Why renewables are the cornerstone of the global energy transition

Renewable energy, energy efficiency and electrification are key to energy transition Image: Dan Meyers on Unsplash

Listen to the article

- It's now clear that renewable energy, energy efficiency and electrification must be the drivers of the deep decarbonization we need.

- New analysis from IRENA finds that renewables are now the cheapest form of energy - and capacity is set to rise significantly over the next few decades.

Addressing climate change requires us to decarbonize both energy supply and demand by 2050. The US, Europe and China have committed to net zero or carbon neutrality by mid-century. Others are following suit. This will have a profound effect on the global energy transition, placing electricity as a key vector in decarbonizing the entire energy sector.

The latest insights from IRENA’s World Energy Transitions Outlook were released on 16 March at the Berlin Energy Transitions Dialogue. It provides in-depth analysis of what these effects will look like, starting from the Paris Climate agreement objective of limiting climate change to well below 2˚C and with an effort for 1.5˚C by the end of this century. While several options are being considered for a deep decarbonization, it is clear that renewable energy, energy efficiency and electrification are at the centre of the global energy transition.

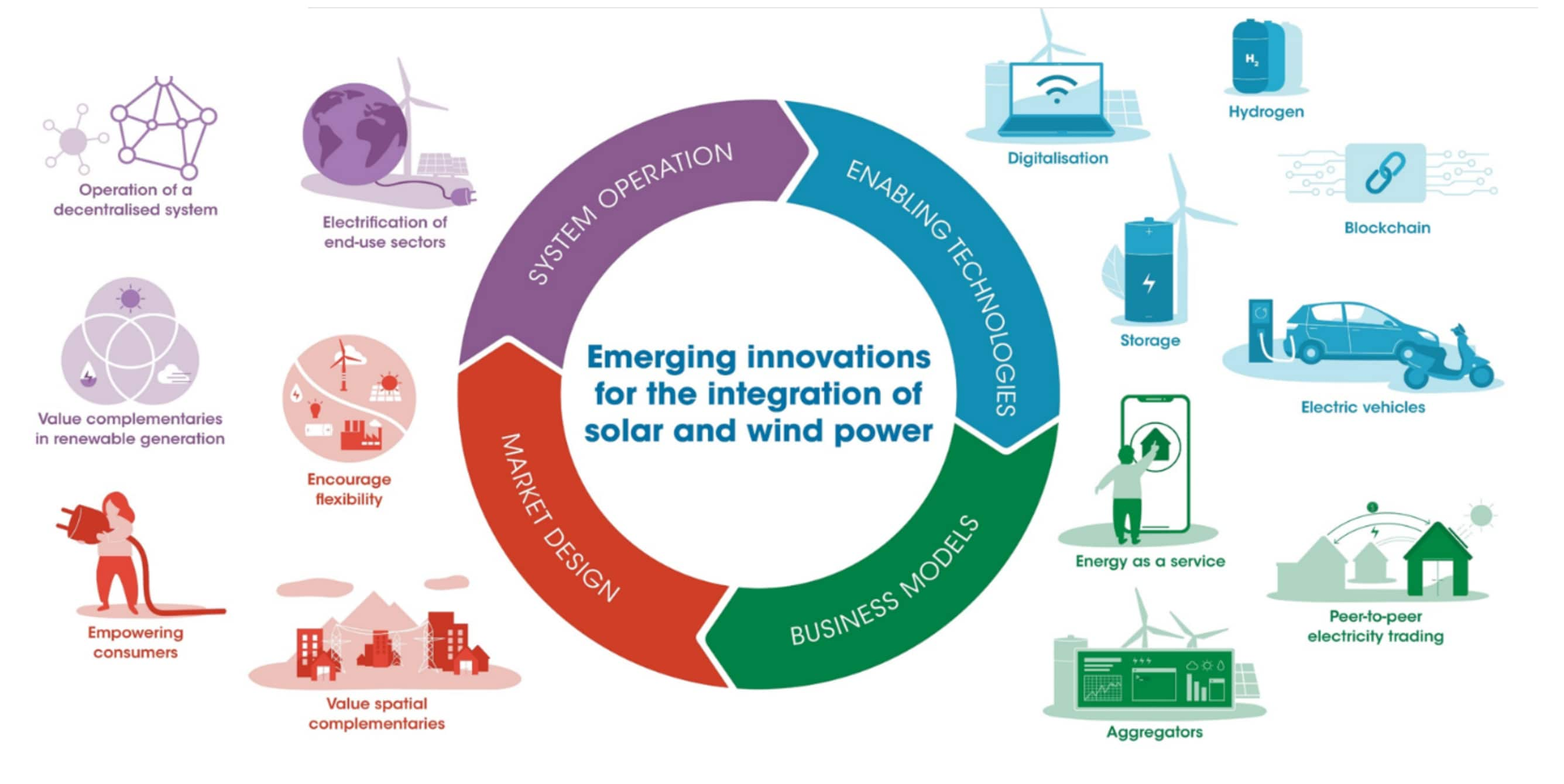

Renewable energy and global energy transition

While climate change mitigation is a powerful driver behind the shift away from fossil fuel-based power generation, this is not the only driver. At the same time, renewable power has become the cheapest form of electricity generation and the costs continue to fall thanks to improvements in technology and economies of scale. The share of renewable power continue to rise from year to year, with nearly 30% renewables in the global power mix at present and renewables dominating yearly capacity additions (see Figure 1, below).

New IRENA analysis indicates a continued swift energy transition to renewable power generation worldwide in the coming three decades, with shares of variable (or intermittent) renewables – solar PV and wind – growing especially rapidly. Variable renewables will dominate the world's total power supply by 2050, a major change from today’s situation. Yet experience from around the world shows it is possible to operate power systems with high shares of variable renewables, as witnessed in Germany, Ireland and the UK, amongst others. During 2020, despite the COVID-19 pandemic, the share of renewables (mainly variable) in total electricity generation was 40% in Europe, a more than 4% increase in the share in comparison to 2019. Most notably, the share of other generation sources fell in Europe over the same period between 6% and 16%, as in the case of coal-based generation.

Increasing flexibility to smoothen energy transition

The operation of power systems with a high share of variable renewables requires much higher flexibility. Today, dispatchable fossil plants (that is, plants that can generate electricity on demand) provide that flexibility, but this will change going forward as their role declines. IRENA has identified 30 options for increasing flexibility across four main pillars: hardware, markets and regulations, and operational practices and business models (see figure 2, below). This toolkit of options must be deployed in the context of each power system’s specific characteristics. Especially the demand side offers interesting possibilities, as the electrification trend results in new loads connected to the system -such as electric vehicles, behind-the-meter batteries and heat pumps- which if operated smartly can support grid balancing. This is helped by rapid digitalization of power systems. Time-of-use pricing, aggregators, Demand Side Management are some of the strategies that benefit from digitalization and smart grids continue to expand worldwide. Still many transmission and distribution grids will require expansion and upgrading in order to deal with the new power system realities.

Also, regulations and grid codes need to be adjusted in order to enable to full deployment of the new flexibility options. This is an area that warrants more attention.

Electrification, including buildings, transport and industry, as well as the production of green hydrogen, will play a key role in a net-zero CO2 emissions future.

IRENA analysis suggests that up to a quarter of all electricity will be used for the production of green hydrogen. At the same time, a massive shift will occur towards electrification of road transportation while synfuels produced from clean hydrogen will play an increasing role in aviation and shipping. Whereas better building efficiency will reduce the need for heating and cooling, this is balanced by a shift to electric heat pumps. The analysis suggests that direct electricity use and indirect electricity use for the production of green hydrogen and derived synfuels may account for 60% of total final energy use by 2050, up from around 21% today. As a consequence, electricity demand will grow 3-4 fold from today’s level. This represents a massive shift; the electricity sector will become the central pillar of global energy supply and demand, a much bigger role than it has played in previous decades. Traditional incumbents in the energy sector, such as oil and gas companies, are already eyeing this trend and developing strategies to become electricity market players. It remains to be seen who will become the dominant player in this market in coming decades.

Given the growth in electricity demand and the shift to renewable power a massive expansion of clean power generation will be needed and infrastructure planning must be ramped up accordingly. The investment needs are hefty and it is critical to ensure that the infrastructure rollout speed is commensurate with the needs of the energy transition. This will require further streamlining of planning and approval processes.

IRENA continues to work with its 164 member countries to devise and implement renewable energy transition strategies for power sector transformation based on its Innovation Toolbox, Flextool, power systems planning and grid studies.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Decarbonizing Energy

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Climate Action and Waste Reduction See all

Shinnosuke Komiya and Chitresh Saraswat

July 3, 2026