Action, not ambition, is now defining net-zero leadership

More investors want to see action, not just ambition, when it comes to corporates' climate transition plans. Image: Getty Images/serts

Shantanu Srivastava

Research Lead, Sustainable Finance & Climate Risk, South Asia, Institute for Energy Economics and Financial Analysis (IEEFA)- A well-articulated climate transition plan can show existing and potential investors how a company will decarbonize while remaining profitable.

- But investors want to see action, not just ambition, when it comes to climate transition planning.

- A recent analysis of the climate transition plans of Indian firms shows how this shift is impacting companies of all sizes, across industries.

Since the start of the decade, companies around the world have set ambitious net-zero goals. And, on paper at least, corporate ambition appears unprecedented. The Science Based Targets initiative (SBTi) lists more than 10,000 companies with validated decarbonization targets and over 2,000 with net-zero targets, underscoring growing corporate ambition.

But investor scrutiny is zeroing in on climate transition planning and whether these plans can actually produce results.

A key aspect of corporate climate transition plan disclosures is the impact on capital flows, investor confidence and the overall credibility of sustainable finance markets. According to an International Organization of Securities Commissions (IOSCO) survey of global investors, while climate transition plans are in the nascent stages, market participants are increasingly interested in using them for capital allocation, risk assessment, pricing, valuation and decision making.

Indeed, a well-articulated climate transition plan can help a high-emitting entity to demonstrate to existing and potential investors how it will decarbonize while remaining profitable. Investor signals are also being reinforced by rapidly evolving disclosure expectations. The International Sustainability Standards Board (ISSB) disclosure standards have been adopted in 37 jurisdictions globally. And, in June 2025, the IFRS Foundation released a guidance document on transition plan disclosures within the IFRS S2 standard, effectively endorsing Transition Plan Taskforce-aligned disclosures.

As a result, it’s increasingly important for companies to be able to show concrete results from their climate transition plans, if they wish to access the global sustainable finance markets. This is particularly true for companies in emerging markets that wish to tap into growing investor interest in sustainable businesses around the world.

Climate transition planning in emerging markets

Indian corporates and sovereign entities raised $14.5 billion from sustainable debt markets in calendar year 2025, according to Bloomberg New Energy Finance – a modest amount compared to the $2.2 trillion raised globally during the period. As global capital pools look for execution, not just ambition, when it comes to climate transition planning, Indian entities in hard-to-abate sectors must deliver results to remain competitive in global sustainable finance markets.

India’s Business Responsibility and Sustainability Reporting (BRSR) standards have brought the country's corporate reporting closer to global standards. However, while BRSR requires disclosures on emissions, governance and sustainability strategies, these remain siloed. This makes it difficult for stakeholders to understand how companies plan to translate climate ambitions into actionable steps and measurable outcomes. BRSR also does not yet include dedicated climate transition plan disclosures.

As global frameworks converge around transition planning, this gap could affect how international investors assess firms’ preparedness in India, and in other emerging markets currently at a similar stage when it comes to corporate climate transition planning.

A divide in climate transition planning

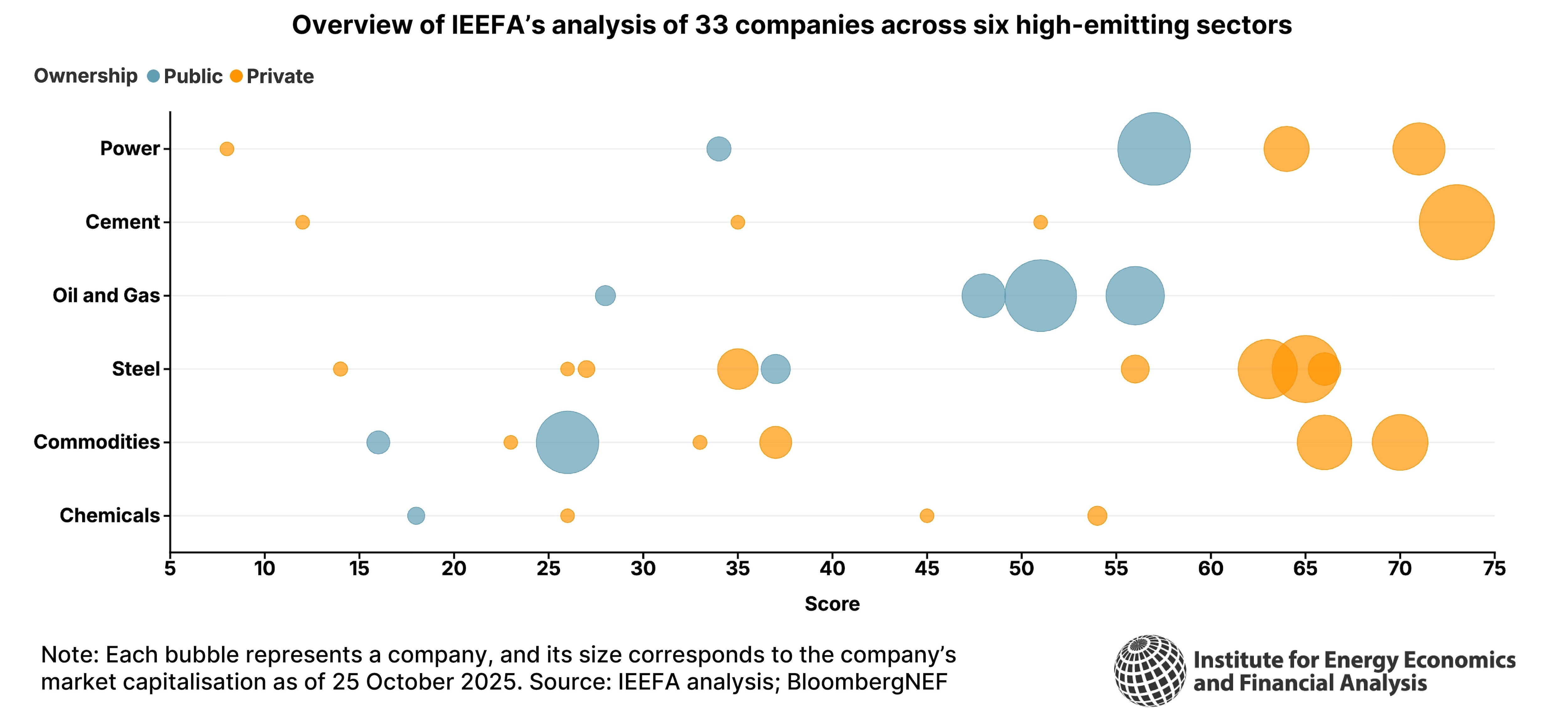

A recent Institute for Energy Economics and Financial Analysis (IEEFA) study of public disclosures on climate transition planning by key entities in high-emitting sectors in India reveals a clear divide. Large globally exposed companies outperform small and mid-sized firms, and also public sector peers, in transition planning disclosures.

Additionally, companies with large capitalizations score almost twice as high as small and mid-sized firms, across sectors. This reflects a deep structural issue in terms of capacity, internal data systems and processes, and the existence of a compliance-driven mindset among smaller corporates.

Across sectors, execution is the weakest link

Most companies analyzed by IEEFA identify at least one action to decarbonize their operations – from renewable energy adoption and energy efficiency improvements, to using green hydrogen and carbon capture technologies. However, these levers are rarely linked qualitatively with climate ambitions such as a net-zero target. Few firms demonstrate how specific actions contribute to emissions reduction over time.

The analysis also shows that governance structures remain largely procedural and have yet to translate into clear accountability, incentive alignment or execution capacity for delivering climate transition plan objectives. The weakest governance component overall is incentives and remuneration, with only a handful of large internationally exposed companies disclosing mechanisms linking climate targets to compensation.

Translating climate ambition into quantified, time-bound and financially integrated execution pathways is another weak point. Most companies do not demonstrate a link between transition actions and corporate budgeting. Internal carbon pricing is largely absent, with only a third of companies reporting its use, according to the IEEFA analysis. Even fewer report using it for capital allocation decisions.

Engagement with stakeholders also remains process oriented. Companies recognise their reliance on suppliers, customers and policy-makers for achieving their climate transition plan objectives, but few show how these relationships will be managed.

Lastly, disclosure of how transition plans translate into measurable and verifiable outcomes also remains weak. Across sectors, reporting on emission inventory largely stops at Scope 1 and 2 emissions. Third-party verification practices are still evolving and the alignment between climate strategy and business decisions is also unclear.

While the analysis creates a dim picture of transition planning practices in India, it is important to look at it in the context of disclosures by companies in other markets. As the IOSCO survey mentions, transition planning practices are at a nascent stage globally. Jurisdictions that proactively support capacity building and regulations for robust climate transition planning will be frontrunners in the global capital markets of the future.

Coordinated action on climate transition planning

Strengthening climate transition plan disclosures in India will require a coordinated push from regulators and corporates.

For the regulator, releasing a BRSR–TPT–ISSB mapping framework, updating existing BRSR guidance to explicitly embed transition planning elements and introducing a one-page "transition plan snapshot" within BRSR filings should be short-term priorities.

For corporates, transition planning must shift from being a reporting exercise to become a strategic tool. Climate targets should be integrated into corporate strategy and capital allocation processes. Executive incentives must be linked to climate milestones. Also, supplier engagement and workforce reskilling should move from acknowledgement to implementation.

Global capital markets are moving rapidly from rewarding climate action to pricing climate execution. As disclosure regimes converge around ISSB-TPT-aligned transition planning, emerging market corporates will also be assessed on the credibility, financial integration and delivery of their transition pathways, not just on the targets they announce.

Corporate climate transition planning stands at an inflection point. As capital providers increasingly value credible transition plans, firms that translate ambition into action will gain a competitive advantage, while those that treat it as a disclosure formality risk falling behind.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

The Net Zero Transition

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Economic GrowthSee all

Samaila Zubairu

March 3, 2026