The energy transition's foundations are weakening. The US-Iran crisis shows why that matters now

The US-Iran war is creating a short-term brake on the energy transition Image: via REUTERS

- The US-Iran war created a short-term brake on the energy transition but may also strengthen the long-term case for cleaner, more secure systems.

- Energy security is no longer only about oil and gas supply; it now includes grids, critical minerals, finance, technology supply chains and regional cooperation.

- The countries that are best insulated today invested in diversification and clean capacity long before this crisis hit.

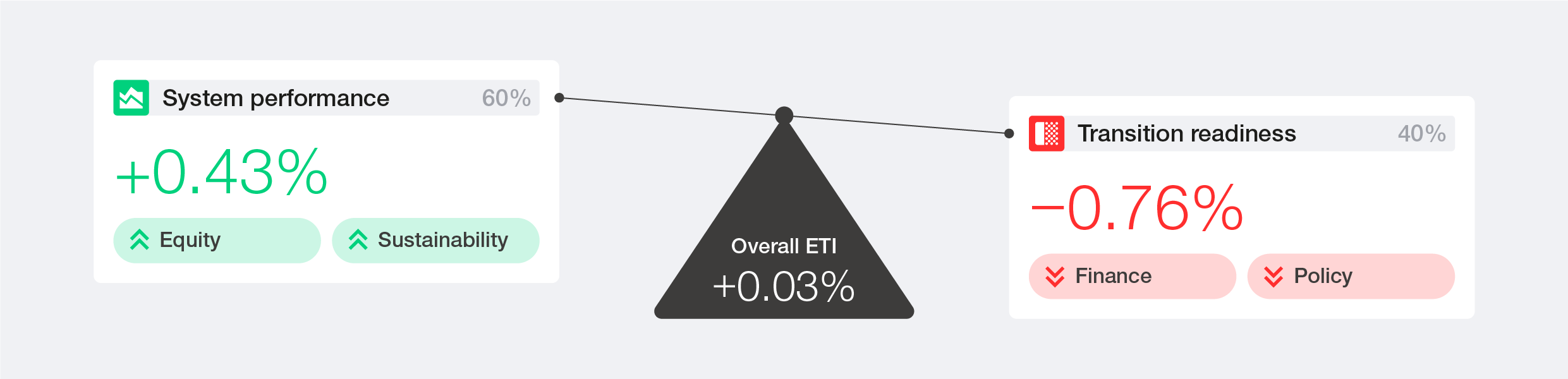

For the first time in over a decade, the conditions needed to sustain the energy transition are weakening. The 2026 Energy Transition Index, which tracks 120 countries across 44 indicators, finds that transition readiness fell this year, with four of five enabling dimensions declining simultaneously.

That makes the decisions facing governments and businesses only more important. When the US-Iran war started in 2026, the immediate question for energy markets was familiar: how would oil and gas prices be affected?

However, for the energy transition, the harder question is: what does a shock of this scale do to the transition itself?

This year’s index, built on pre-crisis data, highlights the vulnerabilities clearly exposed by the Hormuz crisis.

Overall, the progress was near-flat (+0.03%); however, the conditions that make future progress possible, essentially the readiness for the transition, policy stability, investment access, innovation capacity and infrastructure, have weakened together.

The energy system was already under pressure on multiple fronts before the crisis hit. Geopolitical fragmentation was reshaping supply chains and critical mineral flows.

Financing conditions in emerging markets were tightening. Policy credibility was weakening in several major economies. Infrastructure investment was lagging. None of these pressures was new; each had been building for years.

While the war did not create these vulnerabilities, it brought them all to the surface at once. The countries now managing best are precisely those that addressed these pressures before they converged.

What the Energy Transition Index shows on current performance

System performance continued to advance in 2026. Renewables and nuclear reached 42% of global electricity generation. Nearly 800 gigawatts of renewable capacity were added. Energy efficiency improved across 92 economies.

The exception is energy security, which was the only system performance dimension to decline, falling 0.9%, driven by weaker supply diversification (-0.7%) and a sharp drop in reliability (-3.0%). These weaknesses predate the Hormuz disruption. The crisis has amplified them.

Energy shocks remind policymakers that dependence on imported fossil fuels creates vulnerability, while local energy supply, including domestic renewables, provides resilience.

For example, Vietnam's solar build-out, initially pursued primarily as a climate measure, is providing a meaningful buffer against gas-price spikes. Such shocks often result in a short-term rise in emissions, followed by a longer-term structural shift toward cleaner energy systems. The 2022 European gas crisis is the most recent example.

This crisis will put affordability gains under sustained pressure in the most exposed markets. While advanced economies can absorb higher energy costs through strategic reserves and fiscal headroom, many emerging markets are simultaneously managing energy access, fiscal stability and transition investment, with less room to accommodate all three.

The Association of Southeast Asian Nations (ASEAN) alone is absorbing an estimated $3.4 billion per month in excess energy costs. India has recommissioned coal. South Korea has lifted coal generation restrictions. The Philippines has declared a national energy emergency.

How are companies and governments responding?

The crisis has compressed the decision window for companies too. Energy value chain exposure across fuels, minerals, and grid connectivity is being assessed with the same rigour as financial risk. System integration capability is emerging as the competitive differentiator for the decade ahead.

As a response to the Hormuz crisis, some countries are reaching for short-term tools – rationing, price caps, extended coal generation – that eases immediate pressure but may erode investor predictability and risk recreating the supply distortions that worsened past energy crises.

Others are using the moment to accelerate longer-horizon arrangements that few countries could deliver alone.

ASEAN is moving down the second path. The bloc is accelerating the regional cooperation it has been advancing for years.

The ASEAN Power Grid initiative, which is now backed by financing from the Asian Development Bank and the World Bank, could mobilize around $760 billion in generation and transmission investment by 2045, enabling resource sharing and a meaningful buffer against single-route exposure.

In parallel, Japan's Asia Zero Emission Community framework, originally designed to support the clean energy transition, is being repurposed as a regional energy security mechanism, with Japan committing financing to help Asian economies secure supply and build reserve capacity.

Cross-border power flows are no longer purely an efficiency measure; they are a security strategy. The European Union's setting up of REPowerEU to diversify its energy supply following the Ukraine-Russia conflict suggests this logic, once adopted, tends to hold even as the original crisis fades.

3 signals to watch over the next 12 months

1. A new justification for renewables

The US-Iran crisis is shifting the case for renewables from mostly cost and sustainability to a powerful additional security driver.

Unlike fossil fuels, domestic clean power is less exposed to chokepoints. China is accelerating hydrogen use with local wind and solar, while India and the EU are reviewing biofuel and clean-fuel mandates through a security lens.

Other countries are also considering how to accelerate electrification based on domestically available renewables and other energy sources. The political logic is shifting; clean energy is increasingly framed as an industrial security asset, and procurement decisions are beginning to follow.

2. How the ‘transition fuel’ narrative sustains under pressure

Around 19% of global LNG trade transits the Strait of Hormuz, with almost 90% bound for Asia. Japan and Korea are responding by locking in long-term contracts from additional sources; others are looking past gas entirely.

The signal to watch is the next wave of LNG contract decisions across Asia and whether gas demand projections through 2035 are revised downward.

3. Whether policy credibility becomes the new risk premium

Capital for energy and infrastructure investment prefers jurisdictions with stable, long-horizon frameworks. The 2026 Energy Transition Index shows that this is not a marginal effect: if recent trends continue, cost-of-capital divergence between markets is set to widen through 2026 and 2027.

For companies and investors, policy stability is now a vital question for returns on investment; it is a returns question. For governments, the binding constraint on the next phase of the transition is not technology or capital; it is credibility.

Stable rules, predictable regulation and credible delivery pathways are what unlock the next wave of private finance. Countries that grasp this will attract capital; those that do not will find the cost of delay rising faster than the cost of the transition itself.

The Middle East crisis has crystallized what the 2026 index data already showed: the transition is not just multi-speed, but structurally also divergent.

The immediate pressures will pass. What they leave behind, in policy and business choices made under duress, in capital redirected or withheld, in institutional credibility built or squandered, will shape the trajectory of the transition long after the crisis fades.

Ultimately, the impacts of this crisis on the energy decision will depend on decisions taken by business and government leaders in the coming months.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Energy Transition Index

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Energy TransitionSee all

Ayla Majid

July 28, 2026