The new investment race does not have to become a new development divide

AI is attracting a growing share of international investment. Image: REUTERS/Priyanshu Singh

Nan Li Collins

Director of Investment and Enterprise, United Nations Conference on Trade and Development (UNCTAD)Sean Doherty

Head, International Trade and Investment; Member of the Executive Committee, World Economic Forum- Global foreign direct investment rose in 2025 but the recovery is fragile and increasingly concentrated.

- Strategic sectors such as artificial intelligence (AI) infrastructure, semiconductors, critical minerals and clean technologies are attracting a growing share of international investment.

- Developing countries need realistic entry points into these value chains, not an unwinnable subsidy race with larger economies.

Global investment rose in 2025, but the headline figure hides a more important shift: capital is becoming more concentrated, more selective and more closely tied to the industries that will shape future growth.

Artificial intelligence (AI), data centres, semiconductors, critical minerals, energy-transition technologies and advanced manufacturing are no longer marginal investment categories. They are becoming the infrastructure of future competitiveness.

This is creating a new geography of investment. Capital is flowing towards countries with technological capacity, large markets, skilled workforces, reliable infrastructure or strategic natural resources.

For many developing countries, the risks include receiving less investment and being excluded from the value chains that will define future production, trade and development.

Investment is rising but becoming more concentrated

According to the UN Trade and Development’s World Investment Report 2026, global foreign direct investment rose to $1.6 trillion in 2025. Yet the recovery remained fragile. Much of the increase was concentrated in developed economies and in a limited number of capital- and technology-intensive sectors.

Announced investment projects were driven largely by data centres, followed by oil and gas and semiconductors, while many other sectors, including parts of manufacturing, infrastructure and renewable energy, recorded weaker activity.

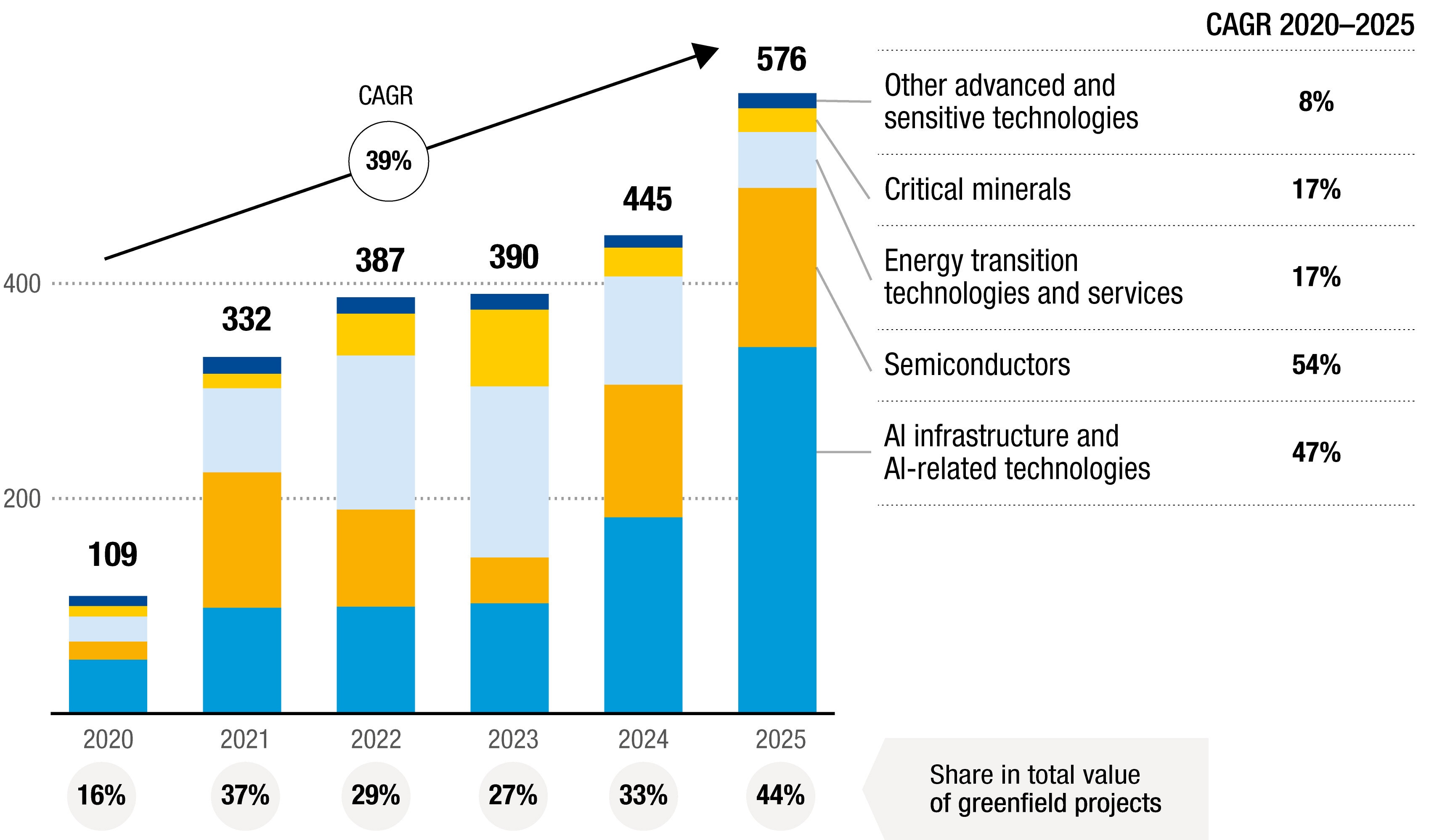

Announced greenfield investment in strategic sectors increased from $109 billion in 2020 to $576 billion in 2025. Their share of global greenfield investment rose from 16% to 44% over the same period.

Yet this boom is highly uneven. Low- and lower-middle-income economies attract only about 10% of global greenfield investment in strategic sectors, compared with more than 20% in other sectors.

This reflects real economic needs. AI requires computing power, data centres and digital infrastructure. The energy transition requires critical minerals, batteries, grids and clean technologies. Supply chains for semiconductors, electric vehicles and advanced manufacturing need to become more secure and resilient.

Policy is also playing a larger role. Governments are using incentives, subsidies, local content requirements, investment screening and strategic investment promotion to influence where capital goes and what it does.

In 2025, they adopted a record number of investment policy measures. Most remained favourable to investors but were increasingly targeted at specific sectors, technologies and projects. Incentives accounted for half of all favourable measures, while restrictions also expanded in areas linked to national security and local value creation.

This marks a shift from an era in which investment policy focused mainly on openness to one in which investment policy is increasingly strategic. The challenge is that not all countries can compete on equal terms.

A strategic investment boom can still become a development divide

Major economies have the fiscal space, institutional capacity and market size to offer large support packages for semiconductors, clean technologies, data infrastructure and other strategic sectors. Many developing countries do not. For most of them, competing through subsidies is not a realistic option.

The risk is that public support in major markets pulls investment towards places that were already well positioned, reinforcing existing advantages.

At the same time, traditional pathways into global production are narrowing. For decades, many developing economies used labour-intensive manufacturing as an entry point into global value chains.

That path is becoming more difficult. Investment in manufacturing is increasingly shaped by automation, digital capabilities, supply chain security, regulatory compatibility and proximity to major markets.

Broadening participation in fast-growing industries

Developing countries are not without opportunities. Many have assets that are highly relevant to the new investment landscape, including critical minerals, renewable energy potential, young workforces, growing digital markets, regional trade platforms and emerging industrial capabilities. The question is how to turn those assets into investable opportunities.

The starting point is realism. Not every economy can build a full semiconductor industry or compete to host the largest data centres. However, many can participate in specific segments of value chains: mineral processing, component manufacturing, business services, digital infrastructure maintenance, renewable energy equipment, logistics, recycling or climate-resilient infrastructure.

The harder task is building the investment ecosystem around those entry points. Investors look at infrastructure, energy reliability, skills, supplier networks, regulatory certainty and the speed of administrative procedures.

Targeted incentives can help but they work best when they are tied to clear development outcomes, such as training, technology transfer, local supplier development or environmental performance.

Countries also need safeguards that are credible without becoming blunt restrictions. Investments in digital infrastructure, critical minerals, energy systems or sensitive technologies may raise legitimate public-interest concerns.

However, broad restrictions can also deter needed investment. Transparent, risk-based mechanisms can help manage security concerns while preserving predictability for investors. Regional cooperation can also help countries overcome scale constraints by building larger markets, shared infrastructure, common standards and cross-border industrial corridors.

Businesses should be part of this shift. They can build local supplier relationships, invest in training, support technology transfer and use regional platforms to diversify production.

International institutions can help reduce risk, improve project preparation and support the policy frameworks that make investment more development-oriented. Importantly, business and government need to cooperate to tell the story of successful investments in developing economies, helping others to follow.

The race for strategic industries is understandable. Governments want secure supply chains, technological capacity and economic resilience. Companies want reliability, speed and access to growing markets.

However, if strategic investment remains concentrated in a small number of economies, the global economy will become less diversified and less resilient. The goal should be to widen investment participation in these.

Developing countries should also have the choice to build credible entry points into the value chains that will shape future growth. That is where national policy, business investment and international cooperation now need to focus.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Oil and Gas

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Trade and InvestmentSee all

Tim Stekkinger

July 6, 2026