The massive impact of IT and software on modern business

Business dynamism is falling across the developed world. Image: REUTERS/Eric Thayer

Productivity growth has declined sharply across advanced economies since the mid-2000s. In the US, productivity growth between 2005 and 2018 averaged less than half its long-term rate. This slowdown followed after an episode of above-average growth in the 1990s, fuelled by the rise of information and communication technologies (Fernald 2015). A similar slowdown occurred in most European countries. Indeed, productivity in France and the UK has almost flatlined for the last 15 years.

The initial surge and subsequent decline in productivity growth coincided with two other macroeconomic trends: the fall of business dynamism, and the rise of corporate market power and firm concentration. Business dynamism, which is the process of firms growing, shrinking, emerging, and failing, has been declining for the last 30 years. Signs that business dynamism is weakening include the decline of the rate at which workers reallocate to new employers (e.g. Decker et al. 2018) and the decline in the number of startups as a fraction of all firms in the economy (e.g. Calvino et al. 2016, Pugsley and Sahin 2018). Recent research on market power shows that the mark-up that firms charge over their marginal costs has increased sharply, while the share of output produced by the largest firms in a sector has risen over the same timeframe (De Loecker et al. 2018, Autor et al. 2017).

The rise of intangible inputs

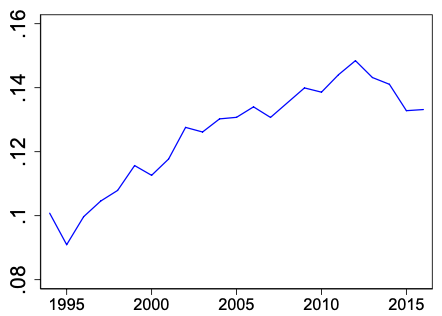

In a new paper (De Ridder 2019), I argue that these trends can be explained by the rise of intangible inputs, such as information technology (IT) and software. I argue that if some firms rely more heavily on intangible inputs in their production process than others, this has a negative effect on the entry of new firms, as well as on long-term growth and innovation. Figure 1 depicts the dramatic increase in the importance of intangibles – software and database investments alone make up over 25% of total investments in France today.

Figure 1 Software investments as a percentage of non-residential gross capital formation

A key difference between intangible and other (tangible) inputs is that intangibles scale – they can be duplicated at close to zero marginal costs (Haskel and Westlake 2017). This means that when intangible inputs are used to produce a good, the cost structure of production changes. Firms need to invest in the development and maintenance of intangible inputs but face minimal additional costs of using these intangibles when production is scaled up. A rise in the use of intangible inputs therefore shifts the cost of production away from variable towards fixed costs. This notion is confirmed in Figure 2, which plots a new measure of fixed costs as a fraction of total costs using balance sheet and income statement data on the universe of French firms. In my paper I furthermore show that fixed costs are higher in service and ICT industries, and that the ratio of fixed-to-variable costs increases significantly when firms adopt large IT systems.

Figure 2 Fixed costs as a fraction of total costs

From intangible inputs to untouchable firms

To show how these scalable intangible inputs can drive the three macroeconomic trends, I embed them in a rich model of endogenous growth. Firms produce one or multiple products, that are added or lost through creative destruction. They invest in research and development (R&D) to produce higher quality versions of goods that other firms produce. Successful innovation then causes the innovator to become the new market leader.

Intangible inputs change the innovation process in the model, because they introduce a trade-off between quality and price. If some ‘IT superstars’ are able to deploy intangible inputs with greater efficiency, they are able to reduce their marginal costs by a greater fraction, which allows them to sell at lower prices. If a firm with less intangible adoption develops a higher quality version of a good that one of these firms sells, the incumbent could undercut the innovator on price. They therefore become ‘untouchable’, and are able to hold on to market leadership. The presence of firms with a high take-up of intangible inputs, therefore, deters other firms and entrants from innovating and developing higher quality products. They also reduce the effect of R&D activities on growth, making ideas ‘harder to find’ (Bloom et al. 2017).

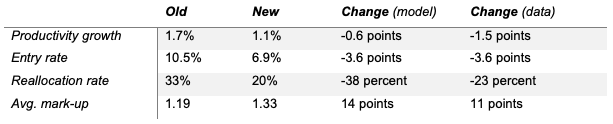

Table 1 summarises these long-term effects quantitatively. The model is calibrated using data on French firms and shows that the rise of high-intangible firms is able to explain a significant fraction of the slowdown of productivity growth.

Table 1 Comparison of steady states before and after the rise of intangibles

Note that despite these long-term effects, the initial effect of the rise of high-intangible firms is positive. Firms with high intangibles ‘disrupt’ sectors across the economy by investing more in R&D, which causes economic activity to concentrate disproportionately around these firms. As the economy transitions to the new balanced growth path, there is an initial increase in productivity, as firms deploy more intangible inputs. This comes with an increase in mark-ups because market leaders have a larger cost-advantage over their competitors, although the increase in fixed costs implies that mark-ups overstate profitability. Mark-ups also offset the effect of the decline in marginal costs on prices, which could explain why the last decade has been simultaneously characterised by rising mark-ups and low inflation.

Discussion

This column is not the first, and likely not the last, to analyse the slowdown of productivity growth and to link it to the decline in business dynamism, market power, or both. The secular decline in real interest rates may have stimulated investments by market leaders more than followers for example (Liu et al. 2019), while anti-competitive (patenting) behaviour by incumbents may have reduced the diffusion of new technologies (Akcigit and Ates 2019). IT might have increased the span of control of firms, causing a reallocation to high-productivity firms with high mark-ups, while lowering innovative investments by incumbents (Aghion et al. 2019).

This column has outlined a complementary view. It shows that when some firms are able to deploy intangible inputs with greater efficiency, long-term productivity growth falls. This is not because there is less investment in innovation, but because these investments are less likely to be successful. This causes innovation to concentrate within a small fraction of firms and has a negative effect on entry.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Inclusive Growth Framework

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

John Letzing

July 3, 2026