5 biggest risks to the global economy today

Global debt recently hit a new record high of 225% of world GDP, amounting to US$164 trillion. Image: REUTERS/Alex Grimm

Wall Street giant Lehman Brothers filed for bankruptcy on September 15, 2008, triggering the most significant global financial crisis since the great depression. Lehman’s collapse was not triggered in a day but over a much longer period, with assets of US$680 billion (£518 billion) supported by only US$22.5 billion of capital by the time it went under. As the subprime mortgage crisis began to eat up financial institutions, this once invincible bank was suddenly no more.

A decade later, with many of the world’s leading economies struggling to grow consistently, one would have hoped that the banking industry and its regulators would have learned from what happened. Gordon Brown, UK prime minister at the time of the collapse, doesn’t think so.

Brown believes we are “sleepwalking” into the next global financial crisis. He sees insufficient headroom to resuscitate economies by cutting interest rates or raising public spending. He describes a “leaderless world” in which it looks harder to achieve the global coordinated action that was critical for avoiding even greater disaster ten years ago.

Is there any room for cheer? Here’s my brief assessment of the indicators that will be crucial in any future crisis.

1. Debt

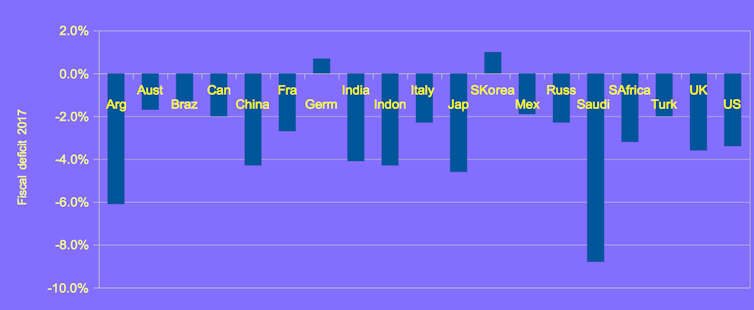

Global debt recently hit a new record high of 225% of world GDP, amounting to US$164 trillion. The world is now 12 points deeper in debt than the previous peak in 2009, with advanced economies’ ratios at levels not seen since World War II.

This is forcing countries with large fiscal deficits to pay ever more interest to cover their bills. And if they can’t reduce their deficits, they will find it tough to deal with even the lightest economic downturn. Hence the recent call from IMF director Christine Lagarde for countries to fix “the roof while the sun is still shining”, by cutting deficits, improving banking capital buffers and maximising exchange rate flexibility.

G20 fiscal deficits, 2017

2. Emerging markets

Nervous investors have been heavily selling assets in emerging markets, such that inflows into these countries plummeted to US$2.2 billion in August compared to a high of US$13.7 billion only a month before. The outflow of money has emaciated the currencies of Turkey, Indonesia and Argentina. Meanwhile, the US greenback gets stronger and stronger as investors seek to benefit from the strength of US treasury bonds and other dollar-denominated assets. These changes are bound to affect international trade, heightening the prospect of contagion to other countries.

3. Trade

The trade tensions between the US and China represent a massive geopolitical risk. These countries have the highest debt piles in the world, US$48.1 trillion and US$25.5 trillion respectively. Any economic fallout from their trade posturing could put global financial markets in a fix.

We are already seeing the impact on the Chinese stock market, which has lost about 20% of its value already this year. There are knock-on effects in Hong Kong, dragging down the Hang Seng trading index to a 14-month low lately. The contagion could soon spread around the globe, including to emerging economies already reeling from the aforementioned currency crises discussed above.

4. Banking

In the aftermath of Lehman, the world’s major banks have moved from depending on short-term borrowings to building larger capital buffers to help them steer through another credit crunch. Be that as it may, many other banks have still looked vulnerable – especially after the Greek, Spanish and Italian banking crises of recent years. It is a strong signal that regulations are still insufficient to protect the system overall.

Then there is shadow banking – essentially financial institutions which aren’t banks, such as insurance companies or hedge funds, providing banking services such as lending. This grewrapidly after the previous crisis, since the institutions in question are subject to fewer regulatory restrictions as the banks.

A mind-boggling study from the US last year, for example, found that the market share of shadow banking in residential mortgages had rocketed from 15% in 2007 to 38% in 2015. This also represents a staggering 75% of all loans to low-income borrowers and risky borrowers. China’s shadow banking is another major concern, amounting to US$15 trillion, or about 130% of GDP. Meanwhile, fears are mounting that many shadow banks around the world are relaxing their underwriting standards.

5. Cyber hazards

Some analysts also worry that the next financial crisis could be triggered by cyber attacks on today’s fully digital and interconnected financial system. This has consistently been rankedas the number one concern by respondents to the Depository Trust’s Systemic Risk Barometer since its surveys began in 2013.

In sum, despite the efforts to strengthen the financial system, it looks far from failsafe. Gordon Brown is unfortunately right that the world has not managed to do enough to prepare itself for the next shock, and the growing divisions within the international community make the situation look particularly dangerous. We have not been able to curb the tendency of financial institutions to take on excessive risk, and as Brown also said, there is still not enough of a corrective mechanism for those who act irresponsibly.

JP Morgan is predicting the next crisis will strike in 2020, if not earlier, and this does seem quite foreseeable. So brace yourself and stay prepared, and let’s hope that things don’t turn out as badly as they potentially could.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Banking and Capital Markets

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Ibrahim Alramady

July 1, 2026