How Asian businesses are using value chain decarbonization to drive growth and sustainability

Image: Reuters/Athit Perawongmetha

- Decarbonization of Scope 3 emissions along value chains is a complex and significant challenge for many corporates.

- This is particularly challenging in Asia, which is home to much of global output and trade in intermediate goods.

- The World Economic Forum's Accelerating Value Chain Decarbonization for Corporate Growth: Perspectives from Asia report highlights opportunities from value chain decarbonization action across industries in the region.

Scope 3 decarbonization is one of the most complex and significant frontiers of corporate action, as the emissions along the value chains usually account for the majority of corporate carbon emissions across industries, yet they operate beyond companies' direct control.

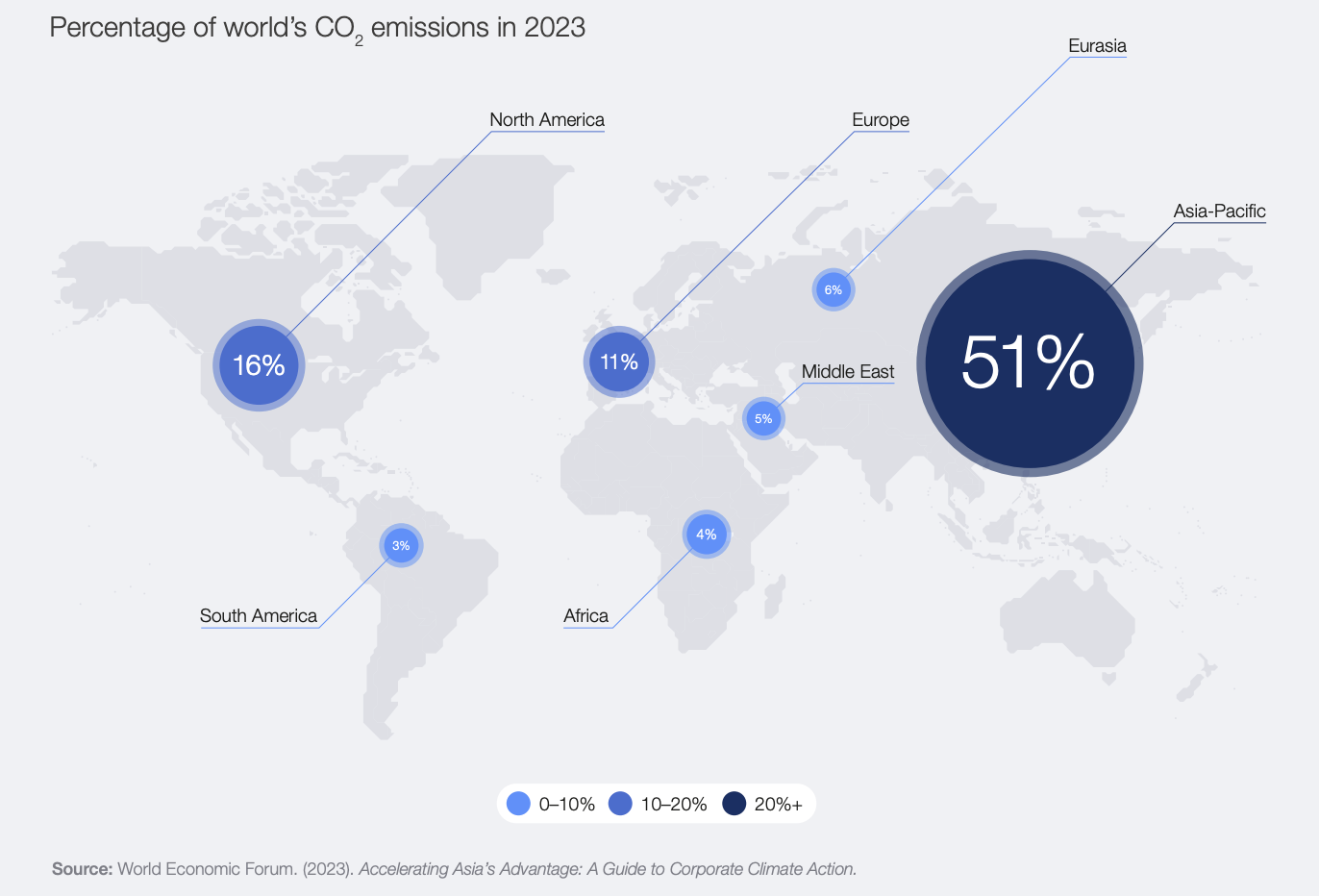

For Asia, this is particularly challenging given it has been home to much of the world's industrial output and still holds more than one-third of global trade in intermediate goods. Its extraordinary manufacturing capacity and position as a trade nexus also means its accounts for half of the annual global carbon emissions. Meanwhile, Scope 3 emissions usually make up 65-95% of a company's carbon footprint, while actions to reduce them often remain inadequate.

However, the story of Asia's Scope 3 emissions is not just one of challenge but also one of opportunity. It is increasingly clear that the region is becoming a key driver for global growth and green innovation.

For instance, Asia powered over half of the global GDP growth in 2024, topping some of the critical green innovations such as photovoltaics, power batteries and electric vehicles, and has the fastest growing number of companies validated with science-based climate targets, with a forecast increase of 134% between the end of 2023 and the end of the second quarter of 2025.

The World Economic Forum's white paper Accelerating Value Chain Decarbonization for Corporate Growth: Perspectives from Asia, highlights opportunities from value chain decarbonization action across industries in the region, and outlines both near-term actions and long-term strategies for success. The leading industry use cases from Asian businesses collectively make the case that decarbonization is not merely a cost, but a catalyst for transformation and value creation.

The business case for value chain decarbonization in Asia

By tackling emissions across their value chains, companies can not only identify and mitigate the physical and transition risks that threaten supply chains and asset values, but also enhance overall resilience.

Strengthening operational efficiency among suppliers and downstream partners improves cost structures and supports more reliable access to capital. At the same time, accelerating value chain decarbonization sharpens business competitiveness and opens new sources of growth, as customers, regulators and investors increasingly prioritize low-carbon products and transparent, sustainable supply chains.

Here are three areas which enhance the business case for value chain decarbonization in Asia.

1. Addressing physical and transition risks

CDP data indicates that in the Asia-Pacific region, an average of 79% of companies identified environmental risks with substantive financial impacts – above the global average of 67% – making it the region where awareness of environmental risk is most widespread. Companies across Asia recognized the materiality of climate-related risks, with policy (32%) and acute physical risks (19%) emerging as the dominant concerns.

Extreme weather events and the readiness of domestic carbon pricing and emerging trade-related regulatory frameworks are reshaping the business landscape. Companies that act early are better poised to avoid rising compliance costs, enhance supply chain resilience and strengthen investor and customer confidence.

2. Enhancing efficiency and financial performance

Improving energy efficiency and optimizing resource use remain fundamental steps for reducing direct operational emissions, and they also act as a critical catalyst for decarbonization across the broader value chain.

In the Asia-Pacific region, companies report an average financial gain of $36.5 million from environmental action against an investment of $4.5 million – an eight-fold return. The most impactful emissions-reduction measures in the region include energy-efficient production processes and the deployment of low-carbon energy sources. This inside-out approach provides a strong platform for attracting investment, enhancing resilience and securing long-term competitiveness in a low-carbon economy.

3. Elevating competitiveness and unlocking new revenues

The transition is no longer merely a matter of regulatory compliance; it has become a source of competitive advantage and a catalyst for new revenue opportunities. For example, by investing in the reuse of construction waste, SCG's (Siam Cement Group) circular economy initiatives not only lower the carbon intensity of cement production but also extend the life cycle of materials.

Meanwhile, China State Construction Engineering Corporation started to develop its carbon assessment consulting service after having continued to optimize its own group-wide carbon emission assessment for three consecutive years with capabilities significantly enhanced.

By developing low-carbon products, circular business models and innovative green solutions, companies can meet accelerating customer and stakeholder expectations for sustainable value chains.

At the same time, growing market segments shaped by low-carbon demand are expanding commercial opportunities and strengthening brand value. Embedding sustainability into core business strategy therefore not only mitigates risk but also enhances market positioning and supports long-term profitability.

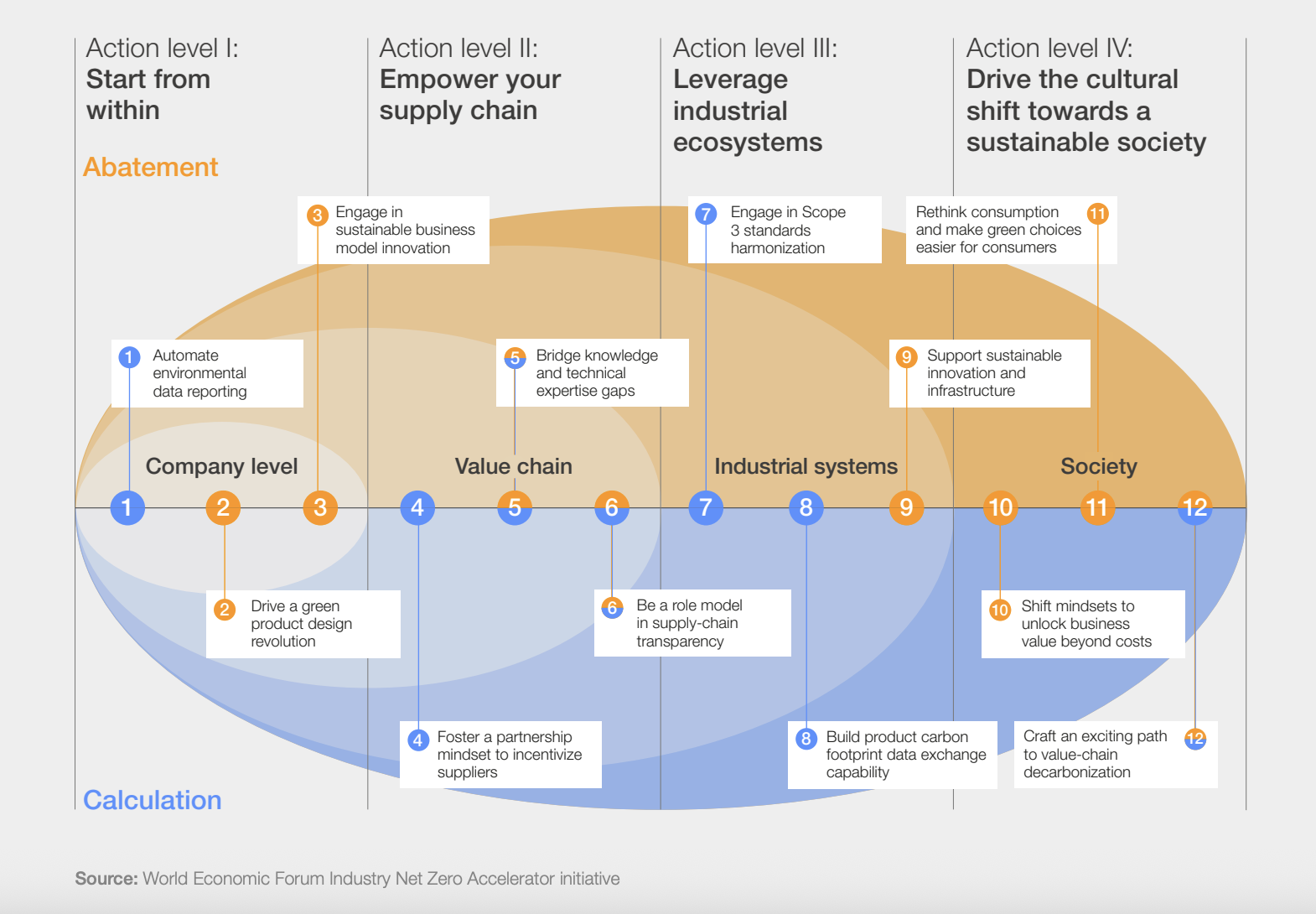

Four-step blueprint to galvanize companies into action

Aligned with the World Economic Forum’s No-Excuse” Opportunities to Tackle Scope 3 Emissions in Manufacturing and Value Chains white paper, we provided some region- and context-specific use cases from leading companies that shed light on how corporate action on value chain decarbonization could reduce carbon emissions across the scopes, and more importantly, how these empower them to translate these actions into short-term gains as well as long-term value creation.

Here is the four-step blueprint to encourage companies into taking action.

1. Start from within: strengthen internal governance and carbon management

Proactive target-setting has become a strategic necessity. Companies that adopt science-aligned goals and measure carbon impacts at both corporate and product levels demonstrate operational maturity to global investors and buyers, reducing transition risks and unlocking access to green finance.

2. Empower the supply chain: collaborate and share resources to enable chain-wide decarbonization

Supply chain engagement is essential for reducing Scope 3 emissions. Value chain leaders that co-invest in supplier capabilities can shift relationships from being transactional to truly strategic. Shared data platforms, cost-sharing models and a partnership mindset help close capability gaps, distribute transition costs and reduce systemic risks.

For example, by 2025, Siemens had assisted more than 500 key suppliers in China to accelerate their carbon reduction journey, playing an important role in supporting Siemens globally to reduce CO₂ emissions in its own operations by 60%.

3. Leverage industrial ecosystems: promote standardization and platform-based transformation

By creating unified protocols, shared infrastructure and digital platforms, industrial ecosystems can reduce duplication, lower transaction costs and accelerate adoption of low-carbon solutions.

For instance, digital energy company Envision’s zero-carbon industrial park model – integrating green power, energy storage, green fuel, and unified carbon-management platforms – has been elevated from a pilot into an emerging national standard with replications across multiple countries globally.

Meanwhile, State Grid Corporation of China has built a trillion-yuan procurement and supply chain management platform, saving RMB77.783 billion ($11 billion) in procurement costs, with 147 green warehouses and 33 zero-carbon warehouses developed.

4. Drive cultural and social shifts: make low-carbon development a shared value

Moving from a mindset of minimum compliance towards genuine ownership of climate goals is essential for lasting impact, and the transformation requires embedding low-carbon values across organizations and society.

E-commerce company JD.com, for instance, illustrates this through its SCEMP-AI platform, which aligns with international standards and innovatively links merchant emissions reduction with consumer incentives, having achieved more than 700 tons of carbon emission reduction even during its pilot phase.

Value chain decarbonization is a strategic opportunity

Value chain decarbonization is not a burden for businesses – it is a strategic opportunity for Asian businesses to pursue sustained growth in line with our climate and broader environment goals. The transition is estimated to unlock a potential market of $3 trillion.

With aligned support across policy, finance, technology and culture, businesses in Asia can transform fragmented actions into systemic industrial advantages and prepare themselves as a global leader in the transition towards a low-carbon economy.

The future belongs to companies and regions that integrate climate action into core strategy and drive growth through green innovation, and Asia looks well placed to lead.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Energy Transition

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Climate Action and Waste Reduction See all

Shantanu Srivastava and Tanya Rana

March 5, 2026