The 'fragile real': Why real returns matter more than market averages in retirement planning

One percentage point can significant alter the trajectory of someone's retirement plan Image: Unsplash+/Getty Images

- Retirees should focus less on long-term average investment returns and more on the actual returns they experience after inflation.

- A seemingly minor change in real returns of even one percentage point can dramatically alter the sustainability of a retirement portfolio.

- Poor investment returns early in retirement can be especially damaging because withdrawals continue while the portfolio is down, leaving less capital available to recover later.

Everybody ages and when retirement comes closer into view, people start thinking seriously about their options once they are no longer able to work – pensions, investments and then importantly, when and what to withdraw from them.

This question could be pertinent to an increasing number globally as we enter a general demographic shift, with the number of people aged 60 or older doubling to 2.1 billion by 2050.

The overall picture for global retirement assets seems to have expanded as well, reaching almost $70 trillion in 2025, representing a nearly 10% year-on-year increase. Despite this, 46% of individuals lack long-term financial plans and 38% feel their retirement security has become more fantasy than reality.

Even with retirement assets in place, much of the discussion about withdrawal strategies focuses on the proportion retirees should withdraw each year without exhausting their savings and how that proportion holds up across different economic and demographic conditions.

However, a more illuminating question could be what are the key forces that drive the behaviour of such strategies over time? One of the most important, and often less visible, aspects of its answer is the return experienced during a person’s retirement.

Long-term averages do not account for uncertainty

Investment discussions often focus on expected returns or long-term averages. These are useful for setting expectations but they do not always reflect what individuals actually experience in retirement.

In practice, outcomes are shaped by what returns look like after inflation, market conditions, asset allocation, and the timing of investment gains and losses over the course of retirement. As a result, the return ultimately experienced by retirees may differ meaningfully from long-term market averages.

What matters, therefore, is not simply the return generated by markets but the return that is actually realized in practice – the real return available to support retirement spending.

Realized real returns are inherently uncertain. In many cases, they can also be more limited than what long-term averages might suggest. This is where fragility begins to emerge.

To examine this in more depth, it is helpful to consider how a commonly used withdrawal framework behaves under different return environments.

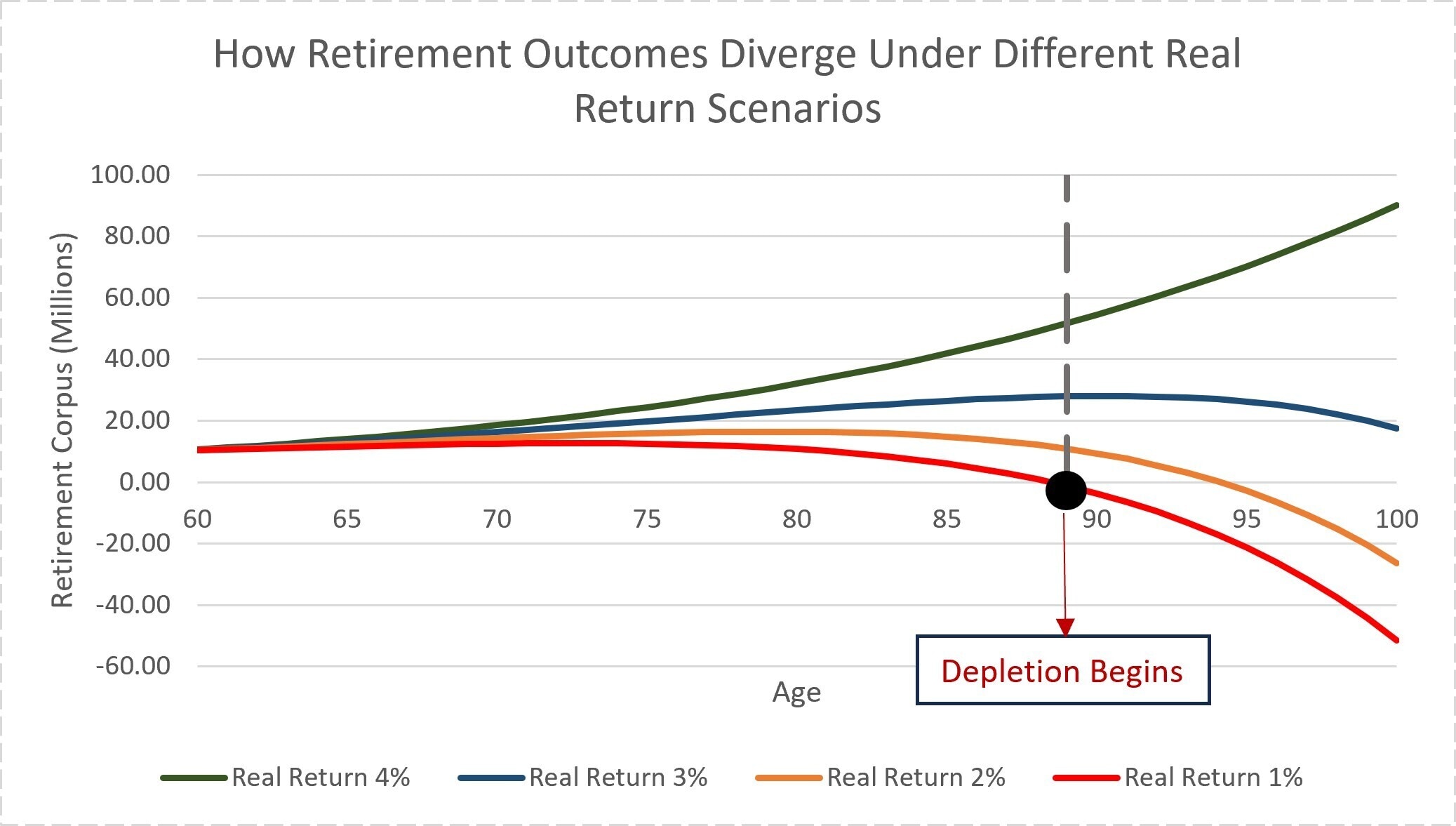

The analysis is based on a commonly used withdrawal approach: an initial withdrawal of 4% of the retirement corpus, with annual adjustments for inflation.

Instead of anchoring the analysis to a fixed time horizon, the focus is on how long the corpus can sustain under different realized real-return scenarios.

This brings into focus a central question: how sensitive is sustainability to the realized returns?

Small differences in returns compound over time

Over long periods, even modest differences in realized real returns can lead to materially different outcomes.

To illustrate this, the analysis considers a range of plausible real return scenarios and examines how the same withdrawal framework behaves under each.

The patterns that emerge are intuitive but important:

- Around 4% real return – outcomes remain broadly stable.

- Around 3% – sensitivity begins to emerge.

- Around 2% – sustainability reduces meaningfully.

- Around 1% – risk of early depletion increases significantly.

These differences become clearer when viewed over time.

The chart shows how outcomes diverge gradually. Early in retirement, paths appear similar. Over time, small differences compound, leading to increasingly different trajectories.

In some cases, this divergence results in early depletion, while in others the corpus sustains for much longer. The point at which this divergence becomes pronounced and, in certain scenarios, leads to depletion is clear.

The key observation is not the precise threshold but the degree of sensitivity. A change of even 1% – well within plausible variation – can materially alter sustainability.

This naturally raises the question of what drives such variation in practice.

Realized returns diverge from predicted averages due to evolving conditions

In practice, retirees adjust their investment approach to reflect their circumstances and preferences, often prioritizing stability and reducing exposure to volatility. These choices are entirely understandable.

At the same time, portfolio structure influences the returns that are ultimately experienced. Different approaches can lead to different outcomes, even under similar market conditions.

The implication is not that one approach is preferable to another but that realized outcomes reflect both market conditions and how portfolios are positioned.

Taken together, these observations point to a broader perspective. The challenge is not simply that returns vary over time. It is that realized returns can differ meaningfully from what is assumed at the outset.

When withdrawal strategies are built around a fixed rate, they implicitly rely on outcomes remaining within a certain range. Over time, this may not hold.

As differences accumulate, their impact becomes more visible. What begins as a modest deviation can lead to materially different outcomes. Sustainability, therefore, is shaped not only by the rule itself but by how it interacts with evolving conditions.

Withdrawal timing can impact real returns

This does not diminish the value of commonly used withdrawal approaches. Rather, it highlights that sustainability depends not only on expected returns but on realized outcomes.

Withdrawal strategies are thus better understood as frameworks operating within changing conditions, rather than as static rules defined at a single point in time.

Realized real returns are one important dimension of retirement income uncertainty and the timing of those returns could compound their effects.

Even when long-term averages appear adequate, the order in which gains and losses occur can shape outcomes in ways that averages alone do not capture. Poor returns experienced early in retirement – before the corpus has had time to recover – can have a materially different impact than the same returns experienced later.

This is sometimes described as sequence-of-returns risk and it interacts directly with the dynamics of the fragile real: a period of poor real returns, arriving at the wrong moment, can accelerate depletion well beyond what the average return scenario might suggest.

Together, these two forces – the level of realized real returns and the sequence in which they arrive – determine much of what actually happens to a retirement corpus over time.

Understanding them helps explain why outcomes can diverge so significantly, even when the underlying withdrawal rate and assumptions about the long-run return appear reasonable.

The “fragile real” offers a way to better interpret how retirement income strategies behave as conditions evolve and how their sustainability is ultimately determined.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Real Estate

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Genevieve Bennett

August 5, 2026