The chemical and materials industry can boost the impact of stimulus packages. Here’s how

From construction to healthcare, the chemicals industry plays a pivotal role in a sustainable recovery post-COVID. Image: Pilmo Kang / Unsplash

Tobias Radel

Industry Lead Chemicals and Natural Resources; Austria, Switzerland, Germany, Russia, Accenture Strategy & Consulting- The chemical and materials sector can play a significant part in maximising the impact of COVID-19 stimulus packages around the world.

- The sector is at the heart of many global value chains, and as such has a key role to play in the move towards sustainability.

- Here are three steps the sector's leaders can take to maximise the reach and impact of stimulus funds.

Aside from being the worst health and humanitarian crisis for decades, COVID-19 has caused a drop of almost $7 trillion in global GDP this year.

In response, governments around the world have committed more than $15 trillion in COVID-19 stimulus packages. Is there a role to be played by the chemicals and materials industry in maximizing the positive impact of these interventions? We think so.

Through collaboration with policy-makers and other stakeholders, this sector's leaders can not only offer solutions that meet new consumer demand for sustainable products, but which can also play a proactive role in bringing innovation into value chains to 'build back better' – and help the sector move towards a more renewable, circular and resilient future.

The World Economic Forum’s Chemical and Advanced Materials Industry Action Group (IAG), supported by the Forum in collaboration with Accenture, has identified opportunities to increase sectorial and societal resilience through collaborative action. As part of this work, we're keen to highlight the role of the sector in boosting the impact of economic stimulus packages.

Economic stalemate

The chemical industry converts raw materials into more than 70,000 different products. These products have a broad range of uses in the food, healthcare, building and construction, consumer goods, agriculture and transportation industries. Common chemical sector products include surfactants, pigments, synthetic rubber, polymers, fertilizers and materials for batteries, to name but a few.

Since 2018, chemical output growth has slowed or contracted in key manufacturing countries. Both Europe and North America have reported reduced chemical activity for 2019, mainly as a result of the global economic slowdown and trade tensions. Now COVID-19 has forced its customers’ industries to shut down entire plants – which is expected to reduce global chemical GDP by around 11% in 2020, according to Accenture research. Recovery for the chemicals and materials industry hinges on the recovery of its core customers –such as the automotive, building and construction, and consumer goods sectors – but their path to recovery is uncertain, and is likely to remain so for the next two or three years.

In addition, demand patterns will become increasingly more dynamic as some of the COVID-19-induced consumer behaviours become the new reality post-crisis. The pandemic has triggered a change in how people live, buy and think. For example, demand for sustainable products had already been growing for a while, but new research shows that after the pandemic 79% of consumers said they will seek out products that are healthier and better for the environment, and that they are willing to pay a premium for them.

There is also greater health consciousness among consumers and an increased desire for convenience and comfort, as evidenced by the growth of online shopping. These changes in consumer behaviour will play out for manufacturers of personal care, packaging, lubricants or nutrition products in different ways. Small pockets of the industry may benefit – such as those that produce chemicals included in sanitation products or certain plastics used in packaging and PPE – but other areas will be negatively impacted.

Turning stimulus to advantage

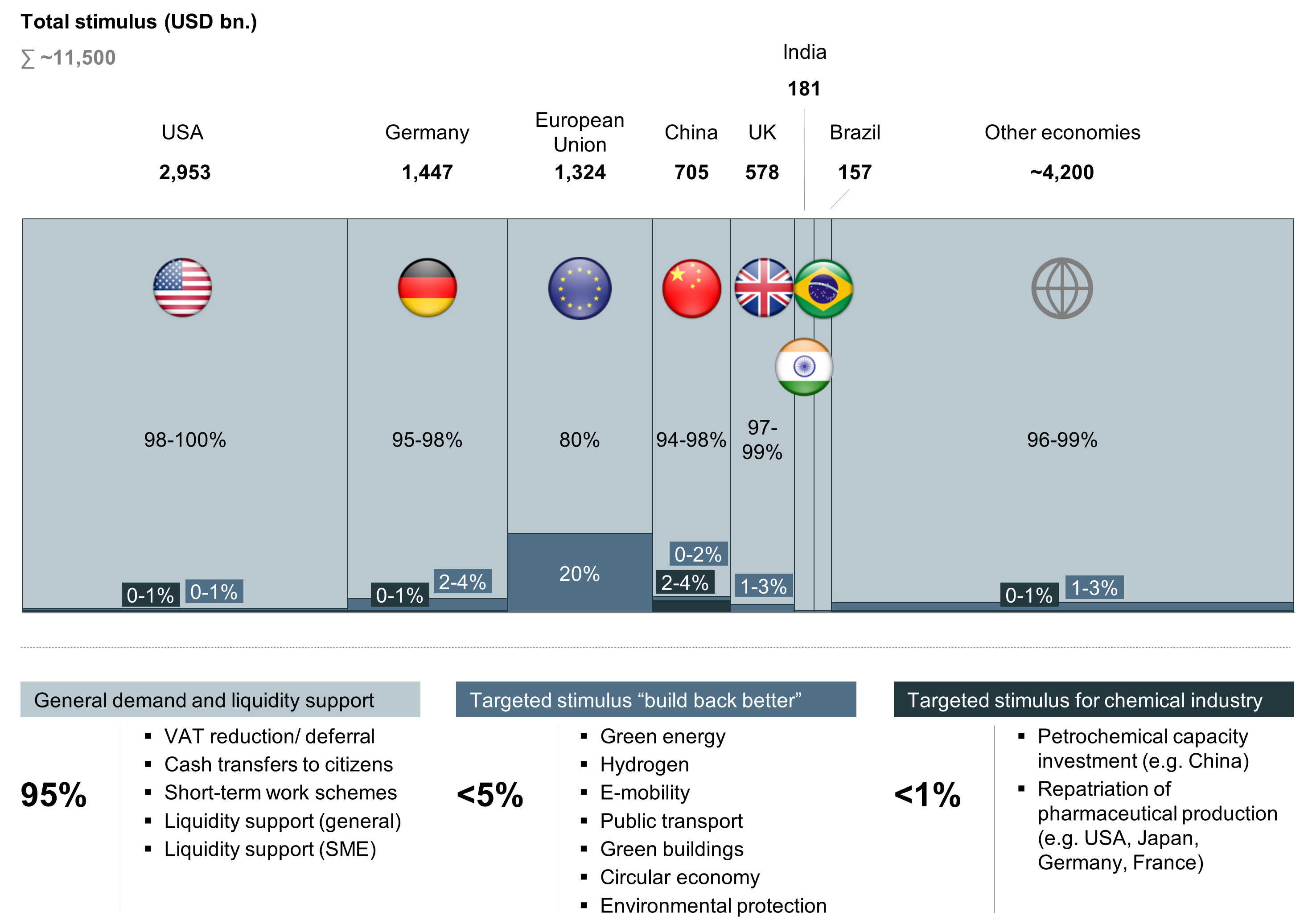

Governments are taking drastic measures to close the GDP gap with stimulus packages worth up to $15 trillion – three times what was spent (as a percentage of GDP) following the 2008 financial crisis. This makes governments around the globe the most powerful consumption engines in their economies.

As the chemical industry lies at the heart of several value chains and acts as a solution provider to other sectors of the economy, it plays a pivotal role in leading a sustainable recovery. Today, chemical innovations already contribute to several sustainable development challenges such as energy and climate, transport, health and food, among others.

The chemicals and materials sector can leverage both direct and indirect stimulus programmes, and can strengthen their broader impact to provide shared value across business and society. Here's how:

- Speeding up critical value chains for chemicals and materials. Some elements of the stimulus, such as short-term work schemes, offer immediate help. However, much of the stimulus aimed at restoring consumer income and spending cannot be dispensed fast enough to make a material difference to upstream industries. The problem is made worse by the time it takes for chemicals to realize returns from customer demand for those goods further down the value chain – for instance, Accenture analysis found that a molecule leaving a chemical plant takes on average 88 days to reach the consumer, for example as part of a motor vehicle.

- Including incentives to support a 'build back better' approach. In key economies analysed by Accenture, only 5% of the stimulus total is targeted at incentivizing structural change in industries, such as progressing environmental objectives (see figure below). The bulk of stimulus funds flows into general programmes such as cash transfers to citizens, liquidity support for companies or tax relief. While these measures are important, they are more likely to support a return to the previous status quo, rather than opportunities to innovate and improve resilience in the chemical sector and downstream industries.

Below are some examples of how direct and indirect stimulus packages have impacted the chemicals and materials sector.

Direct:

- China introduced higher export subsidies for petrochemical products and launched billion-dollar investments in a total of 16 refineries and petrochemical projects.

- Several EU countries, the US and Japan are incentivizing the creation of local pharmaceuticals clusters. For instance, France aims to move production of paracetamol back home. Japan offers subsidies to firms reshoring manufacturing of pharmaceuticals.

Indirect:

- Germany’s green hydrogen strategy includes a $10 billion budget – multiple times the current German hydrogen market, but still a small portion of the country’s overall electric energy sector.

- The EU is backing e-mobility subsidies, with a plan worth $91 billion – 250% of the EU's electric vehicle market (worth $37 billion in 2019, according to estimates by Allied Market research).

Where next?

Strengthening the recovery through stimulus measures relies on how and how fast resources are allocated. Here are three actions chemical sector leaders can take:

1. Build infrastructure to support more resilient and more sustainable socioeconomic systems. With 83% of consumers saying it’s important for companies to design products that can be reused, recycled and never go to a landfill, the chemical industry needs to tackle the huge infrastructure investment that is the foundation of its transformation towards greater sustainability. For example, the transition to a circular economy requires investment to encourage greater transparency in waste streams (circular track and trace), establish end-of-life collection systems for further material classes, develop chemical recycling processes, and build the necessary physical assets. This can only be achieved by collaborating in regional clusters, which represent ideal opportunities for stimulus support.

2. Leverage stimulus packages to innovate and support broader sustainability goals. The chemicals industry has an opportunity to engage with policy-makers and demonstrate their essential contribution to realize ambitious policy goals. As an example, industry innovators may further support the transition to cleaner mobility. The industry already provides a range of solutions that make transport more energy efficient. The future of mobility, with fleets of autonomous and/or electric vehicles, may require a new spectrum of materials and chemicals to make everything from batteries to simplified powertrains and customizable interiors. The contribution of the sector to the development of advanced biofuels, green hydrogen, sustainable battery materials or recycling technologies will be crucial to enabling this transition.

3.Stimulate a new wave of innovation through a collaborative ecosystem. By engaging with value chain partners, governments and start-ups, the chemical industry can build an ecosystem that drives the next wave of innovation. To make this happen, chemical leaders can partner with start-ups to tap into new sources of (digital) innovation. For example, in the recycling space alone, there are hundreds of relevant start-ups across the world that are working with new technologies – but these cannot scale without additional funding.The time is ripe for a new wave of corporate and public venturing to accelerate the process of bringing these technologies to the market.

Build back better

The chemical industry has navigated crises before through diligent fixed-cost restructuring, level-headed portfolio management, and applying a 'lean lens' to its processes. Now there is an opportunity to show how people and planet are the real drivers for business. By capitalizing on cross-sector innovation and collaboration, the chemical industry can not only build back better, but also secure its role in the post-COVID era with its improved products, services and technologies.

This blog was written with contributions from Simonetta Rima (World Economic Forum), Simone Paes (Accenture), David Apel (Accenture) and Bernd Elser (Accenture).

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Chemical and Advanced Materials

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Industries in DepthSee all

Kingsmill Bond and Sumant Sinha

March 25, 2026