Can systemic green transitions unlock a new generation of competitiveness under China's 15th Five-Year Plan?

As China enters its 15th Five-Year Plan period, its understanding of green transition appears to be expanding. Image: Ghostinmirror/Unsplash

- China’s 15th Five-Year Plan expands its green transition from decarbonization to comprehensive ecological resilience.

- Businesses must build system competitiveness by managing their impacts and dependencies on nature alongside their carbon footprints.

- How promising ideas become scalable impact is a key focus at the World Economic Forum’s Annual Meeting of the New Champions, also known as Summer Davos, in China from 23–25 June.

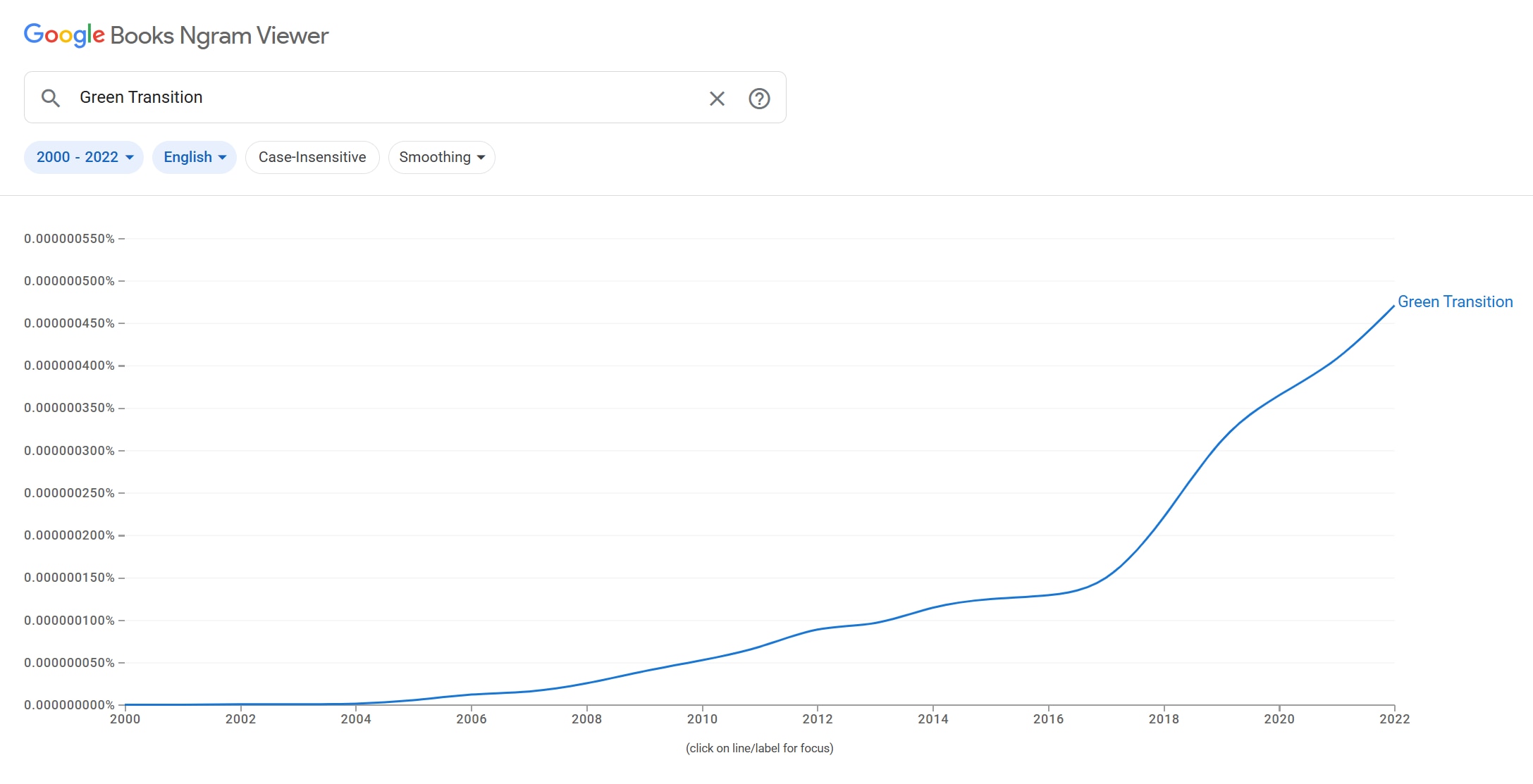

International observers often associate China’s green transition with climate action and clean energy. That perception is understandable. China is home to the world’s largest renewable energy market, the world’s largest electric vehicle market and one of the most ambitious carbon neutrality commitments among major economies.

Yet climate and energy tell only part of the story.

As China enters its 15th Five-Year Plan period (2026–2030), its understanding of green transition appears to be expanding. Part Thirteen of the Plan is titled “Accelerating the Comprehensive Green Transformation of Economic and Social Development and Building a Beautiful China.” The wording is significant. The focus is no longer solely on reducing emissions or deploying renewable energy. Instead, it encompasses the broader relationship between economic growth, resource efficiency, environmental quality and ecological conservation.

This raises an important question. What does “comprehensive green transformation” mean in practice? More importantly, can it create a new source of corporate competitiveness?

From green transition to comprehensive green transformation

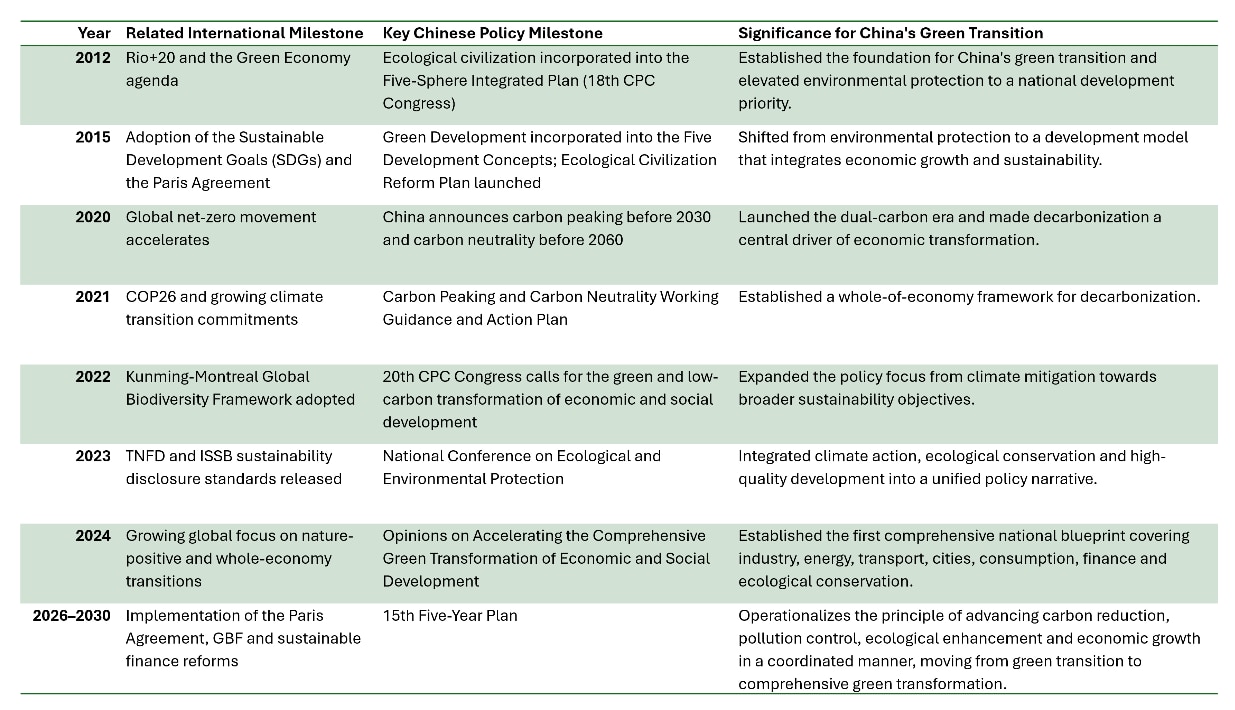

The comprehensive approach did not emerge overnight. It reflects more than a decade of policy evolution and increasing integration with global sustainability agendas.

Viewed as a whole, the trajectory is clear. China’s green transition has evolved from environmental protection, to green development, to the dual-carbon strategy, and now to comprehensive green transformation. This evolution has unfolded alongside major global sustainability agendas, while increasingly aligning domestic priorities with developments such as the Sustainable Development Goals (SDGs), the Paris Agreement and, more recently, the Kunming-Montreal Global Biodiversity Framework.

This broader perspective is reflected in the 15th Five-Year Plan itself. The plan adopts the principle of advancing carbon reduction, pollution control, ecological enhancement and economic growth in a coordinated manner.

The targets demonstrate this ambition. Alongside a 17% reduction in carbon emissions per unit of GDP between 2026 and 2030, the plan also aims to reduce water consumption intensity by 10%, lower PM2.5 concentrations in cities to below 27 micrograms per cubic metre and increase forest coverage to 25.8%. It also calls for stronger ecological protection, expanded green finance and more efficient use of resources such as water, land and minerals.

Climate remains central, but it is no longer the only lens through which green development is viewed. Increasingly, China’s green transition is about managing the interactions between climate, nature and growth.

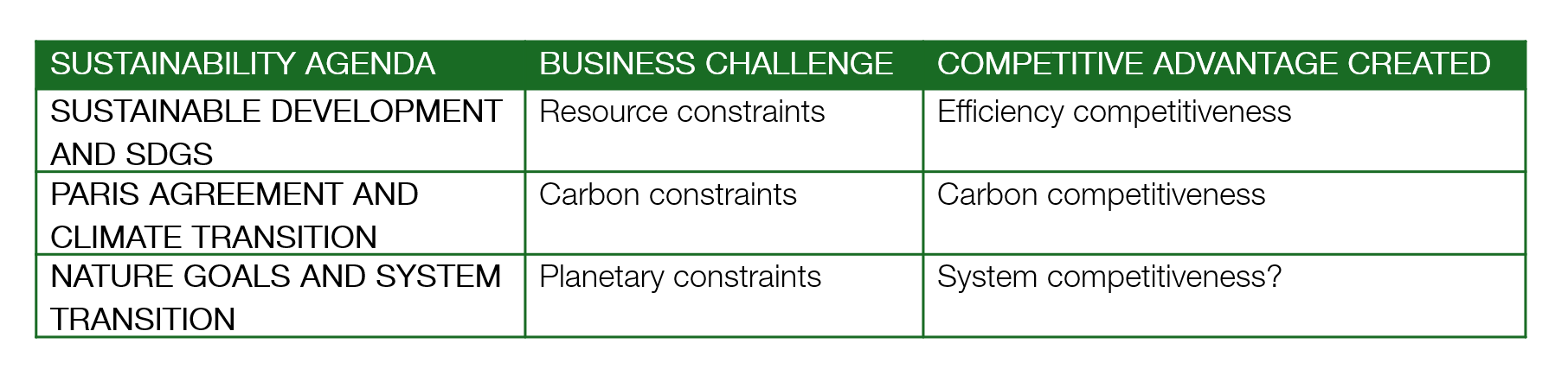

Three sustainability transitions, three sources of competitiveness

This evolution is not only changing policy. It is also changing the basis of corporate competitiveness.

Sustainability goals are often viewed as constraints on business. History suggests otherwise. Repeatedly, major sustainability transitions have created new opportunities for firms that moved early.

The first transition emerged from the global sustainable development agenda that gained momentum after the 1992 Earth Summit and was later reinforced by the SDGs.

As governments, investors and consumers paid greater attention to resource efficiency and environmental performance, leading companies discovered that sustainability could improve productivity rather than constrain it. Energy efficiency, waste reduction and cleaner production became strategic assets. Firms such as Toyota, Siemens and GE transformed environmental management into operational excellence. Sustainability became a source of efficiency competitiveness.

The second transition was catalysed by the Paris Agreement and the global race towards climate goals.

Carbon became a strategic business variable. Companies that could manufacture, transport and finance products with a lower carbon footprint gained access to new markets, customers and sources of capital. Tesla and BYD built a new electric mobility ecosystem. CATL scaled a new way of storing and releasing energy. This era rewarded carbon competitiveness.

A third transition is now emerging.

Unlike previous phases, it is not driven by climate alone. Businesses are increasingly confronting a broader reality: long-term economic value depends on the health of the natural systems that support production, consumption and trade. Water scarcity, biodiversity loss, land degradation and ecosystem disruption are becoming material business risks. These risks affect food systems, manufacturing supply chains, infrastructure and financial institutions alike.

Importantly, nature does not replace climate. Rather, it expands the scope of the transition, exposing a broader set of dependencies, including water, land, biodiversity and the ecosystem services that nature provides.

A company can reach net zero and still face material risks from water scarcity, degraded ecosystems, biodiversity loss or declining ecosystem services. Managing carbon is increasingly necessary, but it may no longer be sufficient.

As climate and nature goals converge, firms are being asked to manage something broader: the resilience of the systems on which they depend. If sustainable development rewarded efficiency and climate action rewarded decarbonization, the next transition may reward the ability to create value while strengthening the resilience of economic and ecological systems.

This may be the emergence of a new source of advantage: system competitiveness.

System competitiveness is already beginning to emerge in several sectors. Food companies increasingly depend on resilient agricultural landscapes, healthy soils and reliable water supplies. Battery and electric vehicle manufacturers face growing pressure to manage the environmental impacts of critical mineral supply chains. Water-intensive industries, including semiconductors and advanced manufacturing, are discovering that ecosystem resilience can be as strategically important as energy security. In each case, competitive advantage increasingly depends on how effectively firms manage their relationship with the broader systems on which production depends.

China’s 15th Five-Year Plan is significant because it attempts to operationalize this convergence at scale. Rather than treating climate, nature and growth as competing priorities, it seeks to align them within a common framework for modernization and high-quality development.

Can markets be reshaped for the new generation of system competitiveness?

Yet history also offers an important lesson. Competitiveness does not emerge simply because governments announce new goals. It scales when markets reward it.

Efficiency competitiveness expanded because markets rewarded lower costs. Carbon competitiveness expanded because carbon markets, green finance, procurement standards and net-zero commitments created demand for low-carbon solutions. The challenge for the nature transition is different.

Businesses are increasingly expected to restore ecosystems, improve water security, strengthen supply-chain resilience and contribute to biodiversity outcomes. Yet the benefits often extend far beyond the company making the investment. A company investing in watershed restoration may improve water security for entire communities and industries while capturing only a fraction of the economic value it creates. Nature generates public value more easily than private value.

This is where China’s 15th Five-Year Plan becomes particularly interesting. Beyond environmental targets, China is increasingly experimenting with mechanisms designed to translate ecological value into economic value. More than 200 Gross Ecosystem Product (GEP) accounting projects have been carried out across the country, helping measure ecosystem services and explore pathways for translating ecological value into economic value. Biodiversity finance is also gaining momentum, with over 26 provinces having trialled the Biodiversity Finance Catalogue since October 2025.

Collectively, they represent early attempts to build markets around ecosystem outcomes. If successful, these mechanisms could do for nature what carbon markets, green finance and renewable energy incentives did for climate: create economic rewards for activities that generate public environmental value. The challenge is no longer whether ecosystem resilience matters. The challenge is whether markets can learn to value it.

In that sense, China’s 15th Five-Year Plan may become one of the world’s most important experiments in translating global nature goals into a new source of economic competitiveness.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

The Net Zero Transition

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Energy TransitionSee all

John Dutton

August 6, 2026