How younger investors are leading a retail investment shift

Has there been a major shift in retail investment? Image: Getty Images

- The new Global Retail Investor Outlook 2024 underscores a major shift in retail investing: younger, more diverse and traditionally underserved groups are entering the markets in greater numbers.

- Generation Z and millennials are embracing artificial intelligence and digital platforms for financial advice and education.

- The financial industry is moving toward hybrid models that combine the efficiency of automation with the trust of human advisors.

The landscape of retail investment is undergoing a significant transformation, driven primarily by the preferences and behaviours of younger investors.

Developed in partnership with Robinhood Markets and the Boston Consulting Group, the World Economic Forum’s Global Retail Investor Outlook 2024 highlighted an important yet unsurprising trend: younger investors place greater importance on intuitive and tech-enabled wealth management journeys.

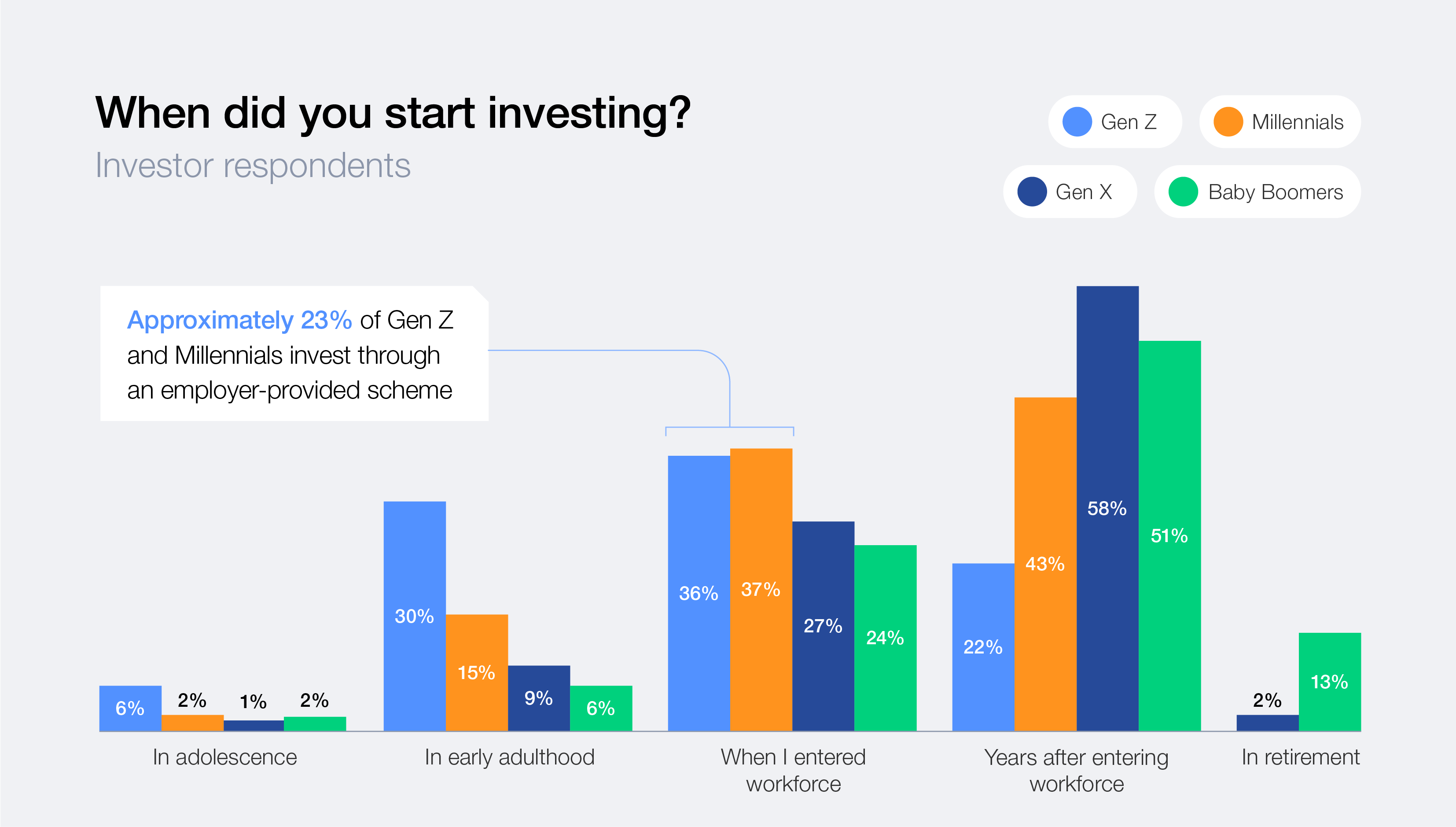

This is a shift we need to pay attention to because younger investors are starting earlier than their older counterparts. According to the report, 45% of Generation Z (Gen Z) and millennials began investing in early adulthood, compared with just 15% of Generation X (Gen X) and baby boomers.

To meet the needs of this growing investor community, we must prioritize user experience and value, both of which can be enhanced through tech-enabled innovations that allow more participants in markets than ever before.

Specifically, the report found that “younger people, individuals from emerging markets, women and other traditionally underserved groups are participating in capital markets at higher rates and are interested in a broader selection of products and more personalized, tech-enabled guidance.”

While they don’t require face-to-face interactions, they still want tools that recognize their needs and wants.

On the other side of the age spectrum, baby boomers and Gen X investors prefer people-first service models. Gen Z and millennials place greater importance on intuitive and tech-enabled wealth management journeys.

Have you read?

Between automation and human touch

For this reason, we intentionally use the term “tech-enabled,” recognizing that there is a broad range of products and services that fall between fully automated and fully human. Within this range, we see the greatest opportunity for innovation and expansion, considering a combination of automation and human expertise.

At Robinhood, we see a particularly important niche where the financial services industry can leverage technology to deliver more inclusive and tailored financial advisory services.

Gen Z is interested in learning and hungry for financial advice.

Many are seeking this knowledge using artificial intelligence (AI) chatbots for financial coaching or advice (40%), compared with only 8% of baby boomers.

Gen Z’s greater trust in AI likely stems from their digital upbringing. This age cohort has been raised on personalized algorithms, voice assistants and instant access to information. Unlike older groups, who may view AI with scepticism, Gen Z sees it as a familiar and efficient tool for navigating complexity.

For them, financial advice doesn’t have to come from a person in a suit – it can come from a dynamic digital interface that's fast, judgment-free and always available.

This shift in expectations presents a challenge and an opportunity. Institutions that adapt can help close the advice gap by meeting Gen Z where they are – online, curious and ready to learn.

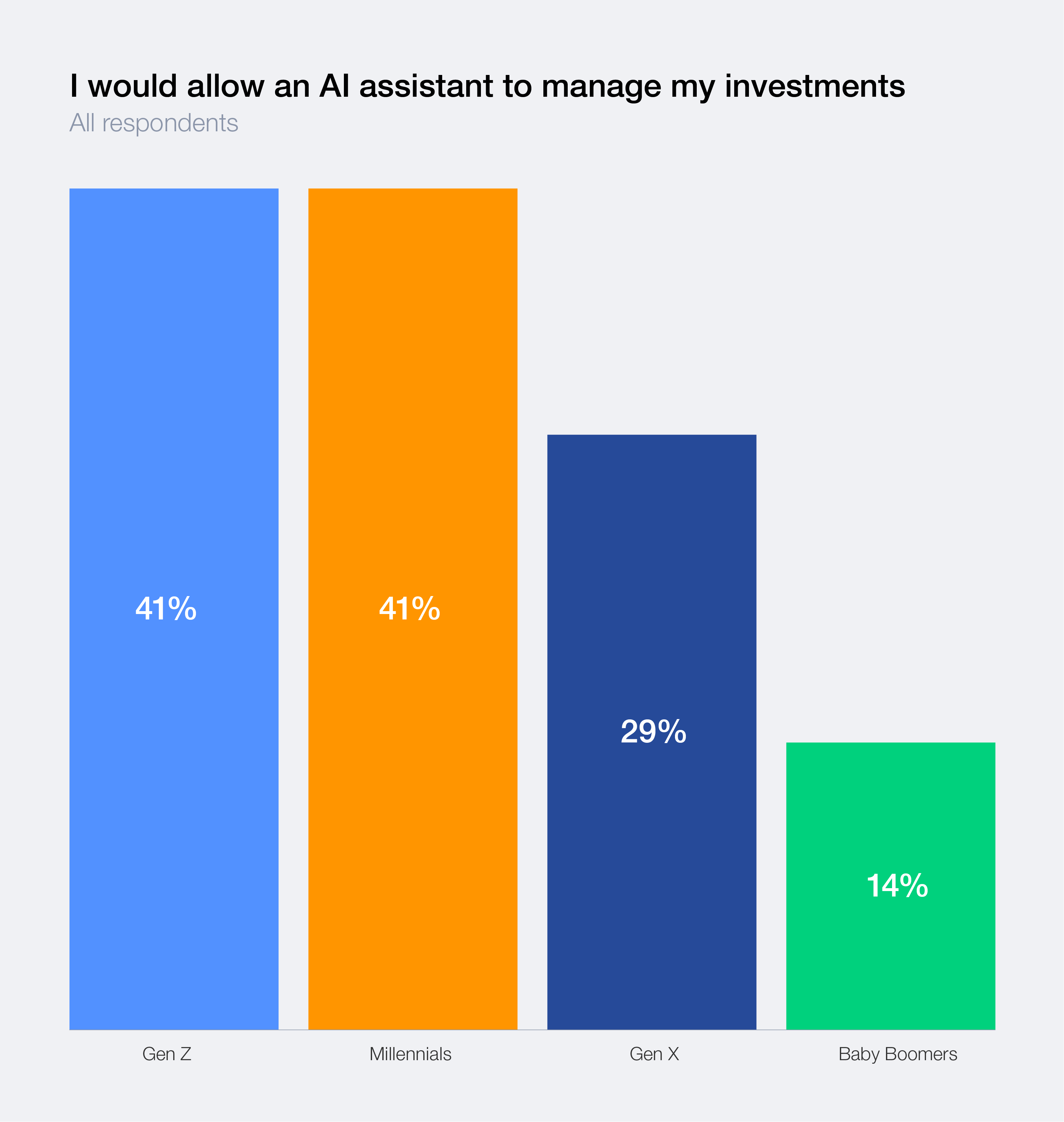

Further, when asked if they would allow an AI assistant to manage investments, Gen Z indicated interest nearly three times greater than baby boomers (40.5% versus 14%). The interest in receiving advice is clear.

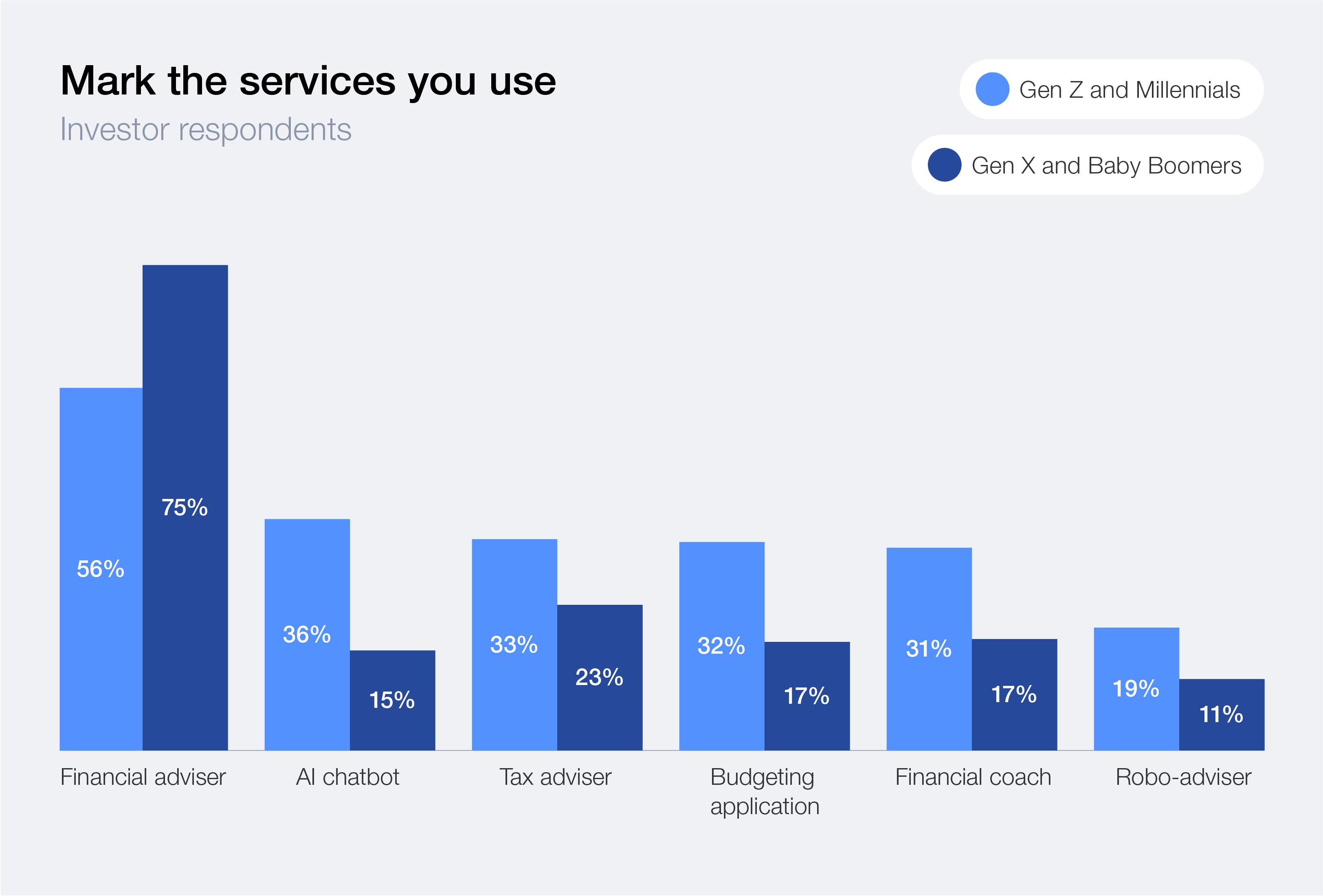

However, when we examine the usage of financial advisors, we see that 82% of baby boomers use them, compared to just 45% of Gen Z respondents.

This data comparing tech-enabled advice with one-to-one human advice highlights two crucial factors: the cost of services rendered and the value of time efficiency.

Hybrid solutions

From all this, we hear a rallying cry: how can we identify opportunities to deliver financial advice that offers the trustworthiness of human expertise with the financial efficiency of tech-enabled products? Many companies, including Robinhood, have heeded that call.

Consider, for example, Endowus.

Endowus is a digital advisor that helps Singaporeans grow their wealth by investing systematically. It determines asset allocation and portfolio construction, customizing investor portfolios. Their minimum account requirement can be a barrier but it is a scalable solution for mass affluent and high-net-worth individuals with different tiers of service in Asia.

At Robinhood, we recently launched Robinhood Strategies, a Securities Exchange Commission-registered investment adviser, to deliver tailored, expert-led, actively managed portfolios and advice to our US clients directly in the app while helping clients understand how and why their money moves so they invest with confidence.

Perhaps what we’re most proud of within Robinhood Strategies is that the team delivers timely insights, providing the “why” behind portfolio changes and updates on broader market moves to keep clients informed.

The “why” is crucial when building trust in technology. The United Kingdom-based nonprofit Fair4All Finance works to improve access to affordable, ethical financial products for underserved communities via tech-enabled tools that explain loan terms, budgeting recommendations and debt repayment options.

These tools don’t just deliver advice; they explain why a particular path is recommended, helping users build financial confidence and avoid predatory alternatives. By embedding transparency and education into digital services, Fair4All Finance delivers a scalable solution to help excluded individuals engage with financial tools they can trust.

Learning by doing

Inherently, high-quality advice is also a form of financial education. As much as the data shows us that individuals want advice, they also want to learn. We found:

- 42% of people “learn by doing” when it comes to investing, the highest ranking response.

- 28% don’t invest because they don’t know how or find it confusing.

- 70% of investors surveyed said they would invest more if they had more opportunities to learn how to invest.

In practice, this data is reinforced. The US nonprofit NextGen Personal Finance (NGFP) provides free personal finance curricula via hands-on simulations, including their investing challenges.

Their instructors consistently report that experiential activities lead to better retention and confidence, and NGPF’s student surveys show that these simulations often spark interest in real investing.

So our guiding question should be: how can we lower barriers to entry to enable folks to learn by doing, within their risk threshold, with the support of an advisor to help them along the way? This way, they can learn about the benefits and risks in real-time. We’re bolstered by the evolving opportunities created to support learning and wealth-building in concert.

With the Great Wealth Transfer, over $100 trillion is expected to shift from older generations to younger ones throughout the next 15 years; younger investors are poised to shape the global financial future. This is a pivotal time to leverage tech-enabled solutions to make investing, advice and education more accessible for those building and inheriting wealth.

By combining automation with human expertise, the financial services industry can provide efficient and affordable services that cater to the diverse and evolving needs of emerging investor groups.

Looking ahead, we have the opportunity to reimagine a financial system that is more inclusive, transparent and empowering. By centring the needs of this new class of investors – those who are more diverse and digitally native – we can build a future where financial well-being is not a privilege but a possibility for all.

The choices we make now can enable shared prosperity for generations to come.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Youth Perspectives

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Ibrahim Alramady

July 1, 2026