What is the ‘protocol economy’ and how is it impacting the crypto world?

The “protocol economy” uses cryptocurrencies to incentivize blockchain actors. Image: Getty Images/iStockphoto

- Blockchain and tokenization can bring operational efficiency, transparency and real-time record-keeping to traditional asset management.

- Token economies drive decentralized innovation: the “protocol economy” uses cryptocurrencies to incentivize everyone along the chain and increase network effects.

- Tokenization is a structural shift much like other technological waves, such as the internet and cloud computing.

As a global investment management firm, Franklin Templeton’s journey into digital assets started in 2019, setting out to test a simple hypothesis: might new distributed blockchain ledgers offer operational efficiencies and cost savings for our organization?

At the time, we ran our own transfer agent functions to manage hundreds of investor records and company transactions for our mutual funds – a ledger-intensive activity. We wanted to understand the impact of moving that record-keeping onto the blockchain.

In 2019, we filed with the Securities and Exchange Commission to launch a tokenized version of a US government money market fund. This allowed the transfer agent to calculate yield, with the shareholder record updating daily, offering a good test for how well distributed ledgers might work.

However, technology suitable for a regulated investment firm was lacking. No platforms could create and manage registered token securities and no cryptographically protected wallets to process know your customer or anti-money laundering information.

As a result, we began to build our own technology, designing and launching our patented Gemio wallet solution, Benji infrastructure stack and blockchain-based transfer agent to issue and manage digitally native token-based securities and register fund ownership via the public blockchain.

We launched our Franklin On-Chain US Government Money Market fund (FOBXX) in early 2022 and have been running that product’s shareholder record exclusively on blockchain ever since, with more than $700 million in assets under management on-chain today in the fund.

Learnings about the ‘protocol economy’

Our first learnings about blockchain – and its “protocol economy” involving open participation, decentralized ownership and community-driven governance – emerged quickly.

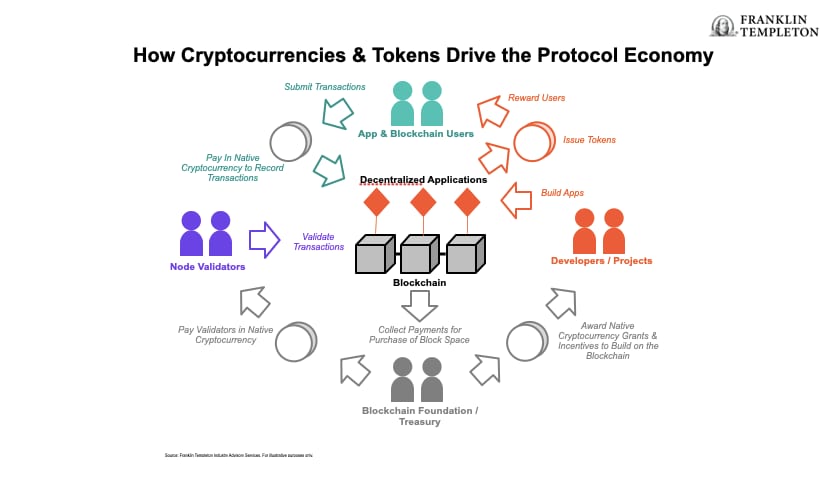

To record our transactions, we needed to pay in the native token of that blockchain, so we had to hold these coins in our treasury. Blockchains issue coins to incentivize validators – those in the chain who verify transactions – to ensure the integrity of transactions.

Such payments help offset the inflationary pressures of coin issuance. We realized that we would need to become a verification node in these networks to maintain the value of our treasury holdings.

Many novices to the crypto ecosystem doubt that individuals, enterprises or institutions will want to use cryptocurrencies to pay for goods or services. What they miss is that the purpose of these coins is to pay for block space on the blockchain ledger.

The cryptocurrency issued by the blockchain is the mechanism that drives its network effects by rewarding validators and encouraging them to validate even more transactions, thereby increasing the value of the tokens they hold.

Another learning, as we expanded our technology and investment activity across multiple blockchain ledgers, was that each of these venues not only uses their cryptocurrency to build their network but also award coins to developers and projects as incentive to create applications that operate on their ledger.

The more development work done on the network, the more coins earned and the more committed the developers become to that network’s success. These blockchains are, therefore, like digital nation-states, with entrepreneurs building their businesses and becoming increasingly vested in the network through accumulating the platform’s coins.

Our final learnings related to how commerce occurs on these platforms. Tokens issued by these networks are programmable. Each blockchain publishes smart contract templates and creates a library of basic building blocks or digital primitives to enable specific functions and allow entrepreneurs to build interoperable applications.

These offerings are like LEGO, allowing for multiple types of applications to integrate and communicate with each other automatically. They are free, open-source protocols for transaction-related functions.

These open-source functional protocols are especially powerful because they allow one application’s functions to be automatically incorporated into another’s to encourage growing consumer engagement and build network effects among users.

For example, a decentralized social media app may allow users to book a car directly from their user interface by incorporating the “reserve a car” function from a decentralized ride-sharing app.

That could, in turn, allow a user to have dinner delivered by any restaurant on their route by embedding a “place food order” function from a decentralized food delivery app on top of each eligible restaurant displayed on the ride-sharing app’s geo-locational map.

This entire transaction chain could occur without development work or contractual agreements between the three app providers.

Each action would create a transaction. The more transactions there are to record, the more demand there is for the blockchain’s native cryptocurrency to pay for these transactions. To drive this flywheel, applications reward users by giving them tokens to recognize their contribution to the application’s and blockchain’s success.

The decentralized social media, ride-sharing and food-delivery apps may each award tokens. This builds a community of incentivized users and further drives network effects. The growth of each app and the underlying network helps drive the value of the blockchain’s cryptocurrency and the app’s tokens higher. These dynamics are illustrated in Exhibit 1.

A driver of economic growth

Having built our digital asset infrastructure natively within the blockchain ecosystem, Franklin Templeton now understands that these protocols will likely transform how the economy operates and drive our next wave of growth. We built an investment team focused exclusively on these token-based opportunities to deliver that growth to our investors.

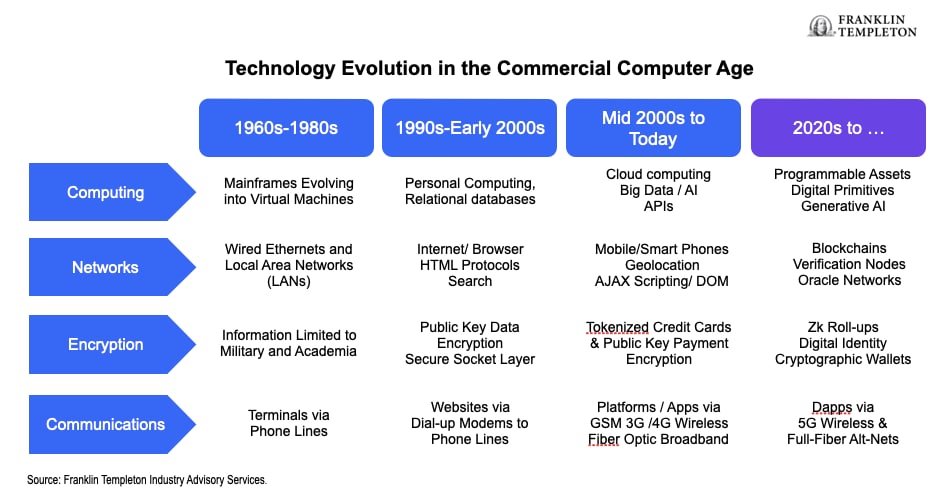

As Exhibit 2 shows, four technologies define the “Computer Age” – computing, networks, encryption and communications. Each has seen three periods of advancement, beginning in the mid-1960s, when miniaturization of electronic components allowed the first commercial computers to emerge.

Blockchain and the protocols described in this paper mark a fourth wave of innovation.

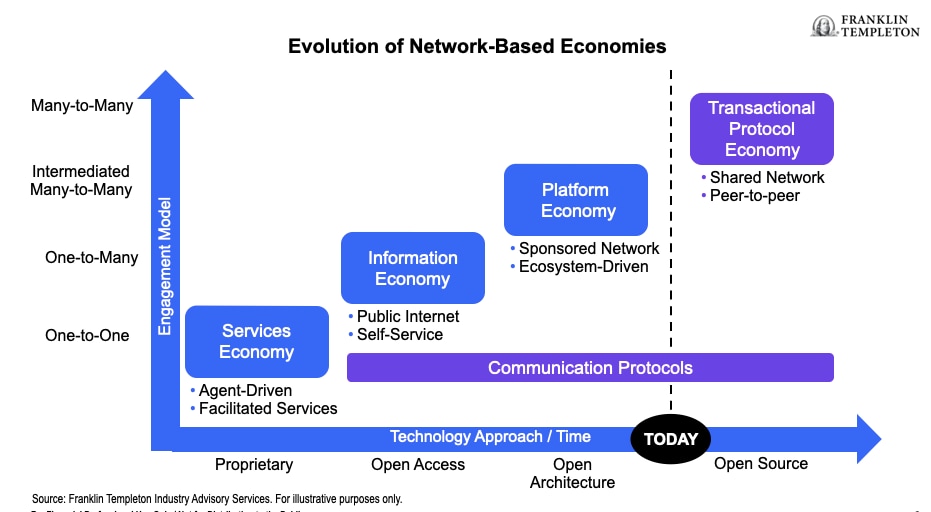

These technologies are enablers of networked economies. Until the late 1980s, the networks they spawned were proprietary. For example, airlines developed the SABRE system to automate airline bookings.

The increase in productivity was transformative, allowing a single agent to complete a transaction with a client much more quickly, servicing many more clients, leading to a services economy. This began to change in the 1990s, as shown in Exhibit 3.

Personal computers, the internet and open-source communication protocols paved the way for the information economy, where one website could now offer services to many individuals simultaneously and those individuals could complete tasks themselves without needing an agent. This once again spawned a considerable surge in consumer activity.

A third evolution in the 2000s to 2010s saw the emergence of cloud-based, open architecture ecosystems driven by powerful intermediaries. Platforms emerged connecting many buyers and sellers.

Access was controlled, however, by the platform itself, accruing significant value to the platform provider and its shareholders, although often at the expense of the consumers and businesses that drive the platform’s network effects.

Today, transactional protocols and blockchains are moving us towards a more open-source, decentralized economy driven by peer-to-peer without an intermediary directing activity or taking a disproportionate share of profits.

Cryptocurrencies and tokens may be unfamiliar and daunting to many. Still, they are incentivization mechanisms meant to align the interests of consumers and businesses and allow for powerful platforms to emerge, driven not by a centralized player but by network effects that economically reward all participants.

This vision is increasingly being recognized globally. For example, the World Economic Forum’s 2023 Tokenization in Financial Markets report outlines how tokenization can reshape capital markets by enabling greater efficiency, transparency and accessibility.

Its research aligns with our findings, reinforcing that tokenization is not a niche innovation but could redefine how financial systems operate.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Blockchain

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Marcelo Bicalho Behar

June 19, 2026