Where is all the hydrogen?

Just a few years ago, hydrogen was the word on everyone's lips. So what happened? Image: REUTERS/Simon Johnson

- Forecasts predict that hydrogen production in 2050 will be 35% lower than predicted in 2022, with clean hydrogen seeing an even steeper decline of 45%.

- Cumulative hydrogen investment is still forecast to reach $3.2 trillion by 2060, but the sector's previously predicted meteoric rise is looking more distant.

- Hard-to-electrify sectors, energy security and food security all depend on policymakers treating clean hydrogen as a genuine priority.

It feels like a mirage now. Just a few years ago, major politicians were declaring hydrogen the future. Five years ago, Germany’s leadership, for example, declared during a trip to the US that hydrogen was to replace natural gas in Europe’s largest economy – and that it would happen quickly.

Hydrogen, German leaders believed, would form part of an industrial strategy that was to modernize German industry and wean the country off imported natural gas. Then, when Russia attacked Ukraine in early 2022, the war became a catalyst for energy security, and hydrogen became a path to energy independence, not just a means of decarbonization.

Now, as the world faces another energy supply shock due to the conflict in the Strait of Hormuz, an obvious question follows: where is all the hydrogen?

What happened to the global push for hydrogen?

The priorities of global leaders in the years since the excitement over hydrogen peaked have changed. Renewable energy has been sidelined in the US, narrowing the path for green hydrogen. Although the government has supported low-carbon blue hydrogen projects, that backing does not match the billions in investment promised under the former administration’s Inflation Reduction Act.

Germany, another industrial powerhouse but with acute energy supply challenges, has had tough strategic decisions to make given the proximity of the Ukraine war and its reliance on imported energy, including from Russia. The country’s current leadership focused on a policy of “realism”, which also provides challenges for hydrogen. With government budgets under pressure, Germany’s approach translates to a more gradual implementation. The current federal government is also more open to blue hydrogen, which is in part a recognition that it is required for essential parts of Germany’s economy, including the expanding military.

New reality for hydrogen

That realism is reflected in the numbers of DNV’s new report into the hydrogen industry. DNV forecasts the amount of hydrogen produced in 2050 will be 35% lower than it predicted in 2022. Clean hydrogen is expected to see an even bigger decrease of 45%. Like most mainstream forecasters of the energy transition, the high cost of hydrogen and the lack of policy implementation have led DNV to revise our outlook.

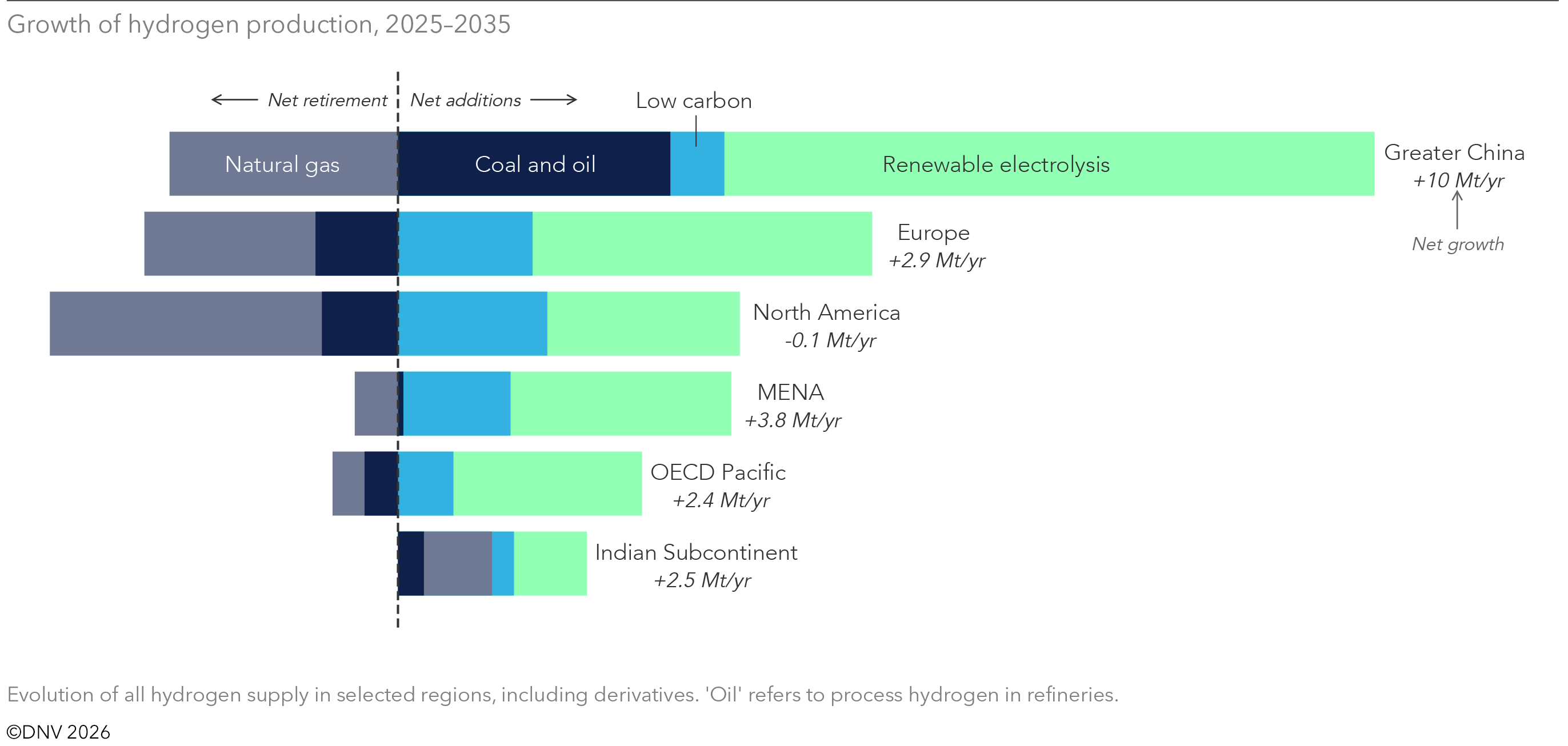

At the same time, this is far from an industry that is standing still. There are around 1,500 pilot projects that have been announced across the globe and cumulative hydrogen investment is forecast to be $3.2 trillion by 2060. And from a low base, renewable green hydrogen from electrolysis will grow 100-fold in the same time period.

What now for hydrogen and derivatives?

The closure of the Strait of Hormuz has highlighted the importance of hydrogen and its derivatives to products essential to our society, such as aviation fuel and fertilizer. In the short term, geopolitical events will accelerate final investment decisions in hydrogen projects as governments seek to protect supply chains. This will mean more clean hydrogen in Europe and China, although the latter will also turn to coal to meet hydrogen demand.

There is no hiding from the fact that clean hydrogen sits at the expensive end of decarbonization. It requires carrot and stick policies; subsidies and mandates including a credible carbon price to help the industry thrive. In China, hydrogen is gaining momentum thanks to policy support in the 15th Five-Year Plan and the rapid scaling of domestic power generation. In Europe, meanwhile, the case for hydrogen is buoyed by the world’s highest carbon price. Both Europe and China are likely to produce large amounts of clean hydrogen by 2040. That will happen not because clean hydrogen is competitive on its own, but because it will receive the support it needs.

In recent years the Middle East has also been building capacity and positioning itself as an export partner to Europe and Asia. It remains to be seen whether other countries are willing to risk outsourcing their hydrogen production to that region again.

De-risking hydrogen

De-risking hydrogen investments will be an important step in moving the industry from pilots to industrial scale. The challenge is whether it can be delivered at scale with sufficient certainty to attract capital. A confidence gap remains between technical capability and investor willingness, and closing it is essential not only to unlock investment but also to build broader societal acceptance.

Scaling hydrogen is not a matter of copy and paste. As projects move from megawatt pilots to gigawatt facilities, new risks emerge around system integration, safety and operational complexity that are not visible at smaller scale. At scale, risk no longer sits within individual components, but in the interaction between systems such as power supply, electrolysers, compression, storage and end use. Closing this gap requires early, structured risk management and greater standardisation.

Even if the sweeping ambitions of the hydrogen economy from just four years ago have fallen short, the case for clean hydrogen remains urgent. Hard-to-electrify sectors, energy security and food security all depend on policymakers treating it as a priority.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Hydrogen

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Energy TransitionSee all

Karikari Achireko

July 23, 2026