The below-market finance myth: why benchmarks matter for developing economies

The below-market finance issue affects perceptions of fair competition and policy space available to developing economies. Image: Getty Images

- Below-market finance is coming under increasing scrutiny as a means of potentially unfair competition amid heightened use of industrial policy.

- To properly assess below-market finance, accurate benchmarks are needed that don't mistake borrower-specific loan pricing for market distortion.

- The benchmark issue particularly affects developing economies, whose financial systems are often less like external models.

With governments making greater use of industrial policy, while trade tensions and scrutiny of state support also rise, below-market finance is coming under the spotlight.

Below-market finance can be understood as funding provided to firms at interest rates lower than a comparable market lender would charge. It can take the form of low-cost bank loans, public-bank lending, direct credit or other policy-influenced credit channels. It matters because cheaper credit can reduce a firm’s cost of capital and is therefore often discussed in subsidy and fair-competition debates.

Whether a loan is judged to be “below market” can affect how subsidy claims are assessed and whether trade remedies are considered. The issue is not only technical: It can shape perceptions of fair competition and policy space available to developing economies.

But deciding whether finance is truly “below market” depends on the benchmark.

OECD studies in 2021 and 2026 treat below-market finance as a recurring category in assessments of industrial support across economics, not as a country-specific issue. If a yardstick is set too high, or imported from a financial system with different institutions, ordinary differences in borrower risk, collateral or bank pricing may be mistaken for market distortion.

This is especially relevant for developing economies, where firms often rely more heavily on bank credit and where financial systems may differ from advanced-economy templates.

The example of China provides a useful framework for asking: Should firms be assessed against an external reference rate, a quoted pricing anchor such as the Loan Prime Rate (LPR), or a benchmark that reflects the domestic financial environment and borrower risk?

Redefining the benchmark

The central challenge in the below-market finance debate is benchmark misidentification. In China’s case, some external assessments compare corporate borrowing costs directly with the LPR, or with risk-free anchors from very different financial systems.

The LPR is important. It is the central pricing anchor for bank lending in China. But it is not the same as the final interest rate paid by every borrower. In practice, banks price loans around the LPR, adjusting for borrower risk, collateral, maturity, contract structure, funding cost and customer profile. A loan priced below the LPR may reflect a lower-risk borrower or stronger collateral, not necessarily a policy-driven subsidy.

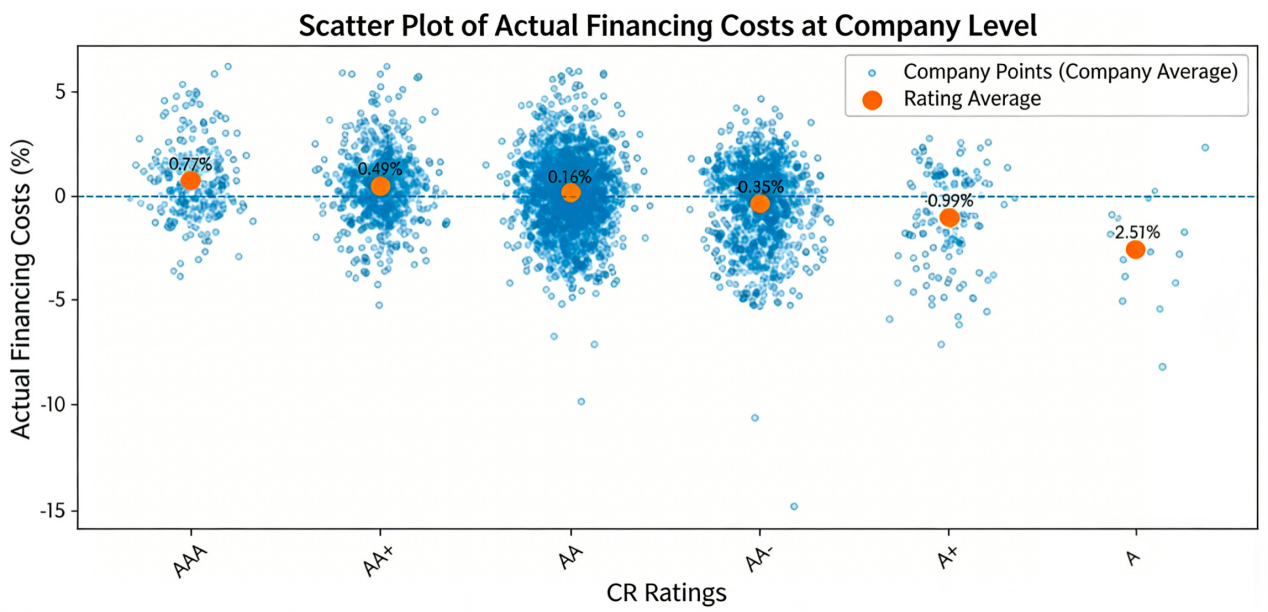

To address this issue, we propose a domestic market benchmark that is relevant to the borrower and to China’s financial system. It combines domestic risk-free conditions, rating-matched credit spreads and a domestic adjustment component, adapting the tiered pricing logic used in OECD’s 2021 study. When Chinese corporate borrowing costs are compared with this benchmark, the picture changes.

Evidence from the demand side

Using financial statement data for Chinese A-share listed firms from 2010 to 2024, we find that average borrowing costs are not below the estimated domestic market benchmark. They are about 0.2 percentage points higher.

This does not mean that no individual firm ever receives relatively favourable financing. Some firms, in some periods, may borrow at relatively low rates. But a low rate may be commercially justified if the borrower has stronger collateral, more stable cash flow, lower default risk or a shorter maturity structure. Such cases do not by themselves establish broad, systematic below-market finance.

What banks tell us

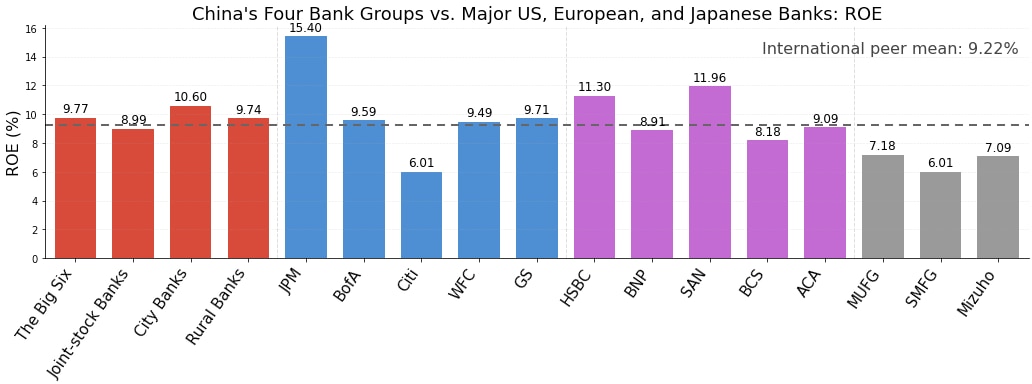

Bank-side evidence points in the same direction. If banks were widely sacrificing commercial returns to provide underpriced loans, that behaviour should show up in weaker profitability.

Yet major Chinese financial institutions do not show the kind of profitability distortion one would expect from broad, policy-driven underpricing. Average loan yields across major bank groups also move in close alignment with the LPR and other benchmark rates, while maintaining spreads that reflect customer and institutional differences.

This evidence suggests that credit allocation in China remains constrained by balance-sheet requirements, risk management and commercial profitability targets. It does not rule out targeted support in specific sectors or periods. But it does weaken the claim that Chinese corporate borrowing is broadly and systematically priced below market.

Why the issue matters beyond China

The benchmark problem is not unique to China. OECD and IMF studies treat below-market finance as a general analytical category, not as a country-specific label. IMF research on Brazil, for example, discusses directed credit and public-bank lending at regulated or below-market interest rates.

A benchmark-sensitivity check discussed at a research seminar of the China Modern Financial Society also shows that, when a comparable pricing-decomposition logic is applied to a Bloomberg-based sample of US-registered bond issuers, the average benchmark-adjusted gap is -1.55 percentage points. This does not mean that US corporate finance should be labelled as subsidized. It shows that “below-benchmark” results can emerge if a particular benchmark is chosen.

This matters especially for developing economies because their financial systems are often less like the models assumed in external benchmarks. Bank lending may play a larger role than bond markets; credit ratings may cover fewer firms; collateral practices may differ; and monetary-policy transmission may work through different channels. If these differences are not reflected in the benchmark, subsidy assessments may overstate distortion and understate legitimate market variation.

Towards more accurate global assessments

As global trade tensions increase, subsidy-related disputes require more precise analytical tools. International assessments of below-market finance should start with a basic question: Is the benchmark appropriate for the financial system being assessed?

A more balanced framework should do four things:

- Distinguish nominal rate differences from substantive subsidies. A lower observed interest rate is not automatically evidence of policy distortion.

- Respect the commercial validity of risk-based pricing. Borrower risk, collateral, maturity, funding cost and bank balance-sheet constraints all affect loan pricing.

- Use transparent, market-based domestic benchmarks that reflect local monetary architectures and actual lending practices.

- Recognize that developing economies may have different financial systems without those differences automatically implying non-market behaviour.

Future global financial governance should move beyond simple narratives and surface-level rate comparisons. Better benchmarks would not weaken subsidy assessment. They would make it more accurate, more credible and more institutionally fair. That matters for global finance because firms and economies should be judged by comparable standards, not by benchmarks that mistake institutional difference for market distortion.

Zhao Youli, Cheng Shi, Zhang Shubo and Zhang Yanwen were additional contributors to this article. Further reading on below-market finance benchmarks is available here.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Financial and Monetary Systems

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Kate Whiting

July 13, 2026