Why measuring material emissions is key to cutting carbon in the built environment

Singapore is leading the way on decarbonizing the built environment. Image: Kirill Petropavlov/Unsplash

Daniel Boero Vargas

Lead, Industrial Decarbonization Innovation, Supply and Concrete, World Economic Forum- For the first time, Singapore has a market-wide benchmark for the embodied carbon of concrete, covering about 68% of the country’s market.

- Lower-carbon materials are generally available and commercially viable, but the barrier lies in the choices made during specification and procurement.

- Because Singapore imports most of its construction materials, its purchasing decisions can drive cleaner production practices across the region.

For decades, efforts to reduce emissions in the built environment have focused on operational carbon, which covers emissions stemming from how buildings are powered, cooled and used.

However, the next frontier lies in the materials that make up our urban environments. The built environment accounts for nearly 40% of global emissions, with approximately 12% linked to materials and construction.

Concrete alone contributes about 8% of global carbon dioxide (CO₂) emissions – more than other heavy-emitting sectors such as aviation and shipping.

Unlike operational emissions, which can be gradually reduced as energy grids decarbonize, the carbon locked into building materials is determined at the procurement stage, when materials are specified.

This raises a critical question: how do we decarbonize building materials at scale, while still meeting development needs?

A systems approach to materials decarbonization

Singapore’s experience of decarbonizing the built environment offers a compelling answer: rather than a single technology, the solution lies in aligning entire ecosystems.

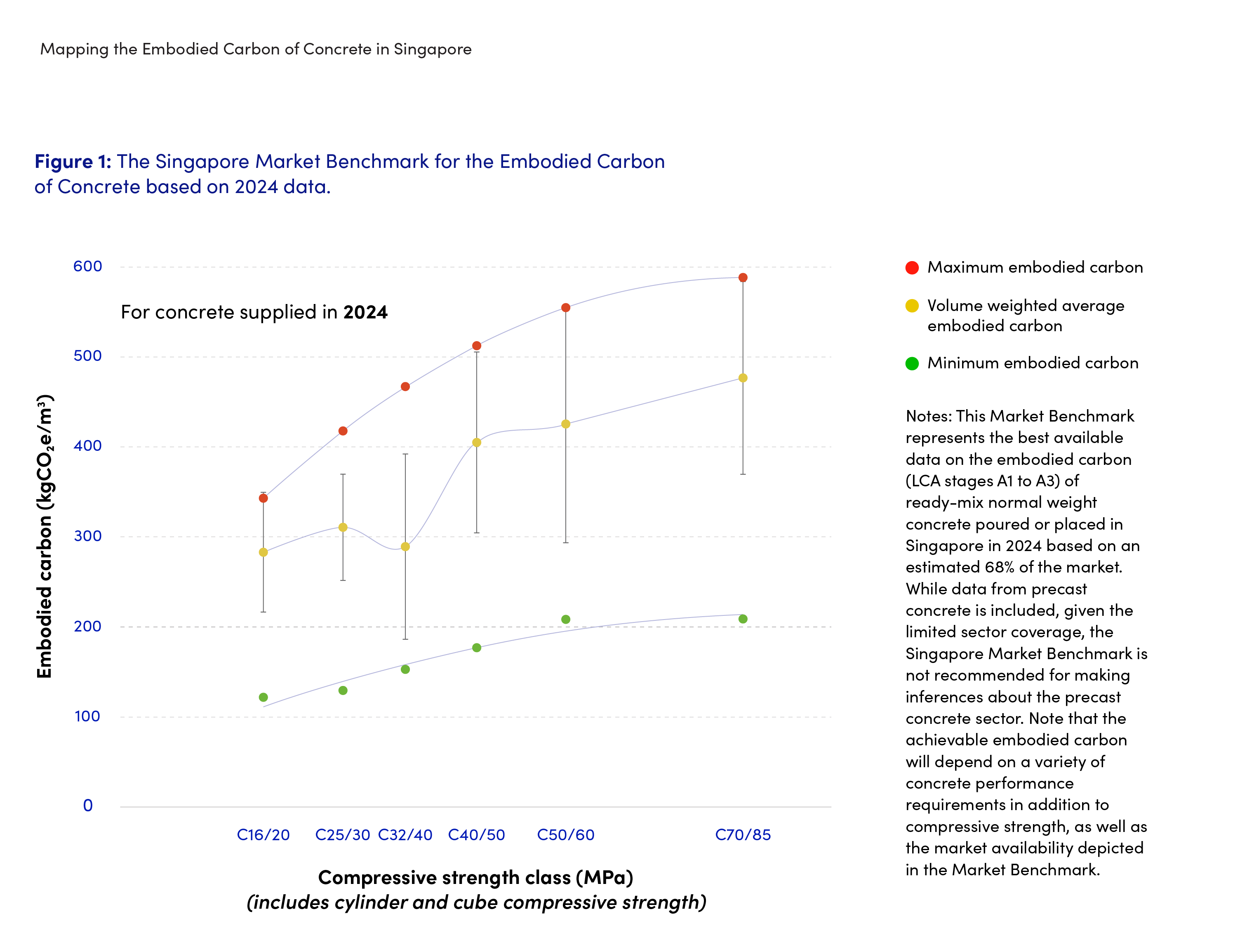

Applying this logic to materials, a multi-stakeholder collaboration has developed one of the first global market benchmarks for the embodied carbon of concrete. The benchmark provides a snapshot of carbon intensity across the national concrete market, covering 68% of supply, and was launched in February 2026 at a joint event with the World Economic Forum's First Movers Coalition.

The collaboration’s central finding shows that lower-carbon concrete is already commercially available, with a near-term opportunity to shift towards lower-carbon solutions.

In Singapore, concrete’s upstream emissions are estimated at 3.7 million tonnes of CO₂e – around 6% of national emissions –, yet most occur outside its borders, in imported materials and regional supply chains. Demand is driven locally, while emissions occur globally.

Bridging that gap requires coordination across the entire value chain.

Shifting from ambition to implementation on decarbonization

The benchmark for concrete's embodied carbon represents a shift from ambition to implementation. It reveals current performance and the full range between minimum, average and maximum values.

This variation shows that lower-carbon solutions are already available, but adoption remains uneven across the four stakeholder groups and the following actions are key to drive decarbonization in the built environment.

1. Industry leadership: turning demand into a signal

Developers, designers and contractors define material specifications and procurement criteria, making them the primary drivers of change.

In this context, developers and financiers engaged suppliers and the wider construction ecosystem to encourage participation and contribution of data to establish the benchmark. Banks and financial institutions have supported the benchmark, which can provide a stronger business case for them to invest in low-carbon solutions.

Large buyers are using purchasing power to shift markets: Microsoft is piloting concrete mixes that cut embodied carbon by over 50% across its data centre buildout, backed by its $1 billion Climate Innovation Fund.

Demand-driven initiatives for low-carbon materials, such as the First Movers Coalition and the Climate Group’s ConcreteZero initiative, aggregate demand for low-carbon concrete into credible signals to help build the business case for scaling low-carbon supply, thereby making such projects financeable. These initiatives ultimately seek to create a global market for lower-carbon concrete.

2. Global coordination: scaling beyond individual markets

The benchmark was developed by CapitaLand and ConcreteZero. ConcreteZero members, spanning developers, contractors and asset managers across multiple markets, have moved from data transparency to collective implementation commitments, demonstrating demand-side coordination at scale.

This approach has precedent: the UK's Low Carbon Concrete Group has published an annual market benchmark since 2022, which now covers over half of the nation's ready-mixed concrete production.

Singapore's benchmark applies the same logic to a market with its distinct characteristics: import dependency, tropical durability demands, and a unique mix of projects under development.

3. Certification and market infrastructure: translating data into action

A key barrier is the lack of consistent environmental data and common definitions of “low-carbon” materials, which limits comparability and increases the risk of misaligned claims.

The Singapore Green Building Council (SGBC) addresses this through its green product certification framework, translating life-cycle assessment data into clear performance tiers, giving buyers a structured way to differentiate products and integrate embodied carbon into procurement decisions.

Market benchmarks are most effective when used alongside certification systems – including the Global Cement & Concrete Association's global rating system for concrete – enabling stakeholders to move from static labels to dynamic, data-driven decision-making.

4. Academia and technical experts: bridging innovation and implementation

Academic institutions like the National University of Singapore (NUS) are critical partners in testing and validating lower-carbon solutions, as demonstrated by NUS's collaboration with Soilbuild Group Holdings, which upcycled marine clay waste from excavation work into durable, low-carbon green cement for use in Redlion2, Singapore first energy-positive logistics hub by DSV.

The result was a rare trifecta: reduced embodied carbon, lower import dependency and a practical solution to waste disposal. Singapore is now recognized as a global leader in circular construction.

A blueprint for materials innovation beyond concrete

The benchmark's implications extend beyond concrete. In Singapore, the SGBC and the Building and Construction Authority have supported the activation of a Low-Carbon Construction Community of Practice, with a similar model emerging in Vietnam through the Urban Land Institute (ULI) Decarbonization & Resiliency Product Council (DRPC).

At project level, The Canopy at Geneo, Singapore Science Park, takes this thinking further. By using mass engineered timber as its primary structure, the development cuts embodied carbon by an estimated 80% compared to steel and over 60% compared to reinforced concrete. Its climate-responsive design, which prioritizes natural ventilation, is expected to cut energy consumption by over 60%.

Moving forward, the question is not whether lower-carbon building materials exist but whether the systems that govern how infrastructure is built – the specifications, procurement frameworks, financial incentives and certification schemes – enable their demand and deployment alongside necessary urban development.

Singapore's benchmark on decarbonization of concrete is an early answer. Now, the harder work starts on making it the norm.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

SDG 09: Industry, Innovation and Infrastructure

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Built Environment and InfrastructureSee all

David Elliott

July 31, 2026