5 ways a climate deal would benefit the economy

We know that Paris could determine our ability to keep global warming below 2 degrees and avoid its catastrophic impacts. But it will also be a key determinant of future economic growth and development.

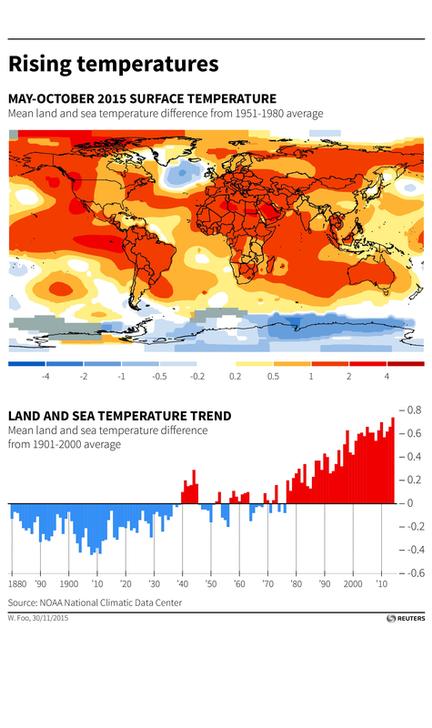

If we don’t act, climate change could have devastating impacts on overall growth and wipe out development gains of the last century. The costs are becoming increasingly clear – some studies estimate that the world has already spent $2.7 trillion more on natural disasters than usual in the last decade.

And we can’t forget the human costs. It is the world’s poorest – who are least responsible for climate change – who stand to lose the most. Runaway climate change would condemn millions to a life of poverty and cause us to fail to meet the Sustainable Development Goal of eradicating extreme poverty by 2030. This is not an acceptable outcome.

Beyond the imperative of avoiding these disastrous impacts, there’s actually a strong economic opportunity in addressing climate change. As the Global Commission on the Economy and Climate has extensively researched, low-carbon investments would bring multiple economic benefits, including growth, jobs and long-term resilience. At Unilever, we’re already starting to see the results of our ambition to decouple growth from our environmental footprint. Not only have we made substantial savings from eco-efficiency in our factories, we’re also seeing that our most sustainable brands are our best performers.

At Unilever, we’re already starting to see the results of our ambition to decouple growth from our environmental footprint. Not only have we made substantial savings from eco-efficiency in our factories, we’re also seeing that our most sustainable brands are our best performers.

The business and economic case for a strong agreement in Paris is clear. A strong deal in the Paris climate conference would encourage businesses and investors to contribute to building a low-carbon and more resilient global economy in five important ways:

- Stimulating innovation and investment in renewable energy

With 40% of the world’s electricity still coming from coal, we’ve got a real opportunity to redefine how we power our businesses and economies in the coming years. Renewable energy could reduce emissions but also create jobs and improve public health. The U.S. solar industry is creating jobs twenty times faster than the overall economy.

Even without further innovation, the International Energy Agency estimates that investing in energy efficiency measures that are already available today would boost cumulative economic output by $18 trillion by 2035.

- Safeguarding the true value of our forests

Forests are often greatly undervalued, even though they supply ecosystems critical for food security and biodiversity, provide a source of livelihoods for 1.6 billion people, and play a critical role in climate change. They have the potential to absorb and store about 10% of global carbon emissions projected for the first half of this century, provided we conserve them and stop further emissions from deforestation.

Paris is an opportunity to commit to doing more by working together to pursue ‘triple win’ opportunities to reduce emissions by protecting forests, increase agricultural productivity and food security, and improving rural livelihoods.

One promising route forward is the potential for place-based partnerships for forest protection and agricultural production – the so-called Produce and Protect approach to source commodities only from areas that cause zero deforestation.

- Growing and using more food per hectare

One of the most striking of the Sustainable Development Goals is the world’s determination to end hunger, improve nutrition and promote sustainable agriculture by 2030. Climate change is a major threat to achieving this goal, reducing crop yields, pushing prices up and increasing food insecurity.

We need to increase the amount of food we grow per hectare, reduce food waste – in our fields and plates, restore 25% of the world’s agricultural land which is severely degraded, and find sustainable models to feed around 10 billion people by 2050.

Conscious of the great potential to make agriculture more efficient and sustainable, business leaders like Strive Masiyiwa of Econet Wireless are helping people to see it as an economic opportunity, not just a moral imperative.

- Accelerating low-carbon development in the world’s cities

One of the most striking trends of our time has been rapid urbanization – around half of the world’s population lives in cities, and this is expected to reach 70%, or 10 billion people, within 30-40 years.

In the next 15 years alone, around $90 trillion will go into urbanisation. This gives us a tremendous business opportunity to build low-carbon, more resilient cities that can generate stronger growth and improve our quality of life. This means developing public, non-motorised and low-emission transport, and putting in place renewable energy and efficient waste management.

- Making long term investments in the low carbon economy

Many businesses are already vocal supporters of strong government action on climate change. Through coalitions like We Mean Business and the B Team, we have publicly called for net zero emissions by 2050 – it’s the only way we can confidently limit global warming to 2° Celsius target.

Businesses and governments need to work together and make a joint commitment if we want to address climate change effectively and quickly. Only a long-term and ambitious goal at Paris will allow us to mobilise the resources – both economic and human – needed for a transition to a low-carbon economy.

It is our responsibility as businesses to deliver ambitious solutions and technologies to bring us low-carbon, inclusive and sustainable growth. There is no excuse not to act. Let’s seize the opportunities of the low-carbon economy and create green growth that benefits all.

The author is one of 78 signatories to an open letter from CEOs to world leaders urging climate action.

Author: Paul Polman is CEO of Unilever and Chairman of the World Business Council for Sustainable Development. You can follow him on Twitter @PaulPolman.

Image: A wind farm generates electricity near bales of hay in the foothills of the Rocky Mountains near the town of Pincher Creek, Alberta September 27, 2010. REUTERS/Todd Korol

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Future of the Environment

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Climate Action and Waste Reduction See all

Planet in focus: The technologies helping restore balance – and other news to watch in frontier tech

Jeremy Jurgens

November 13, 2025