How Sub-Saharan Africa can convert its resource wealth into jobs and shared prosperity

Deep dive

To unlock access to growth for people in Sub-Saharan Africa, challenges must be addressed through integrated solutions Image: Unsplash/Ngozi Ejionueme

Rita Babihuga-Nsanze

Chief Economist; Director of Research and Strategy, Africa Finance Corporation - AFC- Despite strong demographic, resource and investment fundamentals, economic growth is generating too few formal jobs.

- Business leaders identify inadequate public services, energy, water, healthcare and education as major risks because they directly affect productivity, competitiveness and investment.

- Challenges such as employment, infrastructure deficits, fiscal constraints and external vulnerabilities in Sub-Saharan Africa are interconnected and require integrated solutions.

Something isn’t adding up in Sub-Saharan Africa. The continent holds resources the world urgently wants. Its population is young and growing. Investment has been flowing in. And yet, the question business leaders keep returning to is the same: why isn’t more of this translating into opportunity for people on the ground?

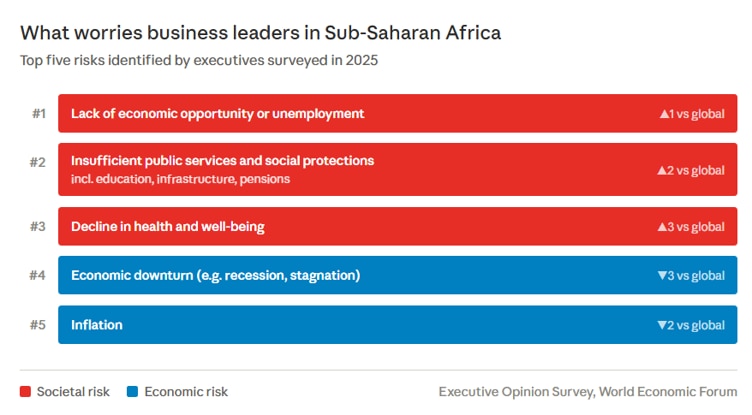

The World Economic Forum’s Executive Opinion Survey captures this clearly. Leaders in Sub-Saharan Africa rank lack of economic opportunity as their top concern for the next two years, more so than in any other region. That consensus is worth taking seriously.

Closing the gap between growth and jobs

Walk through the commercial districts of Nairobi, Lagos or Accra and the energy is hard to miss. Businesses are opening, capital is moving and cities are expanding. But step back and look at the data and a quieter story emerges.

Every additional point of economic growth in the region produces only a tiny 0.04 percentage point rise in wage employment. For the young person entering the workforce – equating to millions annually in Sub-Saharan Africa – that gap between headline growth and lived experience is the defining reality.

Part of the reason is that too little of what Africa produces gets processed or manufactured locally. Take mining, for example. The continent sits on an estimated $8.6 trillion in undeveloped mineral assets, according to the Compendium of Strategic Minerals. Yet fewer than 5% of those critical minerals are refined or processed on the continent.

The ore leaves. The smelters, factories and many skilled jobs and tax revenues are generated elsewhere.

What is true for mining is also applicable across sectors: the constraint is the weak link between production, infrastructure and markets at scale.

Closing the gap requires factories, roads, power systems and crucially, stable conditions for businesses to commit to long-term investment. Conflict and political fragmentation deter exactly the kind of patient capital that industrial development needs.

In practice, what appear as macroeconomic or security risks are often experienced more directly, through higher cost of capital, currency volatility, energy and logistics bottlenecks and delays to project execution.

Basic services must improve to ripple out

According to the Executive Opinion Survey, private-sector leaders rank insufficient public services, including schools, hospitals, electricity and water, as their second-biggest concern, well above the global average. Decline in health and well-being comes in third.

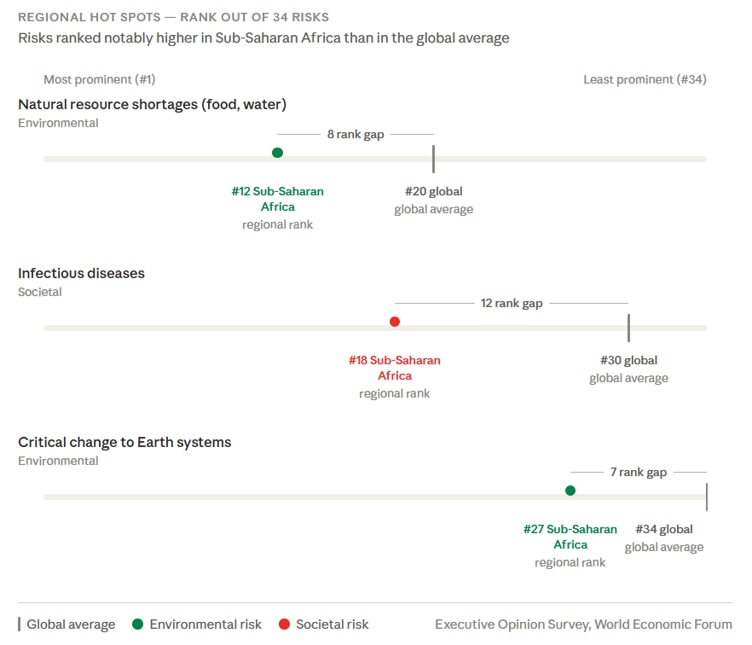

The regional hotspot data shows why these concerns matter beyond public service delivery. Infectious diseases rank much higher in Sub-Saharan Africa than globally, while natural resource shortages, including food and water, also stand out as a stronger regional concern.

These pressures quickly spill over into the economy: infectious diseases affect labour productivity and business continuity, while food and water shortages raise costs for households, firms and public budgets.

Together, these risks point to deeper weaknesses in infrastructure and productive capacity. Reliable power, functioning logistics and connected markets are what make both social and economic systems work.

What makes this moment harder is that outside support is contracting just when it’s needed most. Aid from wealthy countries to Sub-Saharan Africa is estimated to have fallen by up to 28% in 2025 alone, while demands on public systems continue to rise.

The risks leaders see less clearly may be instrumental

Something isn’t adding up in Sub-Saharan Africa. The continent holds resources the world urgently wants. Its population is young and growing. Investment has been flowing in. And yet, the question business leaders keep returning to is the same: why isn’t more of this translating into opportunity for people on the ground?

The World Economic Forum’s Executive Opinion Survey captures this clearly. Leaders in Sub-Saharan Africa rank lack of economic opportunity as their top concern for the next two years, more so than in any other region. That consensus is worth taking seriously.

Yet, geopolitical risks increasingly shape the economic landscape through trade access, financing conditions and supply-chain positioning. They affect the cost of capital, the reliability of trade routes and the bargaining power countries have over where value is created.

Those terms shape whether trade builds local industry or deepens dependence on raw-material exports.

Trade between major global economies and Africa continues to grow but often in ways that reinforce structural imbalances. Africa remains heavily exposed to commodity dependence, external markets and weak infrastructure, with much of its trade in intermediate goods still concentrated in raw materials rather than higher-value industrial production.

Understanding that challenges are interconnected

It would be convenient if each of these challenges could be addressed on its own timeline, in its own silo but that is not the case.

The shortage of good jobs is partly a consequence of weak infrastructure. This, in turn, is harder to fix when financing is constrained. The room governments have to respond shrinks further when external pressures mount.

The evidence points to a system under strain: infrastructure, capital and markets are not yet aligned at scale.

That also means the opportunity lies in better connectivity. According to the Africa Finance Corporation’s (AFC’s) State of Africa’s Infrastructure Report, Africa holds more than $4 trillion in domestic capital, much of it still underutilized in long-term infrastructure and industrial investment.

The task now is to build bankable projects that can put that available capital to work at scale.

A more integrated African market, where countries trade more with one another and less exclusively with the outside world, would reduce vulnerability and increase resilience. Infrastructure corridors, cross-border power systems, and regional industrial platforms offer a practical pathway to achieve this by linking resources to demand and enabling value addition at scale.

The potential is genuinely there. So are the obstacles. Seen in this light, the Executive Opinion Survey findings can help identify where investment, coordination and execution can have the greatest impact and unlock the most value.

The challenge is ultimately about connecting Africa’s resources, demand and capital at the scale needed to create jobs, build resilience and retain more value locally.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

John Letzing

July 31, 2026