EU competition policy should not be sacrificed but trade policy should be strengthened

The EU could create a 'chief trade enforcer'. Image: REUTERS/Cathal McNaughton

In February 2019, Margrethe Vestager, the EU Competition Commissioner, blocked the proposed rail merger between Siemens and Alstom (European Commission 2019). But, trapped between heavily subsidised Chinese firms and unregulated US giants, should the EU relax its competition policy in the hope of creating its own giants? This line of reasoning has gained traction among EU policymakers. Many fear that the region's rigid competition policy is too rigid, and a disadvantage in a world where others don’t play by the same rules. Some even argue that the Union's competition policy could get in the way of its strategic objectives.

These concerns are valid, but we argue that competition policy is not the cause of Europe’s troubles. Weakening the policy would not help the EU achieve its strategic goals (Jean et al. 2019).

Concentration, profits, and investment

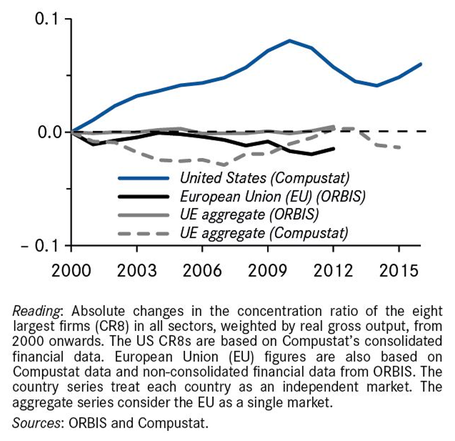

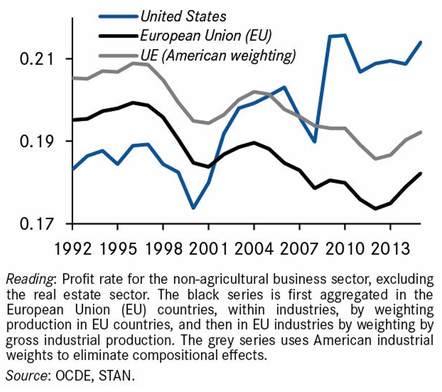

Since 2000, concentration has increased in the US while it has remained relatively stable in the EU (see Figure 1). Profit margins have evolved in a similar way. Until the early 2000s, US markets were more competitive than EU markets, with lower prices and often lower margins. These trends have reversed, with a sharp increase in profit margins in the US, but not in the EU (see Figure 2).

Figure 1 Evolution of concentration levels in the US and EU, 2000-2015

Figure 2 Profit margins in the US and EU, 1992-2015

Prices have also been affected. Comparing the evolution of prices in relation to the unit cost of labour between the EU and US, we find that between 2000 and 2015, prices increased by 15% more in the US than in the EU, while wages increased only by 7% more in the US than the EU. This is an average 8% increase in purchasing power for EU consumers (Gutiérrez and Philippon 2018, Philippon 2019).

Perhaps high margins are needed to sustain high investment? The data does not support this idea. Concentration, operating margins, and stock prices increased in the US, while investment, including intangible investment and R&D, declined. Meanwhile concentration has decreased in the EU and investments have remained (relatively) stable, despite lower profits and lower stock prices (Figure 3).

Figure 3 Comparisons between US and EU (top five concentrated US industries)

Improving EU competition policy

The EU’s competition policy is based on two pillars: consumer protection, and independence of its application by the Commission to guarantee impartiality and strengthen confidence placed in it by member states.

EU policy has been stricter in its implementation than US policy, but it is still a rare event when the commission rejects a merger. In the vast majority of cases, the Commission decides on unconditional acceptance. Between January 2010 and December 2018, 2,980 merger transactions were notified to the Commission. Of these, 2,704 were accepted unconditionally (90.7%), including 1,949 (65.4%) in Phase 1. Another 156 transactions were conditionally approved. Only seven transactions were definitely refused.

Some of these mergers, led to the creation of European giants, such as the combination of Luxottica and Essilor in eyewear, and Lafarge and Holcim in cement.

Competition policy could nevertheless be more flexible and reactive if it evolved in at least three ways.

- Behavioural measures in commitments. To allow for some flexibility – especially in markets that evolve constantly – the Commission should more frequently make use of behavioural measures. The European Court of Justice has, through jurisprudence, made these measures difficult. Behavioural commitments are sometimes costly to monitor, but they are reversible, and therefore can be adapted if events change the way markets function.

- Imposing provisional measures. Dealing with abuse of a dominant position often takes time. Delays are common, especially in highly technical cases. The Google Shopping case, for instance, took around seven years. By then, all competitors had been swept out. The Commission should be allowed to impose provisional measures rapidly.

- Addressing pre-emptive acquisitions. Finally, a new type of abuses of dominant positions have emerged in some sectors. Most important, the practice of acquiring innovative start-ups with no significant revenue to nip potential competitors in the bud (Cunningham et al. 2018). The turnover tends to be below the notification thresholds of competition regulators. But lowering the thresholds would vastly increase the number of cases to be reviewed, and so it is not an optimal solution – as the German competition authority recently found out. Imposing the value of the transaction as a new threshold isn't a solution, because these amounts can easily be manipulated. On the other hand, allowing ex-post control of mergers by the competition authority would be an efficient and flexible way to target pre-emptive acquisitions without overloading the authority.

In practice, two main problems might stop policymakers levelling the playing field. The first is the problem of dominant positions, the second of industrial subsidies.

Competition in third markets

By definition, EU competition policy is concerned only with the effects of competition in Europe. It leaves open the issue of competition in third markets. Therefore, European firms might be at a disadvantage if they have to compete in those markets with foreign firms who enjoy a dominant position in their home markets. A dominant position in the home market can affect competition in foreign markets in two ways:

- the company implements cross-subsidies (some revenues from its home market are used to subsidise low prices elsewhere), or

- the company operates in a sector where size is a decisive competitive advantage.

In case cross-subsidies significantly distort competition, there are two possible remedies. The first would be to request the opening of an anti-dumping proceeding by the importing country, as this practice corresponds precisely to the definition of dumping in trade law. The second is to bring a dispute to the WTO for the implementation of harmful subsidies. In practice, neither would be easy. This also has limited practical relevance because, to our knowledge, no one has yet proved the existence of large-scale cross-subsidies.

Empirical studies show that size is a limited source of competitive advantage. For instance, De Loecker et al. (2019) find that a 10% increase in a company’s size increases its output by 10.3% to 10.8%, implying that its productivity increases by between 0.3% and 0.8%.

Mergers frequently fail, which also implies that a larger company is not always more efficient. The groupings of Chinese state-owned enterprises orchestrated by the state-owned Assets Supervision and Administration Commission of the State Council (SASAC) were followed by a significant deterioration in their economic performance (Lardy 2018).

Size does matter in some sectors – for example, when network effects are strong (digital platforms), or when the growing importance of intangible capital creates large sunk costs. Also, when the cost of investment increases disproportionately, such as in new production tools for semiconductor foundries, or new products in the automotive, pharmaceutical, and aeronautics sectors. In such cases, poor application of competition policy in the home country is an advantage.

Unlike a subsidy, however, this distortion creates higher prices, and so the best remedy is therefore to insist upon market access reciprocity. This requires stronger transparency obligations on non-tariff measures, and on the implementation of regulations and commitments, which will mean there are fewer informal or poorly identified obstacles.

These objectives should be an important focus of the discussions about WTO modernisation. The EU should also make more strategic use of the WTO consultation and dispute settlement system for important breaches, as well as of its trade defence instruments. And it should restore reciprocity in the openness of public procurement to foreign providers.

The EU could also create a 'chief trade enforcer' to co-ordinate these policies, aiming specifically at the implementation of trade-related commitments. In practice, these would be a variety of remedies, such as enquiries about commitments application, publication of the conclusions, naming and shaming, formal requests, referral to the WTO Dispute Settlement Body, ex-officio initiation of anti-dumping and anti-subsidy investigations, or safeguard measures.

Industrial subsidies

The first-best response to industrial subsidies would be to make regulation a priority subject in WTO reform discussions, to strengthen transparency obligations and make the adoption of countervailing measures easier when subsidies are harmful. The creation of a rebuttable presumption, that non-notified subsidies would be detrimental to partners and therefore susceptible to countervailing measures – as already proposed by the EU – would be a powerful lever to change incentives in this area.

But this may not be easy or quick to do. So, we need a plan B.

Reforms of trade defence instruments and of the methodology for determining anti-dumping duties recently came into force, and they are a first step. We need a more reactive way to use these instruments when significant subsidies are identified. We must also take foreign direct investment (FDI) into account. The screening of FDI, currently limited to looking for potential threats to security or public order, could be extended to concerns about public funding, so as to avoid distortions related to subsidies, and the preservation of competition.

Finally, the EU could take more advantage of the current legal framework on state subsidies, such as the Important Projects of Common European Interest (IPCEI). This makes it possible to grant large amounts of aid to large industrial projects in a non-distortionary manner.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

European Union

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Geographies in DepthSee all

Naoko Tochibayashi

October 30, 2025