Europe’s economic outlook: managing short-term shocks is no longer enough

Deep dive

Economic downturn and inflation sit at the top of European risk rankings. But just behind them are longer-term structural fears. Image: Alexandre Lallemand/Unsplash

- Europe is trapped between immediate economic shocks and slow-burning, long-term structural crises.

- European leaders link economic downturns with geoeconomic confrontation, threatening supply chains and trade stability.

- A sharp rise in misinformation and social polarization is paralyzing Europe’s ability to pass critical reforms.

Every year, the World Economic Forum asks thousands of senior business and policy leaders about the most pressing risks in their countries. The answers, drawn from the Executive Opinion Survey data collected between March and August 2025, reveal something striking about Europe: a continent caught between two distinct layers of anxiety, and increasingly aware that it must confront both simultaneously to survive.

The double threat facing the European economy

Think of two clocks on the same wall. The first runs fast, tracking concerns such as recession, an inflation spike, quarterly growth figures and other developments that dominate headlines. The second runs slow, and it measures longer-term concerns such as labour force shrinkages, infrastructure ageing, or the quiet fraying of the social contract. Europe’s leaders are watching both clocks simultaneously. The problem is that most policy responses are calibrated to the fast clock.

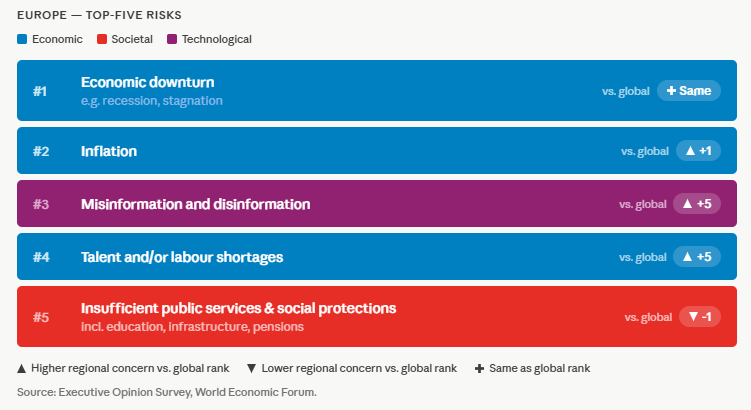

In 2025, economic downturn and inflation sat at the very top of European risk rankings, as the immediate, pressing concerns. But just behind them, steadily climbing, were longer-term structural fears: a shortage of workers and social safety nets that are beginning to come apart.

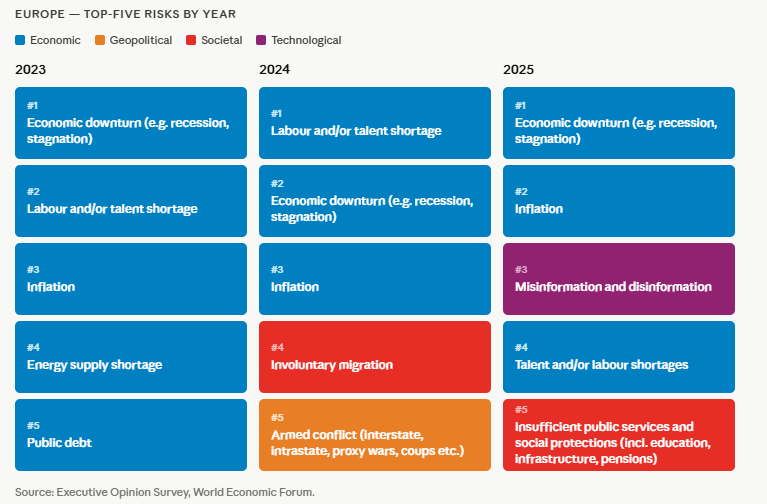

What is remarkable is how persistent Europe’s underlying worries have been. Economic downturn has topped the rankings for three consecutive years, while labour shortages and inflation have consistently remained among the top risks. But the real signal that the “slow clock” is ticking louder is the rise of longer-term social concerns: insufficient public services and social protections jumped from 14th place in 2023 to 5th in 2025. This shift mirrors real conditions on the ground, suggesting that Europe’s structural problems are finally breaking through the noise.

For leaders in the field of risk, this shifts the task from reacting to shocks to anticipating the slower-moving pressures that can harden into crises. “In an evolving European environment, effective risk management means looking beyond the immediate: anticipating the risks that matter most before they become crises,” says Barbara Badoino, Head, Corporate Ethics, Risk and Compliance at Novartis International. “In the pharmaceutical industry, guided by high standards of integrity and compliance, that same discipline supports responsible choices that consistently put people first.”

This is where the fast and slow clocks start to converge. Economic downturn functions as what is sometimes called a “hub risk” – a central threat that clusters with nearly every other major concern, from unemployment and debt to geopolitical tensions and labour gaps. Leaders are not simply bracing for another recession. They fear something harder to recover from: a low-growth equilibrium where structural problems, ageing populations, underinvestment and widening social gaps prevent recovery even when demand eventually returns. Europe ranks geoeconomic confrontation higher than the global average in 2025 (8th versus 14th globally), and concerns about economic downturn and geoeconomic confrontation often appear together, suggesting that European leaders see the two risks as fundamentally linked. The fear moves beyond a weaker economy; it includes a long-term concern about supply chains, trade barriers and strategic dependencies actively blocking the paths back to growth.

Misinformation and polarization: Europe’s new security frontier

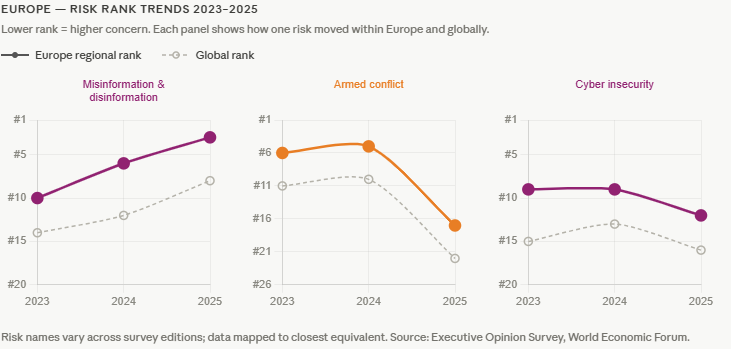

Three years ago, misinformation ranked 25th on Europe’s risk list. In the 2025 data, it sits at 3rd. In the same period, concern about armed conflict fell from 5th to 17th.

While the war in Ukraine continues and conflict in the Middle East has intensified since the 2025 survey results, one of the threats European leaders have elevated most sharply – misinformation – is not one fired from a weapon. Moreover, misinformation and social polarization cluster more tightly together in Europe than in most other parts of the world. And divided societies struggle to make the collective decisions that complex problems require.

For businesses, this turns misinformation from a public-policy concern into an operational and governance risk. “Addressing the risk of misinformation and deepfakes as a global organization in an increasingly uncertain world requires a multi-layered approach that combines technology, robust governance, employee education and strategic communication,” says Lisa Bechtold, Head of Group Risk Management at Nestlé. “As most online content will potentially be synthetically generated in the near future, vigilance and sound human judgement will be critical.”

How geopolitics and climate divide Europe’s risk map

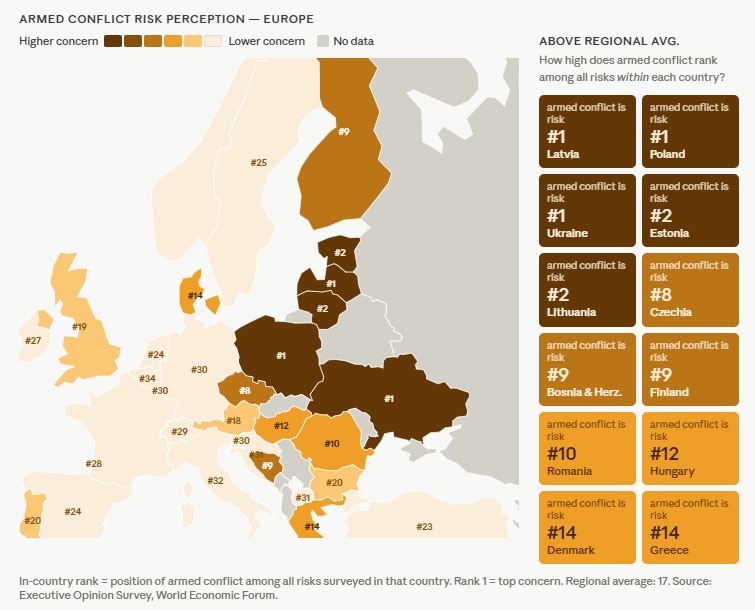

Zoom out from the continental picture, however, and a more complicated geography emerges. According to the survey, across 43 cases where individual European countries diverged significantly from global averages, every single one reflected heightened concern. Europe’s direction of divergence runs one way.

However, the texture of that alarm differs sharply by geography. Countries closer to active conflict – Ukraine, Latvia, Poland, Estonia – cluster around security risks: cyber warfare, armed conflict, biological and chemical threats. And Southern Europe’s profile is shaped by climate vulnerability in ways Northern Euope’s is not.

The time-series data reveals a further complication: European risk perception is volatile. Concern about geoeconomic confrontation – the fear that trade and investment become instruments of geopolitical rivalry – swung from 4th in 2022 to 25th in 2023 and 2024, before surging back to 8th in 2025 amid heightened concerns around tariffs, for example. Involuntary migration moved in the opposite direction: rising steeply through 2023 and 2024, then falling sharply. A strategy built on a snapshot of European concerns will always be looking at the wrong clock.

Balancing economic growth, defence spending and climate risk in Europe

Take all this together, and three interlinked challenges emerge.

The first is how to escape from the political logic of managing short-term risks first while pursuing structural reform later. The data suggests this is a trap. Long-term concerns are shaping business decisions today. And policies that foster economic transformation and growth also lower vulnerabilities to disruption.

The second is how to properly link economic policy and security policy. This must recognize the complementarities – there can be no economic growth without security – but also the tensions. Trade and international specialization are a pillar of growth, but also a source of vulnerability to economic coercion. And spending on defence takes away from spending on education, reskilling and climate action – which help address competing sources of risk.

The third challenge is how to address these issues in an environment of political polarization, misinformation and eroding trust. The central question, then, is how can Europe turn diagnosis into action: in other words, how can it address these challenges and manage the associated trade-offs?

On defence, Europe must rearm and gain autonomy. But it must do so in a way that is fiscally affordable, benefits growth and maintains cohesion: by raising scale, creating cross-border competition, sharing fiscal burdens and maximizing innovation spillovers.

On economic security, Europe must lower external dependencies, but it must do so in a way that maintains the benefits of trade and respects international commitments.

On the business front, Europe must protect its key industries and prevent its social fabric from tearing. But it must also understand that protection can at best buy time. It will need to discover new comparative advantages in sectors and regions that make best use of its labour force, human capital and institutional strengths.

And finally, Europe must not lose sight of climate change as a critical source of long-term risk. Addressing this risk without dividing societies requires mobilizing social mechanisms that spread burdens widely.

Europe’s fast and slow clocks will not wait for each other. Neither can its policy-makers.

Additional insights and contributions by Mark Elsner.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.