How fintech forges resilience in ASEAN – with lessons for the wider world

Image: Christiaan Koepke/Unsplash

- Global trade disruptions disproportionately impact small and medium enterprises (SMEs), but their crisis-driven adoption of financial technology (fintech) is sparking wider change.

- Fintech offers SMEs tangible solutions to trade frictions, such as P2P lending and streamlined cross-border payments, enabling faster access to cash and simpler international transactions.

- The current crisis-driven fintech adoption is stress-testing and validating these technologies at scale.

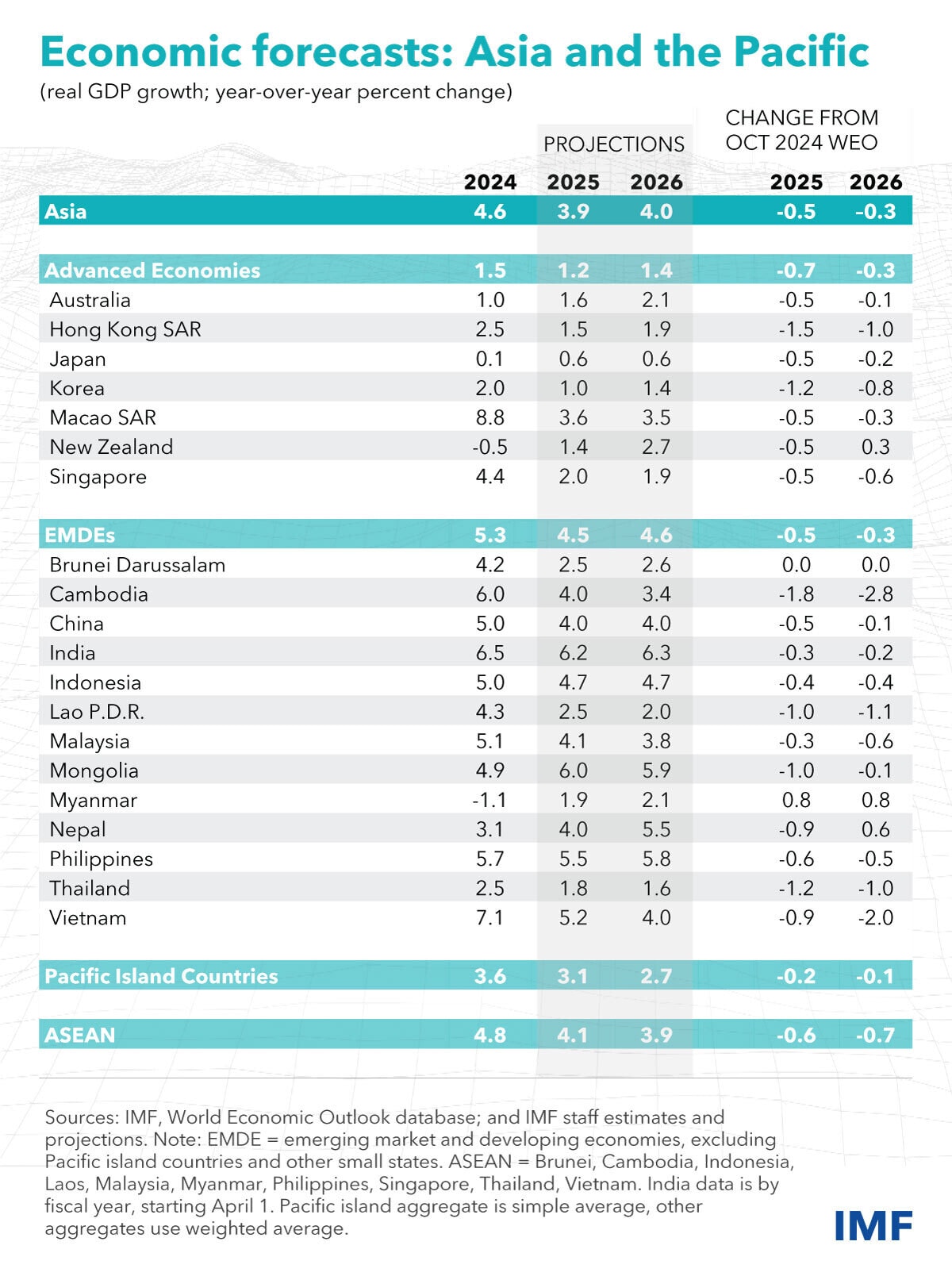

The current era of protectionism and reciprocal tariffs between major economic players sends ripples far beyond those who initiated them. These waves are felt across regions like ASEAN, which is at the crossroads of these global realignments. This uncertainty forces businesses, especially in trade-reliant regions like ASEAN, to rethink how they buy, sell, and manage their supply chains. Indeed, ASEAN’s growth is set to slow from 4.8% to a projected 4.1% in 2025.

Small Businesses are Bearing the Brunt but Driving Change

SMEs – the bedrock of most economies, including ASEAN, where they represent over 99% of firms and are crucial for employment – are often most exposed to volatile climates. Unlike large corporations, SMEs often have smaller cash reserves and fewer resources.

Cash flow management becomes a critical challenge when supply chains fray, orders are delayed, or input costs surge unexpectedly. Access to traditional financing can also constrict as financial institutions may adopt more conservative lending stances amid perceived heightened risks. This environment demands agility and innovative solutions to keep these vital economic engines running.

Fintech: A Catalyst for SME Resilience

The dynamism of fintech is emerging as a critical enabler to support SMEs. The challenges amplified by global trade frictions are accelerating fintech adoption and proving the value of these innovations that benefit SMEs:

● Getting paid faster, accessing funds quicker: Instead of waiting weeks or months for traditional bank loans or customer payments, fintech platforms offer services like invoice financing (getting an advance on unpaid invoices) and peer-to-peer (P2P) lending (connecting businesses directly with investors). For example, Funding Societies, a major P2P operator in Southeast Asia, has disbursed over $4.38 billion in financing to over 100,000 SMEs, with close to 95% of financing fulfilled in less than 5 days. This helps SMEs manage unexpected costs or invest in finding new markets.

● Making international sales easier: Selling to new countries often means complex and expensive international bank transfers. Digital payment platforms simplify this with faster, cheaper, and more transparent transactions. Digital cross-border payment platforms offer streamlined, faster, and more cost-effective solutions, making it more viable for SMEs to engage with new international partners. Launched in late 2022, the ASEAN Regional Payment Connectivity (RPC) initiative streamlines cross-border transactions by enabling local currency payments, reducing reliance on intermediaries, thus lowering costs and transaction times.

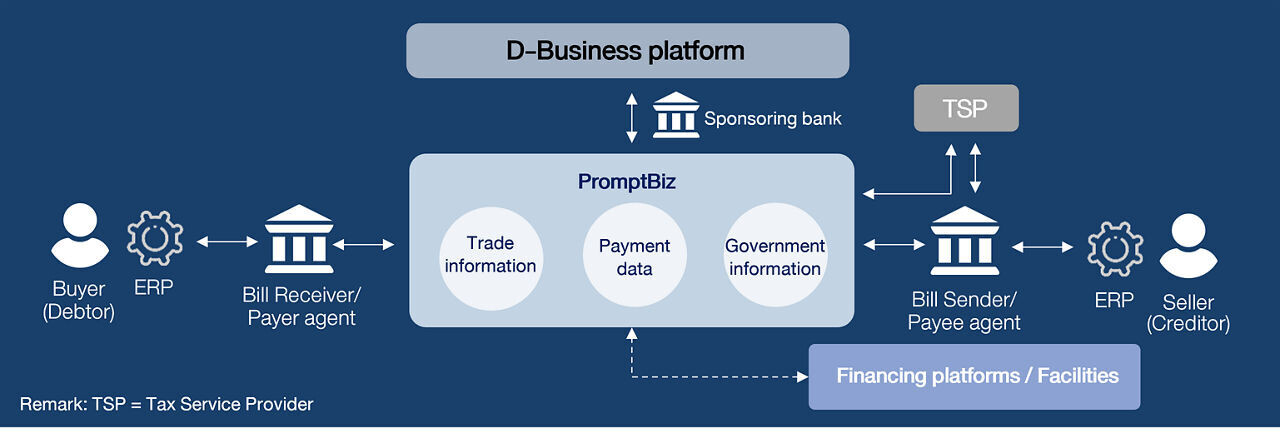

● Smoother Trust and Efficiency in Supply Chains: Fintech tools can improve how money flows through entire supply chains. Some new technologies, like blockchain (a secure, shared digital ledger), promise even greater transparency and efficiency in tracking goods and payments. Thailand's PromptBiz initiative, for example, aims to simplify B2B trade and payments, enabling SMEs to access invoice financing more easily through participating banks.

The Rebound: How SMEs adapt through crisis-driven innovation

When large numbers of SMEs adopt these new fintech tools out of necessity, it's more than just a survival story. It’s a real-world testbed for better ways of doing business globally. Asian SMEs are showing, on a large scale, that fintech solutions are not just theories—they are practical, efficient, and effective tools for global trade.

As businesses get used to faster payments, lower transaction costs, and more transparency, these benefits start to become the new expectation. This shift isn't gradual; it's a direct consequence of current pressures forcing rapid innovation, making the case for broader adoption more compelling now than ever before. This can push larger companies and traditional banks to improve their services. The tools and practices gaining popularity among SMEs today could well become the standard ways of conducting international trade and finance tomorrow.

Think of it as innovation bubbling up from the ground up.

Challenges to wider fintech use

However, for fintech to truly help all SMEs and reshape global trade, some significant hurdles need addressing:

● The digital gap: Not everyone has equal access to digital tools or the skills to use them – a gap that, if unaddressed in our rapidly digitising global economy, will leave many SMEs behind today. Initiatives like Go Digital ASEAN, which has trained over 215,000 SMEs and MSMEs in digital skills, are crucial. Yet, more effort is needed to improve digital literacy and ensure affordable internet access.

● Security worries: Using more digital tools means an increased risk of cyberattacks. SMEs are frequent targets – 43% of cyberattacks in 2023 targeted small businesses, and the average cost of such an attack can be substantial, even up to $120,000. Stronger cybersecurity measures and awareness are vital.

● Clear rules and collaboration: The rules for fintech are still developing and can vary widely between countries. Clearer, more consistent regulations are needed to encourage innovation while protecting users and ensuring financial stability.

Have you read?

The Way Forward: Building a More Resilient Trade Future for All

The experiences of ASEAN SMEs and the innovative responses from the fintech sector offer critical lessons for the world. It's a call for everyone involved in global trade – governments, banks, and tech innovators – to:

1. Upgrade Financial Systems: Learn from the speed and efficiency SMEs find with fintech. This means supporting the development of better digital infrastructure for all and finding ways to integrate these new, proven tools more broadly.

2. Create Smart Regulations: Develop clear and supportive rules for fintech and digital finance. These rules should encourage new ideas while managing risks like cybercrime and data privacy, ensuring that these technologies can safely benefit as many businesses as possible.

By learning from these nimble businesses and supporting the technologies that help them, we can build a global trade system that is not only more resilient to shocks but also more efficient and inclusive for businesses of all sizes. The challenges of today, met with smart solutions, can genuinely pave the way for better global commerce tomorrow.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.