 2021. That is the equivalent of 7.7% of the region’s GDP. But what else can authorities do to ensure a less uneven recovery and ensure protection is offered to those who need it? Here are three options.

1. Promote digital adoption: The pandemic has necessitated the use of digital tools and platforms as a means to resolve health challenges. The democratisation of information and services would further open up access to resources such as financial services. A McKinsey paper on the opportunity for Asia to harness technology for growth suggests that the region (including Emerging Asia) has taken a lead in social commerce – the process of selling products directly via social media and the COVID-19 pandemic has simply accelerated adoption.

2. Champion the importance of financial literacy: Providing individuals with the tools to understand and responsibly use financial services is an important part of any response to the global health crisis. In a paper written on financial literacy in Indonesia for the Asian Development Bank, the three academic authors concluded: “A key policy lesson from the study is that it is advisable for national and international efforts in poverty reduction to pay more attention to improving and enhancing an individual’s financial knowledge and skills.”

3. Create a level playing field: Regulators now have an opportunity to create an equitable environment that offers protection and transparency. Solid regulation is also a form of protection. For example, new market entrants should be subject to a common regulatory approach – shielding the most vulnerable consumers should be a post-pandemic priority.

There is little doubt that the global pandemic will have long-term impacts on populations in Emerging Asia. However, the crisis has presented new opportunities to embrace fresh approaches to healthcare delivery and access to financial services. The deep impact on the region’s poorest, the reduction in credit access to those communities and the threat of unregulated operators means we will need closer cooperation between the public and private sectors if we are to avoid deeper inequality post-pandemic.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

COVID-19

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Forum in FocusSee all

Gayle Markovitz and Maxwell Hall

April 7, 2026