Southeast Asia may be a distinct region but its risks affect each country differently

Deep dive

Economic pressure, geopolitical rivalry and technological disruption affect countries in Southeast Asia differently Image: Unsplash/Joshua Kettle

Joseph Liow

Dean and Wang Gungwu Professor in East Asian Affairs, Lee Kuan Yew School of Public Policy, National University of Singapore- Economic pressure, geopolitical rivalry and technological disruption are affecting the region unevenly, reflecting big differences in economic structure, fiscal space and demographic trends.

- Tariffs, supply chain shifts and competing global partnerships are forcing Southeast Asian economies to balance short-term stability with long-term strategic autonomy.

- While governments and firms are investing in AI infrastructure, uneven adoption, energy constraints and workforce disruption could leave smaller firms and vulnerable workers behind.

Imagine 10 very different houses on the same street – some new, some old, some developing while others are becoming unstable; the same neighbourhood but very different grievances.

That’s very much the narrative for Southeast Asia.

The region spans 10 economies, from Singapore, one of the world's wealthiest, to Myanmar, one of its poorest, with their gross domestic product per capita differing by around $98,000. Yet, in conversations about trade, investment and risk, “Southeast Asia” is often treated as a single place with a single story.

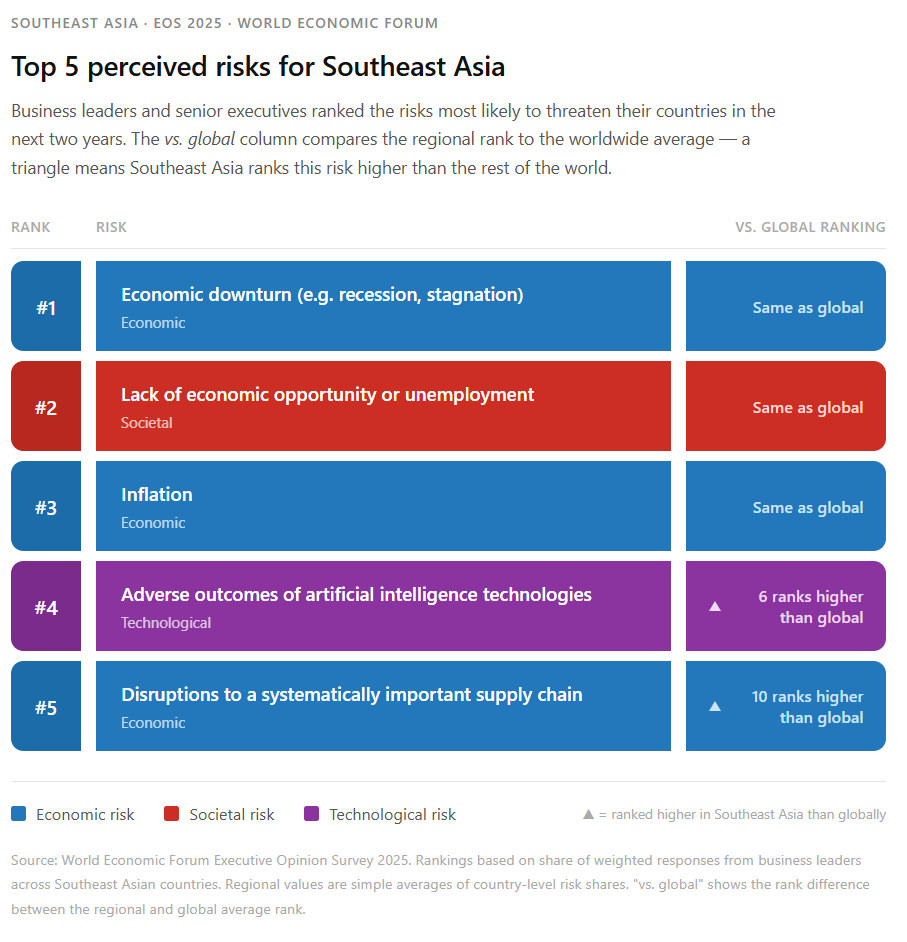

This shortcut misses much about the region and according to the World Economic Forum’s Executive Opinion Survey, capturing how business leaders perceive the risks around them, the divergence is clear.

There is growth but it’s not reaching everyone

Economic growth is a case in point. In the survey, the top three perceived risks in the region are economic downturn, lack of jobs or economic opportunity and inflation, reflecting a shared anxiety about how individuals will experience growth. The signs of stress are already visible.

In Thailand, growth forecasts have been revised downward due to trade uncertainty and high household debt. Meanwhile, Brunei is still trying to reduce its reliance on oil and gas, and Lao PDR faces serious debt pressures that limit room to manoeuvre.

Meanwhile, ageing demographics in Malaysia and Viet Nam are outpacing economic development, a challenge requiring different investments in productivity and skills.

Even in Singapore, cost-of-living pressures dominate policy conversations, with households feeling squeezed despite the country’s wealth.

The three top risks reflect something structural: economies are growing on paper but have not yet conquered stable inflation management, good jobs and targeted support for the most vulnerable – factors that turn GDP into genuine security.

Isolating economic downturn, unemployment and inflation as individual policies means missing the connective tissue between them.

When superpowers compete, smaller economies feel squeezed

Southeast Asian economies also find themselves at the sharp end of a more global rivalry. As shown by the survey, respondents ranked geoeconomic confrontation – including tariffs, sanctions and investment restrictions – eighth regionally, compared to 14th globally.

That six-position gap signals that leaders in Southeast Asia perceive their operating environment as significantly more geopolitically exposed.

The numbers demonstrate why.

Last year, US tariffs would have imposed rates of 46% on Vietnamese exports and 36% on Thai exports, potentially reshaping entire supply chains overnight. There was also pressure to tighten rules of origin to prevent Chinese-made goods from being rerouted through Southeast Asia to avoid tariffs.

However, as most Association of Southeast Asian Nations (ASEAN) economies trade more with China than with the United States, cutting ties was a non-starter. To navigate this new conundrum, Malaysia convened a special summit with ASEAN, the Gulf states and China, during which Indonesia secured a lower tariff rate for key commodity exports during the 90-day tariff pause.

Vietnam and the European Union also deepened their economic partnership, an already burgeoning relationship that accelerated during this period.

Then, in February 2026, the US Supreme Court struck down the tariff regime.

Overnight, Cambodia, Malaysia and Indonesia, which had already signed bilateral agreements accepting 19% tariffs, found themselves in legal limbo as the US administration moved to reconstitute the tariffs under different legal authority, reintroducing uncertainty.

Beyond a single tariff rate, the deeper issue is that pressured trade arrangements for short-term stability can entail long-term obligations that erode a country’s negotiating leverage.

In addition, supply chain decisions made by multinationals today will need to withstand a geopolitical environment that has already proven capable of reversing direction overnight.

AI boom in the region brings opportunity (and widening fault lines)

Southeast Asian executives rank the risks from artificial intelligence (AI) adversely at fourth regionally, compared to 10th globally. There is also relatively higher concern about online harms and the risks posed by frontier technologies more broadly.

Investment in AI-enabled growth is underway across the region. For example, Microsoft announced major cloud and AI investment programmes in Indonesia and Malaysia.

Qualcomm opened an AI research and development centre in Viet Nam. Singapore’s Green Data Centre Roadmap treats computing capacity as strategic national infrastructure, just as earlier generations treated highways or ports.

However, data centres are enormously power-hungry and the region’s electricity grid is still overwhelmingly fossil-fuel-based. Data centre electricity consumption across six major ASEAN economies is projected to increase almost eightfold between 2024 and 2030.

As a result, Malaysia alone could see its data centre emissions rise sevenfold by 2030, while the Philippines faces a potential 14-fold increase and Indonesia a fourfold increase. Malaysian authorities rejected nearly 30% of data centre proposals in early 2025 for failing to demonstrate responsible energy use.

The benefits of AI use are also not evenly spread. Nearly 46% of regional firms have begun scaling AI but among small and medium-sized enterprises (SMEs), which employ the majority of the region’s workers, AI adoption stands at around 15%, even in Singapore, the region's most digitally advanced economy.

If large companies capture most of the productivity gains while workers across the labour market face job losses, AI could increase inequality, especially when unemployment ranks second among perceived risks in the survey.

Around 164 million workers in the region could be affected by AI, with women and younger workers disproportionately impacted. The Philippines’ AI Roadmap 2.0 explicitly frames AI adoption around its large outsourcing and services sector, given the high and visible stakes for employment transitions.

Online harms are also prompting regulatory action: Malaysia has introduced a licensing framework for major social media platforms, Thailand has escalated anti-fraud measures and the Philippines has continued strengthening laws protecting children online.

Regional efforts are also taking shape, such as the ASEAN Digital Economy and AI Learning (DEAL) project to build shared AI skills and coordinate data and policy.

While these are all important steps, they work best in coordination: when energy and digital strategies are addressed as the same policy question and when governance frameworks are built across borders.

The risks are all arriving at once

Southeast Asia’s challenge is not that it faces many risks but that these risks now converge and reinforce one another.

”None of the mentioned risks is operating in silos.

Geoeconomic competition shapes who can afford to build AI capacity, risking a widening technology gap between the region’s richer and poorer economies.

Supply chain restructuring is accelerating the digitalization of manufacturing, creating new cybersecurity and governance exposures where regulation has yet to reach.

Inflation and unemployment pressures are themselves partly a product of external trade shocks.

“Southeast Asia’s challenge is not that it faces many risks but that these risks now converge and reinforce one another,” said Vijay Eswaran, the executive chairman at QI Group.

“Economic pressure, geoeconomic fragmentation and technological disruption are testing the region’s resilience at the same time. The response must therefore be more integrated, more adaptive and grounded in long-term values rather than short-term reaction.”

The domestic context adds its own pressures as governments manage electoral cycles, leadership transitions and contested policy directions, precisely when the multi-domain risk environment demands the most sustained attention.

In economies where fiscal space is also narrowing, including Thailand, the ability to absorb external shocks without domestic political costs is further reduced.

ASEAN’s consensus-based model of cooperation has historically been well-suited to slow-moving, long-horizon challenges. The current risk environment is neither slow-moving nor neatly contained within single policy domains.

Closing that gap requires deliberate action from multiple actors simultaneously: governments investing in connecting policy and the private sector, particularly multinationals, reshaping the region’s supply chains and digital infrastructure, proactively building shared standards, capacity and platforms.

No single government can build that architecture alone; together, they must act before the risk environment outpaces their ability to act.

Additional insights and contributions by Grace Atkinson, Mark Elsner and Joo-Ok Lee.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Global RisksSee all

Matt Strahan and Daniel Murphy

April 9, 2026