3 ways Africa can maximize the value of its critical minerals and finance its future

A worker collects samples for inspection from a pile of copper dust at a mine in Eritrea. Image: Reuters/Thomas Mukoya

- Africa does not sufficiently monetize its abundant critical mineral resources, exacerbating its development financing gap.

- With growing demand for critical minerals for the energy transition, the continent has a key window for transforming its industrial strategies.

- Increasing local processing, addressing the fiscal revenue gap, and building regional integration would help recapture African mineral wealth.

Africa faces a development financing gap of $1.6 trillion, consistently failing to meet its needs across health, education, energy and infrastructure. Traditional responses through foreign aid and debt relief have failed to close this gap, with official development assistance to Africa declining by 9% in 2024 and borrowing costs continuing to rise. But critical mineral assets offer an immediate alternative financing pathway.

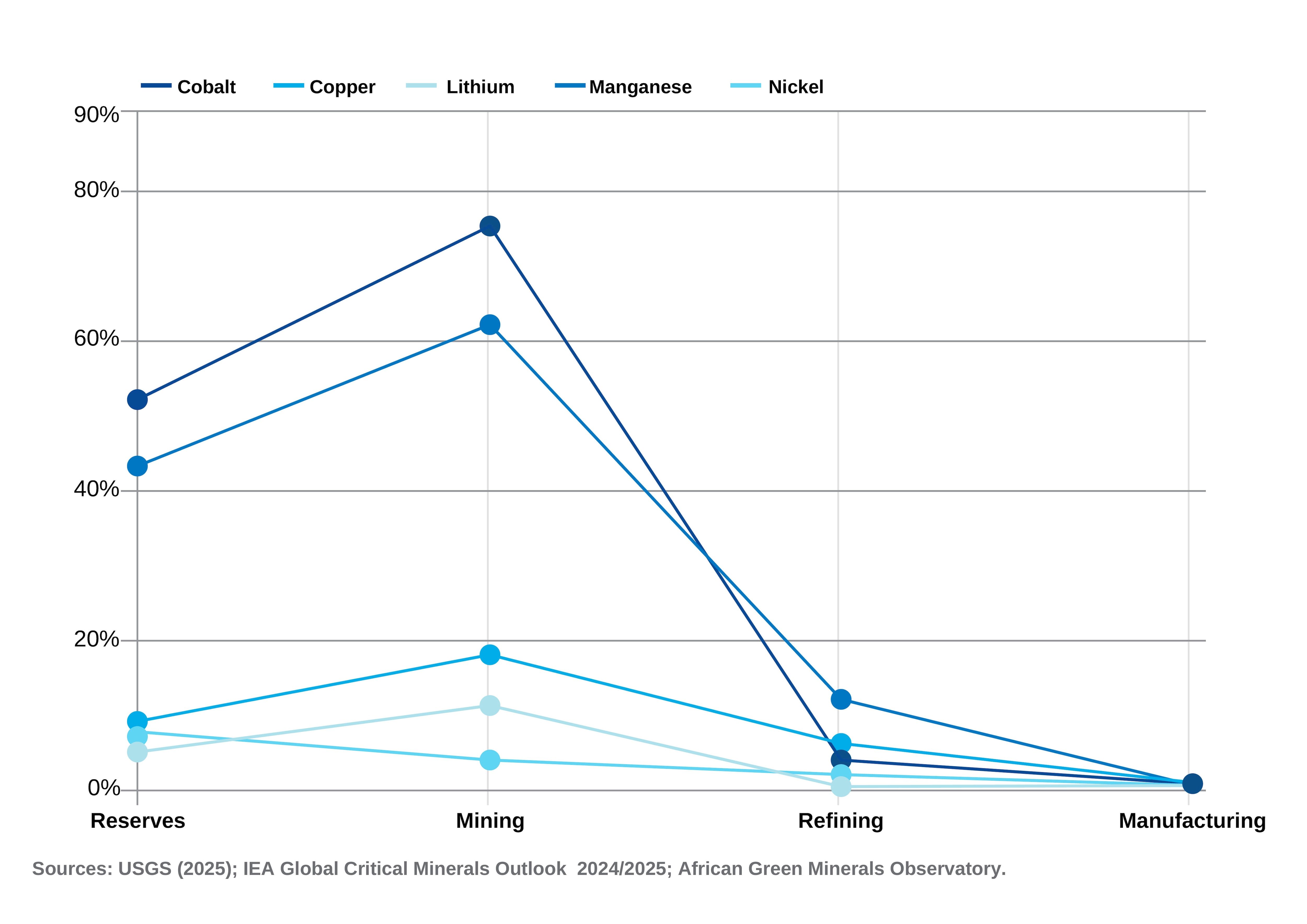

The continent holds an estimated 30% of the world's critical minerals, contributing about 75% of global cobalt production, 62% of manganese, while holding significant deposits of lithium, copper and rare earth elements. As demand driven by the global energy transition keeps rising, revenues from just four key minerals (copper, nickel, cobalt and lithium) are projected to reach $16 trillion over the next 25 years, with sub-Saharan Africa positioned to capture over 10% of that total. Yet African countries currently collect only about 40% of potential revenues from these resources. Three strategies can change this.

1. Increasing local processing and beneficiation

Africa’s critical mineral wealth can directly finance its development by strategically moving up the value chain. Every stage of value addition that happens on African soil, from refining raw ore to producing battery-grade materials, will generate tax revenue, create employment and retain foreign exchange that would otherwise leave with the unprocessed export. For decades, the continent has exported the raw materials of global industrialization while importing finished products at a premium, capturing less than 1% of the total economic value of the green technologies its minerals make possible.

The gap between what Africa mines and what it processes is particularly wide for cobalt: Despite the DRC accounting for two-thirds of global mined cobalt in 2024, nearly all output is exported with minimal processing. The chart below shows this pattern across key minerals, with Africa's share collapsing at every stage beyond extraction.

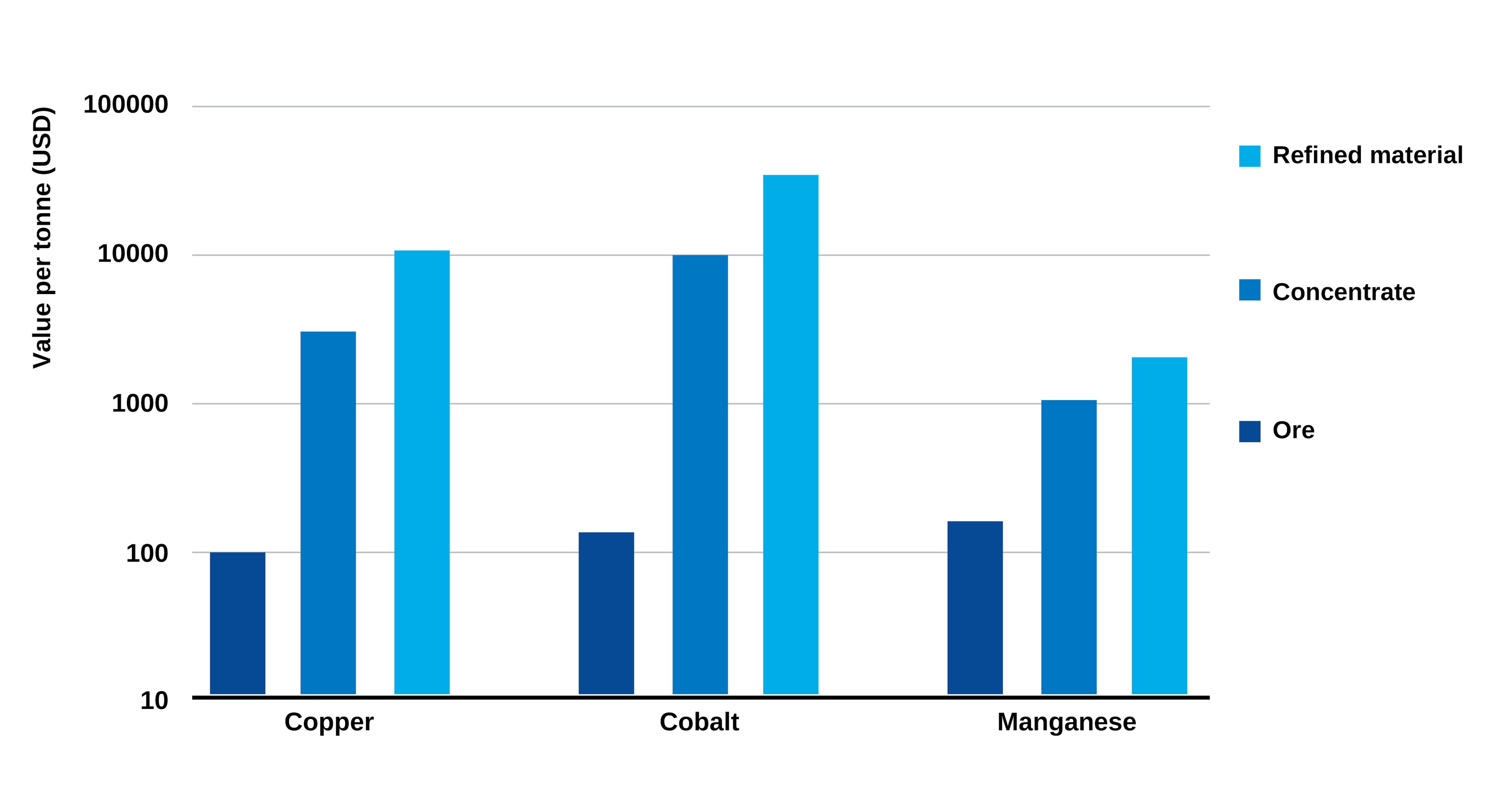

Refining these critical minerals can add a further 15-30% premium at each processing stage; value that currently leaves Africa.

The IEA projects that the total market value of Africa's key refined minerals could rise from roughly $70 billion today to $120 billion by 2040, driven by moving a greater share of production through domestic processing. If done at scale, pursuing beneficiation (the treatment of raw materials) could indeed raise the continent's GDP by 12% and create approximately 2.3 million high-quality industrial jobs.

Therefore, the strategic imperative must be to provide the conditions that make processing investment viable and fiscally productive. This means designing investment frameworks that link capital entry to genuine value addition commitments, rather than allowing processing promises to remain unenforceable aspirations. It means directing finance toward the energy infrastructure and industrial corridors that processing facilities require. And ultimately building the institutional capacity to monitor, enforce and progressively deepen those commitments over time.

2. Closing the fiscal revenue gap

While beneficiation captures the long-term prize, reforming the fiscal architecture of extraction could generate significant development revenue in the near term. Tax incentives have a legitimate role in attracting capital to high-risk projects, but their current prevalence in Africa may be reaching a point of diminishing returns. Between 2014 and 2016, corporate income tax holidays granted to just two firms cost Sierra Leone $131 million, which was roughly equal to the country's entire 2024 budget deficit. In Guinea, mining-related tax expenditures, such as corporate income tax holidays, reduced mineral royalties and import duty exemptions on mining equipment, represented 24.4% of total national tax expenditure in 2019; IMF simulations suggest that modest reforms could generate revenue four times the size of the country's entire agriculture budget.

Thinking further ahead, Africa must rethink its incentive strategy and put greater emphasis on incentivizing value creation rather than extractive presence alone. These could be in the form of performance-linked incentives that are time-bound and tied to outcomes such as local value addition, technology transfer and infrastructure development.

Closing the revenue gap will also mean fixing the revenue leakage problem. Africa loses about $89 billion annually to illicit financial flows, with the extractives sector significantly exposed. The IMF estimates that sub-Saharan Africa loses $450-730 million annually in corporate income tax alone from profit-shifting by multinational mining companies. To address this, African governments must build state capacity for revenue management and close the loopholes that allow transfer pricing abuse (where companies manipulate prices charged between their own subsidiaries across jurisdictions to shift profits away from the country where the mineral is extracted, reducing their tax liability there). Every dollar protected from leakage is a dollar that does not need to be borrowed and can directly flow into the development finance pool Africa urgently needs.

3. Leveraging regional integration

However, both strategies must be supported by regional integration to achieve scale. Africa's mineral endowment is geographically distributed, and no single country holds the full mineral basket required to anchor an integrated clean-energy value chain. This makes regional coordination an economic necessity.

The DRC-Zambia transboundary battery and electric vehicle special economic zone is the most concrete example. Collectively, Zambia and DRC hold 70% of the minerals needed for battery and EV production. A BloombergNEF study confirmed a joint precursor plant is financially viable and building it in the DRC would cost three times less than an equivalent facility in the United States, demonstrating that Africa's processing proposition is commercially competitive.

The AfCFTA creates the architecture to scale this model. By aggregating demand, harmonizing investment standards and enabling shared infrastructure along mineral corridors, the AfCFTA can transform isolated national deposits into a regionally integrated industrial hub. With better coordination, revenues generated at each processing stage will be multiplied across economies.

Africa faces its largest development financing gap at precisely the moment when the global value of its mineral wealth has never been higher. Three forces make this moment particularly critical. The external financing model Africa has depended on for decades is breaking down, but simultaneously the global energy transition has created long-term demand for Africa's minerals that is written into the industrial strategies of major economies. Hence, policy decisions made now will determine the architecture of the clean energy economy for decades, with first movers capturing the dividends. But these conditions will not persist indefinitely, hence the need for urgency.

Increased local processing will raise revenues for Africa by capturing more value; fiscal reform will unlock the revenues already owed from ongoing extraction; and regional integration scales both by creating the market depth and investment attractiveness that individual countries cannot generate alone. On this path, Africa will move from a development financing model anchored in external dependency toward one built on the productive use of its resources.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Africa

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Energy TransitionSee all

Sofia Balestrin

April 2, 2026