Global economic outlook darkens – here's how chief economists view the year ahead

A supply shock originating in the Strait of Hormuz has dramatically altered the outlook among chief economists. Image: via REUTERS

- The global economic outlook has darkened, according to the latest Chief Economists’ Outlook.

- The conflict in the Middle East and closure of the Strait of Hormuz have disrupted vital energy, food and fertilizer flows, threatening access and growth.

- Global inflation is expected to rise as volatility increases.

The World Economic Forum’s May 2026 Chief Economists’ Outlook finds that 89% of the chief economists surveyed expect global growth to weaken over the next 12 months, and more than one in five expect it to weaken significantly.

The conflict in the Middle East and closure of the Strait of Hormuz have induced a shock now shaping global prospects, as supply shortages of fuel, fertilizer and other essentials are rippling through economies.

Inflation has re-emerged as the dominant near-term risk. 94% of the chief economists agree or strongly agree that global inflation will rise in the next 12 months, driven mainly by rising energy and food prices.

Yet the outlook is not one of imminent global recession. 58% of the respondents disagree or strongly disagree that a global recession will occur within the next year. Instead, the concern is a weaker, more volatile economy with limited short-term gains in resilience; six in 10 respondents do not expect the global economy to become more resilient.

At the same time, 79% expect volatility in private debt markets to increase over the next 12 months, while 74% say the same for public debt markets as do 68% for global stock markets. The Middle East conflict may only further increase volatility.

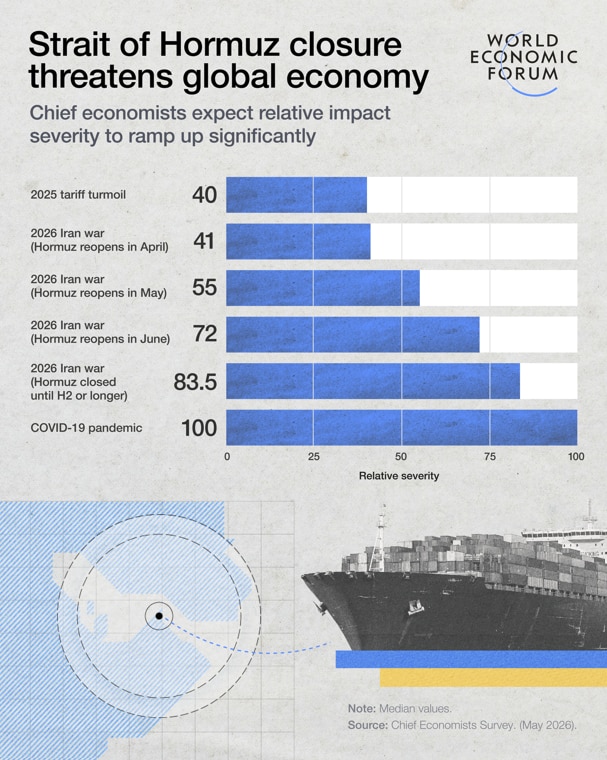

A shock through the strait

The closure of the Strait of Hormuz turned a regional conflict into a global shock. The longer it remains closed, the more severe the impact is going to be.

Chief economists already see the current disruption as more severe than that of the 2025 tariff turmoil, and anticipate that impacts could quickly ramp up. Should the strait remain closed for much longer, disruption is expected to approach levels last seen during the COVID-19 pandemic.

The industries most exposed to the conflict are energy and materials. 58% of the chief economists describe disruption in these sectors as very high.

Supply chain and transport services follows closely, with 76% of respondents rating disruption there as high or very high. Leisure and travel, defence, agriculture, forestry and fishing, and manufacturing are also being affected, though in different ways; some through direct price shocks, others through rerouting, input shortages, and changing risk perceptions.

Regional outlook remains divergent

The shock is expected to hit different regions in different ways.

South-East Asia is expected to bear the brunt, with 62% of the chief economists anticipating significantly higher energy prices there over the next 12 months. The equivalent figure for Europe is 45% expecting significantly higher prices, for both Japan and India it’s 41%, and for Sub-Saharan Africa it’s 36%.

The food shock is likely to arrive more gradually, but it may be severe if fertilizer shortages persist. More than four in five chief economists expect food prices to increase or increase significantly across all regions, with the Middle East and North Africa particularly exposed.

Have you read?

India stands out as the most upbeat growth story in the survey. Slightly more than half of the chief economists, or 52%, expect strong or very strong growth there over the next 12 months.

South-East Asia should also remain relatively resilient, with 48% expecting moderate growth there and 21% expecting strong or very strong growth. However, both of these regional economies are vulnerable to higher energy and food import costs. India in particular faces rising inflation expectations, with 61% of respondents projecting high or very high inflation there in the year ahead.

The US and China each remain relatively resilient, but for different reasons. In the US, 74% of the chief economists expect moderate growth, supported by AI investment, consumption, and government spending, though more than half expect high or very high inflation there. China’s outlook has improved, with 77% expecting moderate or stronger growth there, up from 71% in the previous edition of the outlook published in January 2026, helped by strong export performance and high-tech manufacturing.

The outlook for Europe, by contrast, has deteriorated. 65% of the respondents expect weak or very weak growth in the region, while half expect high or very high inflation as energy shocks raise stagflation risks.

The Middle East and North Africa region faces the sharpest projected deterioration in the outlook. 88% of the chief economists expect weak or very weak growth there – a direct reflection of the conflict, higher regional food exposure, and weaker employment prospects.

Sub-Saharan Africa and Latin America and the Caribbean are each meanwhile seen as more stable, though inflation in these regions is a primary concern. In Sub-Saharan Africa, 67% of respondents expect high or very high inflation, while in Latin America and the Caribbean 51% expect the same amid modest growth and constrained financing conditions.

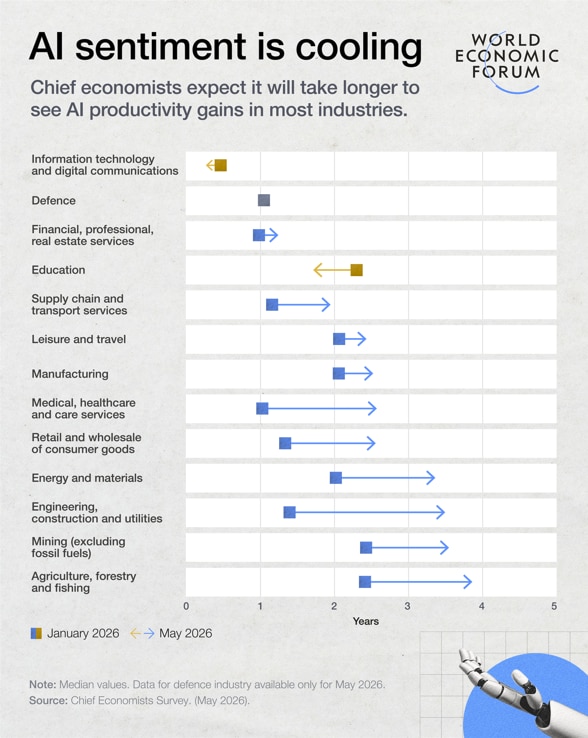

A cooling view on AI-related productivity

AI remains the main source of optimism among the chief economists, but expectations are moderating.

More than nine in 10 expect AI adoption to increase in the next 12 months, and imminent productivity gains are expected in the information technology and digital communications sectors.

However, sentiment has cooled across most industries compared with January 2026.

Respondents now expect broad-based, AI-related productivity gains to take longer to materialize, especially in industries where firms faces higher obstacles when attempting to integrate AI into existing structures and processes.

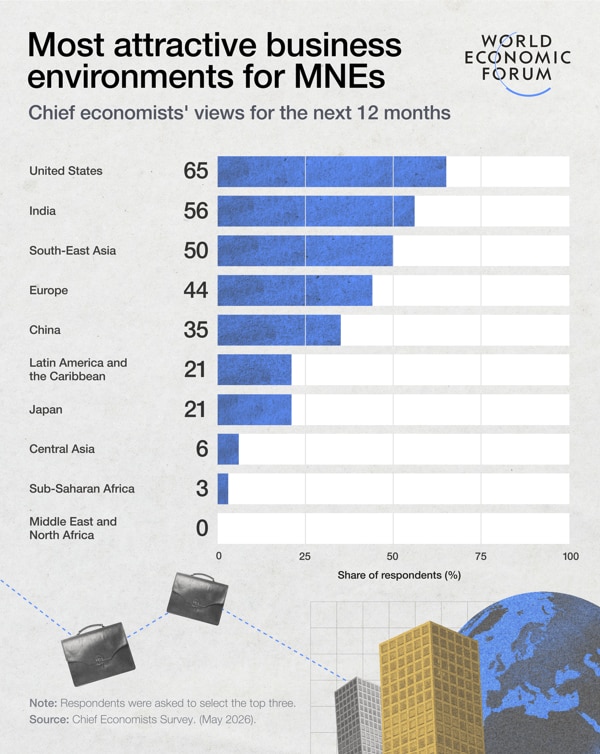

A new global business map

Multinational companies are reassessing where to invest and operate.

According to the chief economists, the US, India and South-East Asia are now viewed as the most attractive business environments, with 65%, 56% and 50% of respondents, respectively, placing them in their top three.

That ranking suggests that scale, strategic flexibility and supply-chain positioning matter more than headline growth alone. The US retains deep capital markets and demand, India offers scale and growth potential, while South-East Asia is seen benefiting from increased foreign investment and supply-chain diversification.

Europe remains competitive, despite growth that’s constrained by regulatory unpredictability and sluggish consumer demand. And China continues to offer scale and technological depth, though intense competition and relatively thin margins temper its appeal to multinational companies.

Sub-Saharan Africa and the Middle East and North Africa are each seen as less attractive now, due to geopolitical risk and infrastructure constraints.

The broader message delivered by chief economists is clear: the global economy is not simply slowing, it is being reordered by conflict, supply-chain stress, energy insecurity, and a more uneven path to technological transformation.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Marushia Gislén and Emmy Van Enk

July 8, 2026