Is global trade and financial fragmentation here to stay?

Restrictive trade and financial policies can be self-perpetuating, making it politically difficult to remove them and raising the risk of escalation. Image: REUTERS/Carlos Barria

- The period from 2025 to early 2026 marked a turning point in global trade and finance, as a wave of tariffs and trade and investment restrictions was imposed.

- By creating concentrated domestic winners, restrictive trade policies can become politically difficult to unwind, making these policies self-reinforcing.

- New analysis from the World Economic Forum and Oliver Wyman shows that fragmentation is already costing the global economy, and the damage could get much worse.

From 2025 to early 2026, policymakers in several large economies implemented a raft of tariffs and trade and investment restrictions that are fragmenting the world’s commercial and financial systems more than at any point in recent decades.

Resilience and security concerns – exacerbated after the COVID-19 pandemic – are making countries more willing to use protectionism after decades of driving for efficiency and the expansion of free trade. The result is an erosion of shared norms that underpin the global financial system.

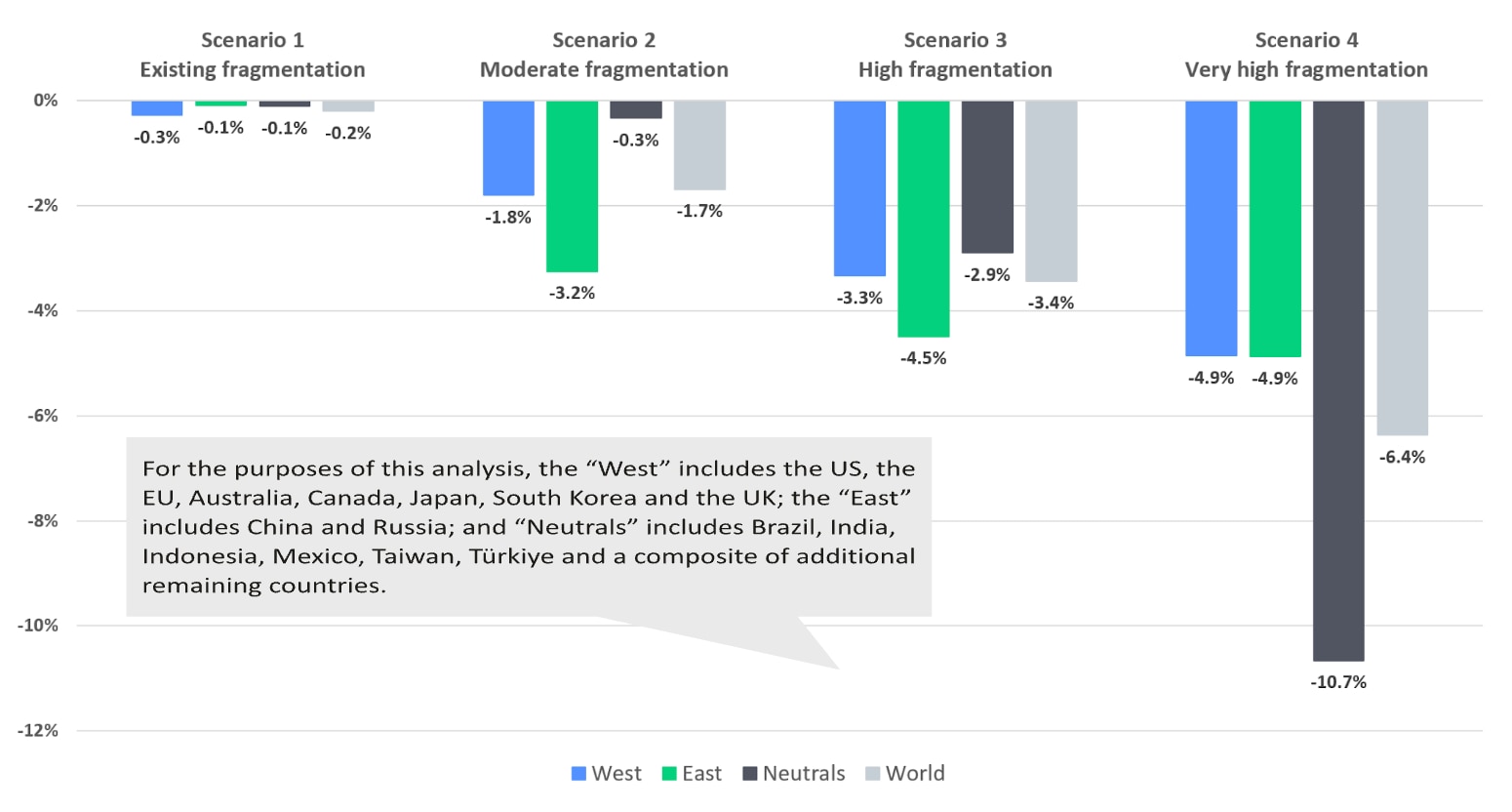

A newly released analysis from the World Economic Forum indicates that policies already in place could curb global growth by at least 0.2 percentage points (pp) and put upward pressure on inflation, while an increasingly likely worst-case escalation could raise this cost to as much as 6.4 pp and increase inflation by 6.1 pp. These impacts do not include the negative economic effects of the current conflicts in the Middle East and Europe, which only compound the damage.

The global economy may remain saddled with these protectionist policies for some time as they bolster certain domestic industries and subsets of workers within the country imposing them. If those beneficiaries grow dependent on these protections, they are likely to advocate for their preservation and expansion. This self-reinforcing nature of restrictive policies raises the likelihood of damaging escalation.

A turning point in global trade and finance

How did the recent acceleration in fragmentation start? Beginning in January 2025, the US embarked on an effort to remake global trade with major changes in trade and investment policy, including tariff increases across a wide range of trading partners. China was the target of some of the most severe US measures. It retaliated with its own damaging restrictions, including unprecedented export controls on critical minerals, and rerouted its state-subsidized exports away from the US, threatening industrial sectors in many countries. The US imposed restrictions on trade with its geopolitical adversaries and partners alike, accelerating efforts among countries to diversify, including among large European investors.

When imposing tariffs, the US government cited familiar arguments: revitalizing an ailing US manufacturing sector, restoring manufacturing jobs and narrowing the record-high US goods trade deficit. These measures hurt national economies in aggregate by pushing up prices and slowing growth, even if they benefit individual industries.

The economic cost of fragmentation

The new report from the World Economic Forum, in collaboration with Oliver Wyman and NERA, quantifies the impact of recent trade policies on economic output and inflation, and estimates the potential economic costs of escalation.

Restrictions implemented as of March 2026 (Scenario 1 in Figure 1) reduced GNE growth prospects by 0.2 pp relative to projected growth before their implementation at the start of 2025. Scenarios 2 through 4, which model progressive escalation in fragmentation between blocs, show that further increases in tariffs and other restrictive policies could cause substantially greater damage.

Marginal change in output

Deviation from baseline at one year

Meaningful reallocation of capital and production is underway

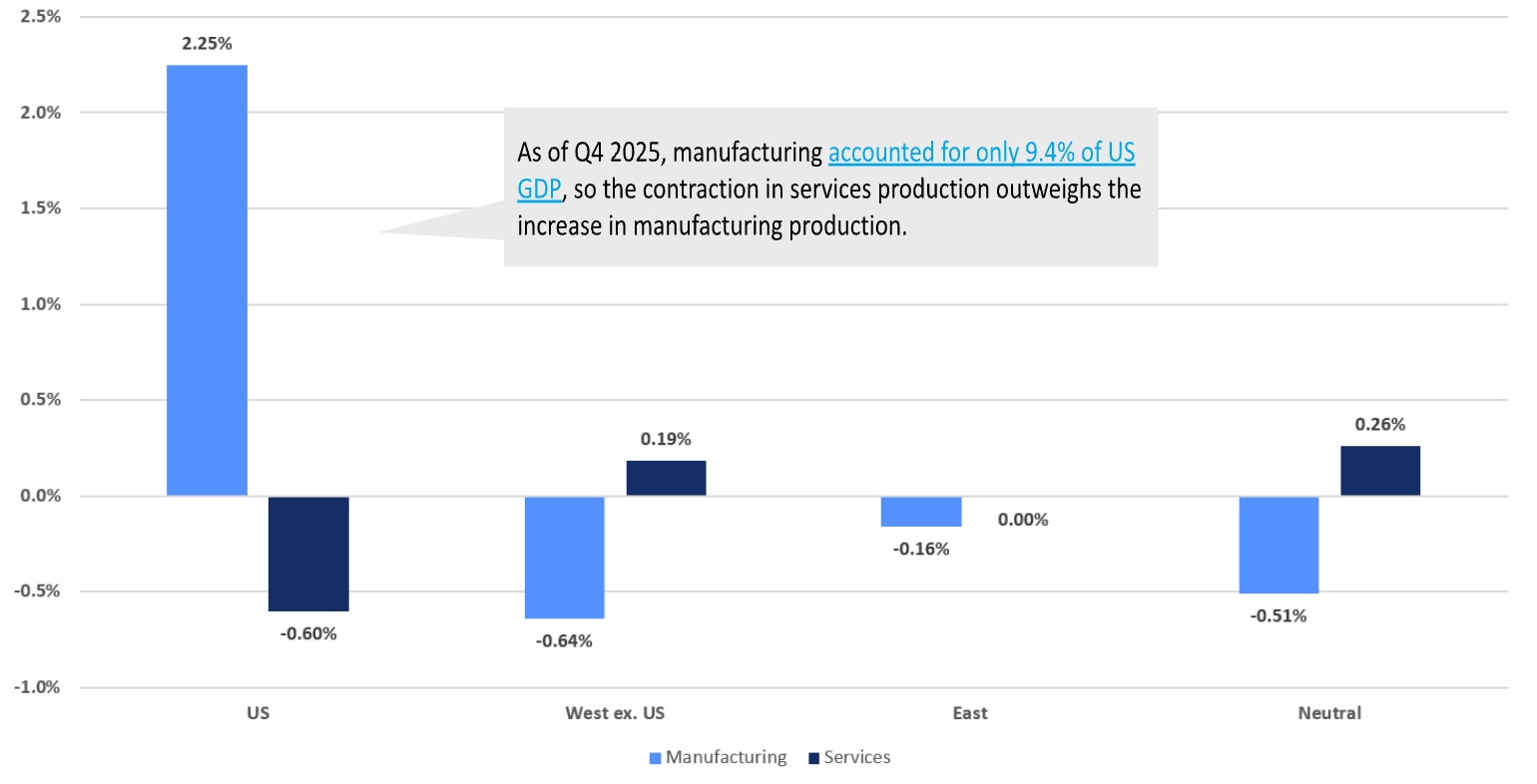

Existing trade policies are shifting production patterns across blocs. In the US, the current higher import tariffs are projected to lift manufacturing output by 2.25%, as consumers and firms substitute away from imports and adjust supply chains, a finding consistent with a recent analysis by the Budget Lab at Yale. But increased tariffs also raise input costs and wages in all sectors, pushing up prices, reducing real income (including for low-skilled workers) and contributing to an overall 0.60% drop in US services demand and output.

For countries being targeted by tariffs, the opposite sectoral shifts are taking place. In the West (excluding the US) and among neutral countries, manufacturing output falls as exports lose their competitiveness due to increases in the price of raw materials and other inputs, lifting overall prices and reducing goods demand. Meanwhile, services output rises as spending shifts toward domestic services, with consumers choosing restaurants and other hospitality services spending over purchases of goods. In the East, manufacturing declines less, so reallocation toward services is limited, leaving output in the sector broadly unchanged.

Long-run real production change by country group and sector group in the existing fragmentation scenario

Deviation from baseline at five years

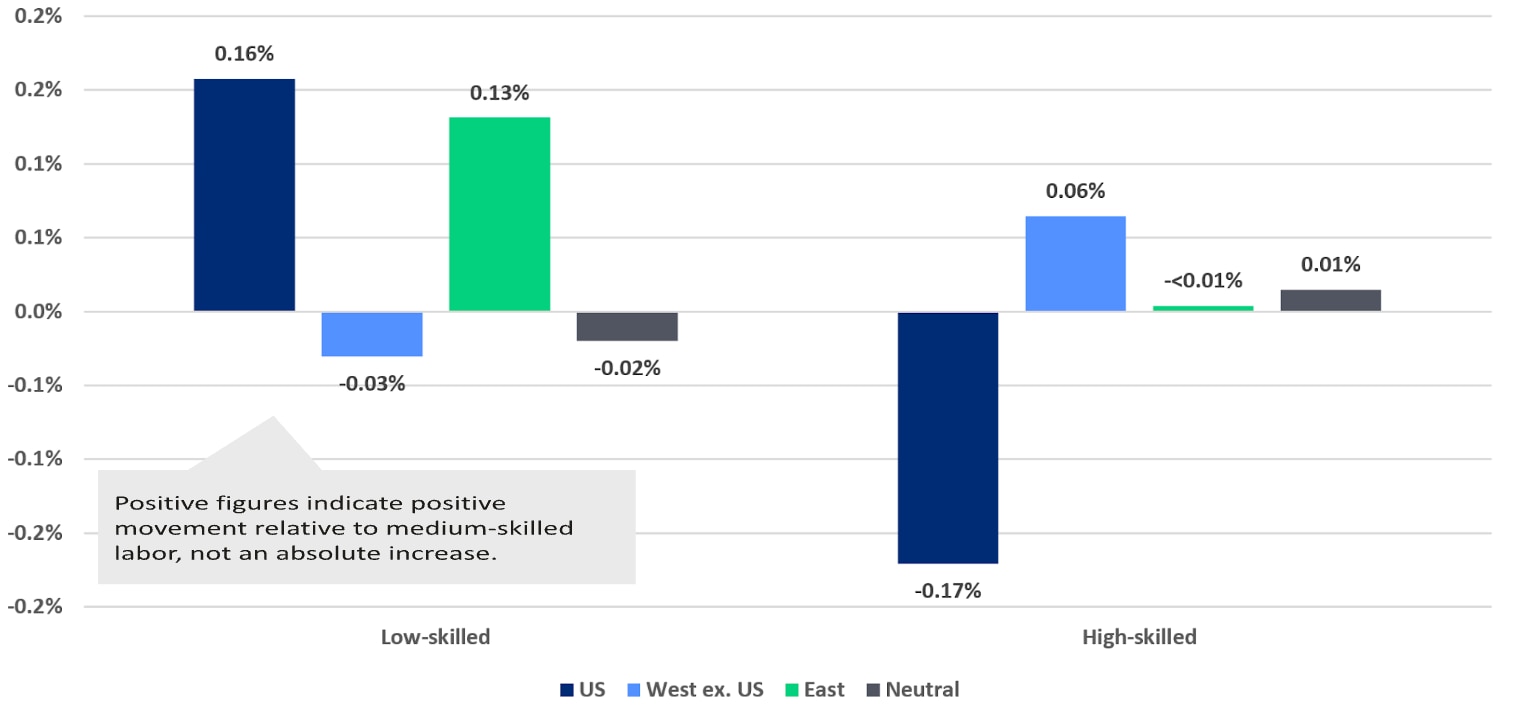

These sectoral changes affect wage trends across skill levels. In the US, the key takeaway is that higher import tariffs reduce real wages across all skill groups, making workers across the economy worse off. But on a relative basis, they shift income toward industrial workers relative to other workers as reshoring production by manufacturers boosts labour demand and relative wages.

In the West (excluding the US) and among neutral countries, declines in manufacturing output reduce demand for low-skilled workers, putting downward pressure on their relative wages. This drop is much more limited in the East, meaning wages for low-skilled workers in countries like China are least affected by existing restrictive trade policies. Overall, the model shows that existing policies have a modest but clear effect on wages.

Wage differentials for low- and high-skilled workers in the existing fragmentation scenario

Deviation from baseline at one year, relative to medium-skilled labour

Limiting costly and self-reinforcing trade restrictions

Restrictive policies become self-reinforcing because the reallocation of capital and production described above creates constituencies that benefit from their continuation, while the broader public tends to be less aware of their impact. This makes it politically difficult to reverse course, which can make the escalatory scenarios more likely. In a recent illustration of this tendency, the Biden administration largely retained tariffs imposed on China in the first Trump administration.

While restrictive policies may boost output and jobs in certain US industries (and in other countries that impose such protections), they will ultimately reduce total economic output domestically and globally. Research identifies protectionism as a costly way to save jobs. For instance, the 2018 US washing machine tariffs were estimated to cost consumers over $815,000 per job created annually.

Beyond higher consumer prices, protectionism’s promised gains of more jobs and revitalized industries are far from guaranteed. For instance, one study found that protectionist policies raised employment in only a minority of cases, while another found that higher input costs reduced jobs downstream. There is also evidence that restrictive measures have a poor track record of improving the long-run competitiveness of protected industries. For instance, a US International Trade Commission review of five industries that received temporary import relief found that only one modernized. Most sought renewed protection after it expired, suggesting these policies often shield inefficient firms rather than revive industries.

A “status quo bias” – with concentrated beneficiaries and diffuse costs – means the political cost of liberalization can outweigh the broader economic gains. This bias, in addition to deepening mistrust among major powers, makes it difficult to revert to a more integrated global economic environment.

These dynamics underscore the need for policymakers to align on effective norms for economic statecraft, including preserving the independence of central banks and structuring domestic and multilateral policies to support financial stability. Aligning with these voluntary norms will allow policymakers to continue to pursue resilience and security objectives without creating a self-reinforcing cycle of subsidy and inefficiency. Otherwise, today’s renewed reliance on restrictive policies risks entrenching fragmentation as a durable feature of the global economic and financial system.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Trade and Investment

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Financial and Monetary SystemsSee all

Veronica Frisancho

July 23, 2026