Africa's iron ore production is booming but it needs a parallel steel strategy

As Africa's iron ore production grows, the continent also needs to develop its steelmaking sector. Image: Getty Images/serts

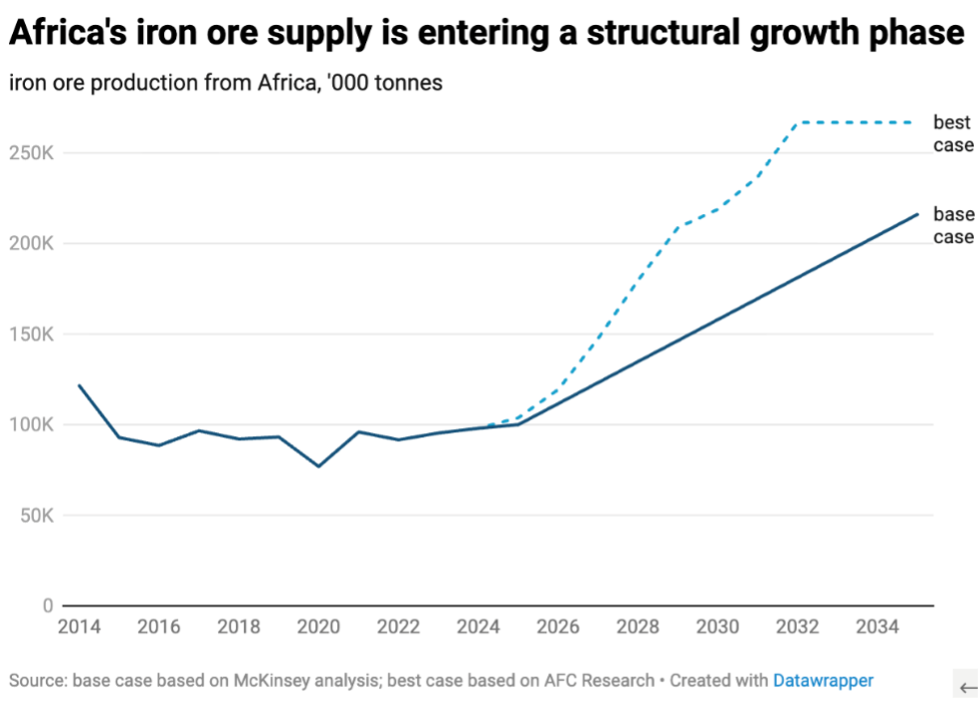

- Iron ore production in Africa is set to rise, with expectations that it will exceed 200 million tonnes annually by the early 2030s.

- It can be used to produce steel, which underpins transport systems, energy infrastructure, housing and manufacturing.

- Alongside investment in the iron ore industry, Africa should boost domestic steelmaking to create a more competitive and resilient industrial base.

After a decade of supply disruption following the Ebola crisis in West Africa, the continent’s iron ore production has recovered to roughly 100 million tonnes per year. It is now entering a new phase of growth that will be structural, not cyclical, because it relies on long-term and approved mine development projects and investment plans across Africa.

By the early 2030s, African output could exceed 200 million tonnes annually. This will be driven largely by the ramp-up of the Simandou project in Guinea to around 120 million tonnes per year, alongside production growth in Sierra Leone, Liberia, Mauritania, Algeria and other Guinean projects.

The scale is significant. But the real story is not about iron ore, it’s about steel.

An iron ore boom without a steel strategy

While Africa's iron ore supply is accelerating, its production of steel – which is made by heating iron ore and adding carbon – has grown only modestly, from around 15 million tonnes in 2014 to just over 26 million tonnes in 2024.

According to the CRU Group, most of this production is based on electric arc furnace (EAF) technology, which uses scrap metal. Primary and integrated ore-based steelmaking, on the other hand, remains limited and geographically fragmented in Africa.

This market structure did not emerge by accident. EAF-based production requires lower upfront capital, can operate at smaller scale, has a much lower carbon footprint and adapts more easily to fragmented and volatile demand.

In markets where industrial and infrastructure offtake remains dispersed, EAF can be practical and efficient. It allows producers to supply steel products without the heavy fixed costs of integrated manufacturing complexes. But this model really only addresses immediate demand gaps, rather than establishing a durable, regionally integrated industrial base.

Scrap availability is tightening as major exporting economies retain more material to meet their own decarbonization and industrial objectives. As supply constraints intensify, scaling production of flat steel (which is essential for automotive, machinery and appliance manufacturing) will require greater access to ore-based metallics.

Globally, flat products already rely more heavily on higher-grade iron ore than on scrap alone, as tighter quality specifications cannot be met consistently with high scrap content. In Africa, this challenge is compounded by limited capacity to remove rubber, coatings and non-ferrous contaminants from scrap, which affects quality control and increases reliance on imported higher-grade metal.

With access to high-grade ore, natural gas and affordable – and, increasingly, renewable – power, Africa is well positioned to produce low-carbon iron ore for higher-quality steelmaking.

Africa's critical materials

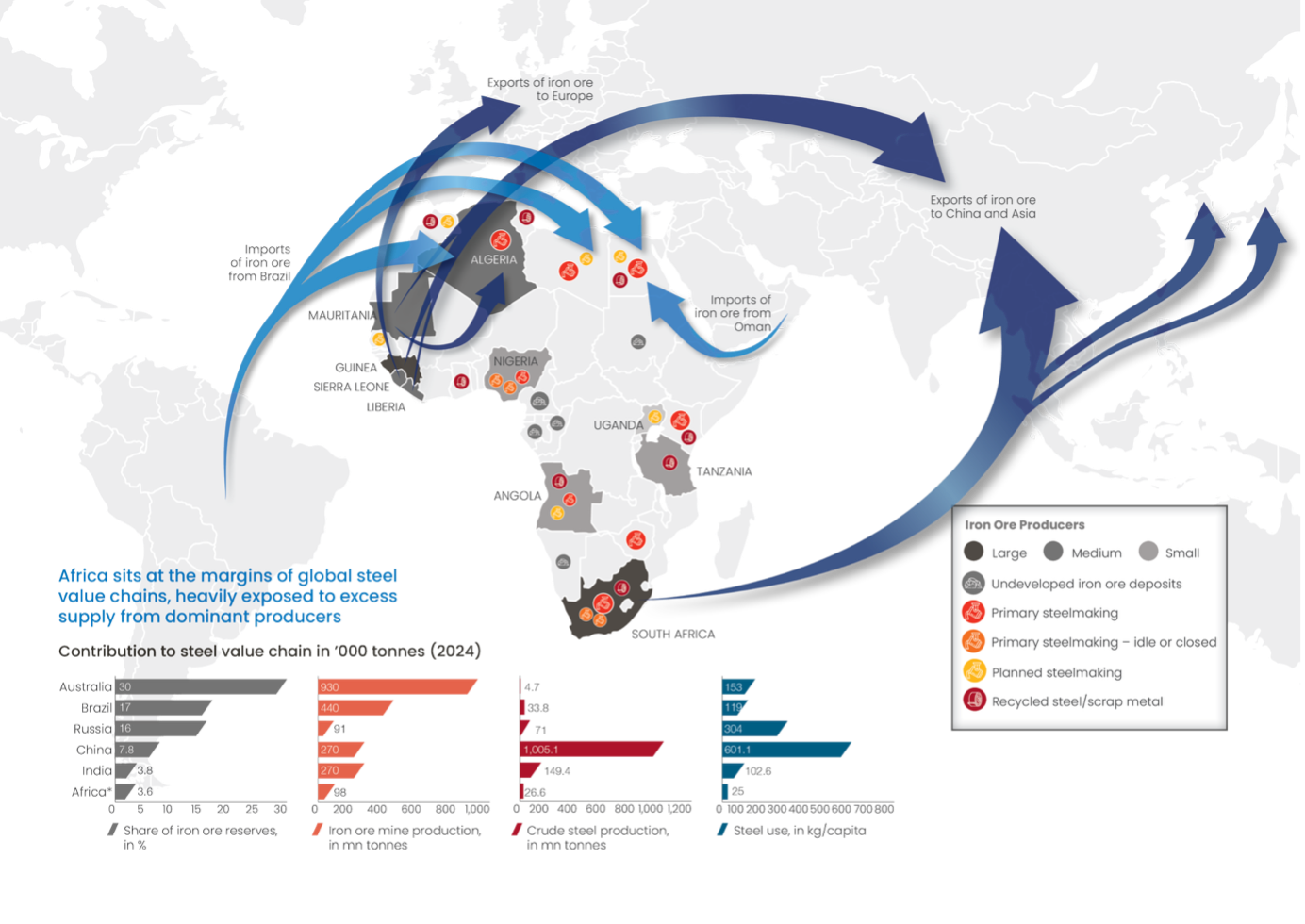

Given Africa’s development needs, steel cannot be treated as just another industrial product. It underpins transport systems, energy infrastructure, housing and manufacturing. But Africa’s per capita steel consumption remains roughly eight times below the global average. At the same time, its urbanization is accelerating at the world’s fastest pace, its infrastructure deficits are substantial and its industrial ambitions are expanding.

The continent continues to import significant volumes of finished steel and steel-intensive manufactured goods. And, when Africa imports steel, it is effectively importing it's own iron back, as well as the other materials used to make that steel, which also come from Africa: manganese from Gabon and South Africa, chromium from Zimbabwe and South Africa, nickel from Madagascar, vanadium and zinc from across Southern Africa.

As domestic primary steelmaking has weakened, internal demand for these associated minerals has remained tied to external steel cycles rather than Africa’s own infrastructure trajectory.

An iron ore expansion without a parallel steel strategy risks reinforcing that pattern.

Steel production is about system design

Working out how to boost Africa’s steel industry is therefore a question of system design. Africa possesses the core inputs required for competitive steelmaking: high-grade iron ore, significant manganese, nickel and chromium reserves, natural gas and expanding renewable and hydropower potential.

Steel demand also exists across the continent, in rail networks, mining corridors, energy infrastructure, housing and manufacturing. But this demand is fragmented by borders, policy reforms, procurement systems and financing structures. No single national market is large enough to anchor full-scale integrated production on its own. This makes regional coordination essential.

Aggregating demand and sharing infrastructure

Under the African Continental Free Trade Area (AfCFTA), regional cooperation could help to aggregate demand, improve offtake visibility and strengthen the economics of primary steelmaking, while also reinforcing standards to limit the smuggling of sub-standard products

South Africa illustrates the difficulty of sustaining domestic steel capacity without a sufficiently integrated regional market, with most primary steelmaking capacity currently idle amid weak, fragmented demand and high input costs. At the same time, infrastructure programmes across Southern and East Africa require exactly these products. The issue is not the absence of demand, but the absence of coordination.

Regional aggregation of infrastructure pipelines could also lower costs and strengthen competitiveness by enabling shared rail, port and power resources across transport corridors, power pools and industrial zones.

For bulk commodities, infrastructure and system design are the primary unlock. The Simandou project demonstrates this fundamental lesson: it only advanced once capital expenditure and infrastructure were structured as a shared system across multiple blocks and stakeholders, according to discussions during Mining Indaba, a conference held in Cape Town, South Africa, in February 2026.

Similar opportunities exist across the Guinea Highlands and the Gulf of Guinea, where integrated rail and port corridors — spanning Guinea, Sierra Leone, Liberia, Cameroon, Gabon and Congo – could transform isolated deposits into regional industrial platforms.

From extraction to industrial sovereignty

The global economy is entering a period of supply chain realignment. Industrial policy has returned. Governments are reassessing strategic dependencies. Decarbonization is reshaping heavy industry.

In this environment, Africa faces a choice. It can expand iron ore exports and remain a supplier of raw inputs into distant value chains. Or it can use this supply boom to re-anchor part of the steel ecosystem at home, linking ore, power, gas, ferro-alloys and regional demand into integrated corridors.

The latter path does not mean isolation. Africa will remain integrated into global markets. But it does mean capturing a greater share of the value chain, stabilizing demand for associated minerals, deepening manufacturing, putting in place policies that incentivise regional offtake and reducing vulnerability to external demand shocks.

Steel is not merely an industrial ambition. It is the backbone of infrastructure, the anchor of multiple mineral value chains and a prerequisite for industrial scale.

The next phase of Africa’s iron ore growth must therefore be matched by deliberate regional planning that aligns ore, power, transport and procurement under a coherent steel strategy. Without that integration, the supply boom will remain largely extractive. With it, Africa can establish a more competitive and resilient industrial base.

This article builds on discussions at a roundtable session during Mining Indaba 2026, as well as analysis by McKinsey & Company and CRU Group.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Industry: Mining and Metals

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Manufacturing and Value ChainsSee all

Laetitia Gardé and Marc Delobelle

February 26, 2026