Nepal faces a crisis as COVID-19 stems the flow of remittances

Some migrant workers were abandoned by employers after coronavirus hit. Image: REUTERS/Jumana El Heloueh

Andrew Caruana Galizia

Head of Europe and Eurasia, Member of the Executive Committee, World Economic Forum- Remittances represent more than a quarter of Nepal’s economic output.

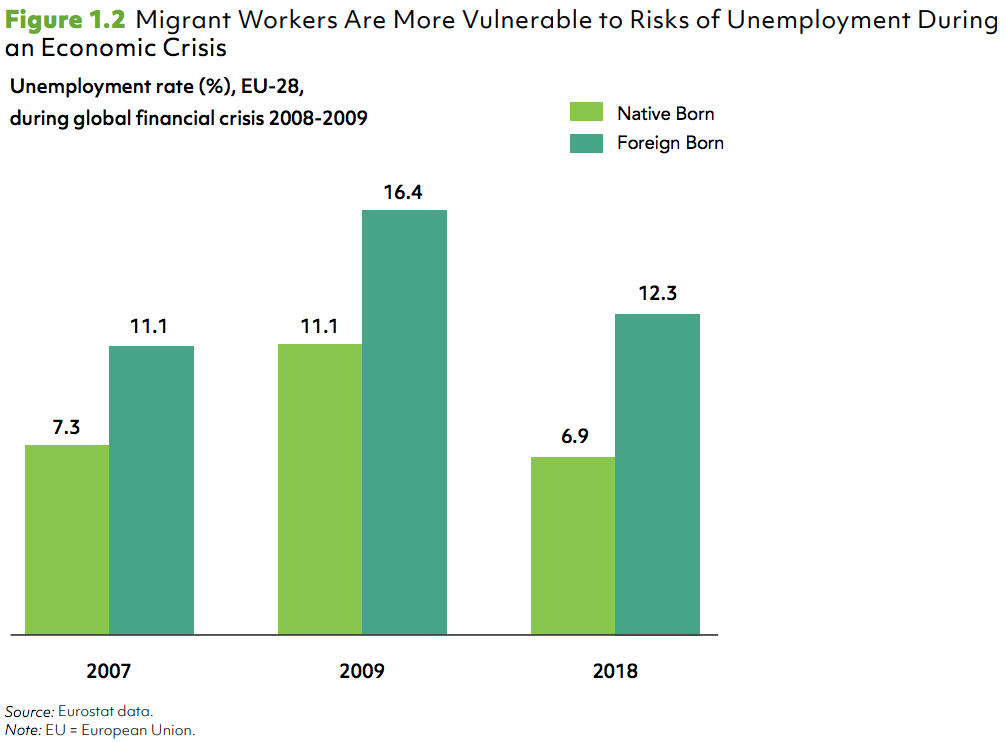

- The pandemic means migrant workers have swapped the risk of death or injury at work with the reality of poverty and homelessness.

- Financing a shift from subsistence to commercial farming could help prevent food shortages and stimulate employment.

- Digitization could make migrant workers more resilient to shocks.

The mixed fate of South Asia’s millions of migrant labourers in the Gulf and elsewhere has long been a humanitarian issue. Now that a pandemic has pushed the world into recession, their precarious employment conditions have emerged as a major economic issue for the countries in South Asia that most depend on the earnings migrant workers send home as remittances. The World Bank projects that remittances to Nepal will slide by 14% this year – not the biggest slump in the region, but remittances represent more than a quarter of the country’s economic output. No other country in South Asia comes close – the next biggest share of remittances was around 8% of GDP in 2019, for both Pakistan and Sri Lanka.

A protracted civil war followed by devastating earthquakes pushed millions of largely unskilled Nepalis to seek work elsewhere. As a result, remittance inflows to Nepal have risen steadily each year for the past decade. By 2019, the annual total had doubled to more than $8 billion, compared with just over $4 billion in 2011. In the six years between the outbreak of the Ebola epidemic in West Africa and the global spread of COVID-19, remittances grew from a lifeline for impoverished rural families to a key motor of Nepal’s economy – far in excess of other financial inflows such as foreign direct investment and net official development assistance – and a key source of liquidity for its banking system.

Though a thriving industry of recruitment agencies and remittance service providers has sprung up around the phenomenon, the financial, digital and welfare infrastructure supporting Nepal’s migrant workers has remained largely inadequate, leaving Nepal struggling to respond to the twin challenges of falling remittances and hundreds of thousands of stranded or returning migrants now out of work.

The end of a bitter road

Data from the Department of Foreign Employment compiled by the International Organization for Migration (IOM) show that the Gulf states of Qatar, United Arab Emirates (UAE), Saudi Arabia and Kuwait are the most popular destinations after India for Nepali migrant workers. Qatar and the UAE alone accounted for 58% of all the permits issued by the government of Nepal in 2019 allowing migrants to work abroad. These migrant workers pay a high price for the money they earn in the Gulf: in the past five years, there have been 4,143 cases of financial compensation paid by the government of Nepal from the Foreign Employment Welfare Fund to family members after the death of a migrant worker, and 1,348 cases of assistance for injured workers. In 2018/19 alone, the scheme paid out to 755 families after a migrant worker’s death, and assisted with 588 cases of work injury.

The strict lockdown measures – India, Malaysia, Saudi Arabia and the UAE all stopped non-essential services during the pandemic – hit the tourism, hospitality and construction sectors hardest, where many migrant workers were concentrated. Laid off at short notice, often with no savings, unemployment insurance, or residency rights, the not insignificant risk of death or injury at work has been replaced by the reality of poverty and homelessness.

Migrant workers are also especially vulnerable to COVID-19 because of the conditions in the crowded labour camps they are often based in. Putting a number to the scale of the problem, in mid-May, Nepali Foreign Minister Pradeep Kumar Gyawali told a parliamentary committee that a staggering 211,000 Nepalis needed to be rescued and repatriated immediately, and that many thousands more would need to be brought back home to Nepal at the next opportunity.

Before the crisis hit, many Nepali migrant workers sold ancestral land or borrowed money through informal networks to raise the high fees recruitment agencies charge for securing visas and work placements abroad. Suddenly jobless and unable to pay down these loans, they will now likely need to take on further debt to refund the costs of their repatriation.

Alongside a diplomatic push to preserve existing jobs abroad, a government task force is examining ways to reintegrate these thousands of returning migrants into Nepal’s labour force. One initiative is for the central bank, Nepal Rastra Bank, to help with lower-rate loans for entrepreneurial activities such as commercial farming – agriculture accounts for 27% of Nepal’s GDP, though it remains largely capital-poor.

With border closures slowing trade and the hundreds of thousands of returning migrants causing a surge in domestic food demand, financing a rapid move from subsistence to commercial farming could help prevent likely food shortages and stimulate employment. The government could provide incentives and support for financial products to reach remote locations, potentially by sharing the costs incurred by rural financial service agents.

Yet, as crises often do, the impact of the pandemic has exposed several flaws in the remittances sector and made the many avoidable hardships suffered by migrant workers suddenly intolerable, which opens the window to nudge changes through at a structural level.

Digitization could make migrant workers more resilient to shocks

Governments in host countries should act to ensure workers are documented in the first place and then make it possible for their identification documents to be linked digitally to electronic ‘know your customer’ (e-KYC) systems. Digital remittances from Nepal’s migrant workers could then be linked to modest savings or pension contributions. If they could access digital solutions easily and make modest savings more readily, the temporary economic security of such large numbers of migrants, their families back home, and entire national economies like Nepal’s, could be assured through crises like this one.

Several players in Nepal have shown significant leadership in tackling the crisis, with the central and private banks unrolling digital solutions to help keep the remittances lifeline tethered to the national economy. The central bank has raised the amounts that may be digitally transferred or paid to merchants, in an incentive that may stay in place after the current pandemic is over. Retail banks across the country, meanwhile, have moved to processing remittances digitally so that those back home relying on migrant workers’ money can avoid going to bank counters for cash withdrawals.

As an enabling backdrop to this digitization, Nepal’s prospective migrants since 2018 have had to open bank accounts to qualify for mandatory labour permits – a policy also designed to reduce the use of informal channels for remittances. At least 61% of Nepalis now have at least one bank account. But the ability of Nepali migrants to open accounts in their host countries is now a critical step towards unlocking end-to-end access to digital channels.

Much more can be done to empower Nepali migrants

The flow of remittances from unemployed migrant workers digging into their savings or from those who have managed to hold on to their jobs could be set on fairer terms by providing incentives to banks, mobile network operators, remittance service providers, and payment infrastructure providers to cut transaction fees and make formal remittances more attractive. Nepal could follow the example of Bangladesh’s central bank, which has raised the ceiling on the 2% “cashbacks” it offers remittance senders.

Remittance service providers themselves can make transactions more attractive by linking remittances to inclusive financial products tailored to the needs of migrants and their families, including savings, credit, insurance and bill payment services. Taken together, these solutions could contribute to building individual resilience on a wide scale until migrant workers gain greater access to national welfare schemes and residency rights in their host countries.

What is the World Economic Forum doing to manage emerging risks from COVID-19?

Nepal Rastra Bank could consider measures aimed at both smoothing the flow of funds during this period of hardship and paying off the toxic informal debts that many migrant workers had taken on to finance their journeys. The central bank could collaborate with remittance service providers in key markets to extend low-interest credit to migrants, with the repayments not starting until their work resumes.

An online portal launched by the government of Nepal would be a vital service to its migrants abroad, giving them access to information and services in Nepali. This could include enabling digital registration with the local embassy and providing medical information and directions to seek treatment. It would also be a good way to facilitate access to legitimate digital money sending channels.

A cross-border problem requires global solutions

In mitigating the pandemic’s impact on the remittances sector, cooperation across sending and host countries and across public and private stakeholders is key. One example of how this can work in practice is the high-level call to action announced on 22 May to keep remittances flowing, spearheaded by the governments of Switzerland and the United Kingdom. The call highlights the measures required of different stakeholders to facilitate the flow, including the opportunity to digitize transactions. The World Economic Forum’s Regional Action Group for South Asia is also supporting a multi-stakeholder working group to devise recommendations to manage the fallout from the remittance crisis.

Nepal and its migrant workforce have been struck by crisis just as the economy back home was turning a corner. The country now faces the cascading impact of returning migrant workers and sliding remittance flows in the midst of a global public health emergency. It will see long-term benefits if it can find the capacity to give new hope to those who have found their way back home at the end of a bitter road. Nepal can also better support migrants abroad through the pandemic – this includes reminding host countries of the long-run impact their migration policies can have on a country like Nepal and its people.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Nepal

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Health and Healthcare SystemsSee all

Mansoor Al Mansoori and Noura Al Ghaithi

November 14, 2025