How is war in the Middle East reshaping Asia’s energy transition?

China's fast energy transition has helped it navigate the current geopolitical energy crisis. Image: Vida Huang on Unsplash

- Disruptions to flows through the Strait of Hormuz are reverberating across global energy markets, with Asia most exposed.

- Geopolitical disruption to fossil fuel supply is both a strong long-term argument for accelerating renewables deployment and a powerful short-term brake on doing so.

- Asia’s dependence on imported fossil fuels is turning geopolitical tensions into an economic strain, with energy security and diversification emerging as core strategic policy priorities.

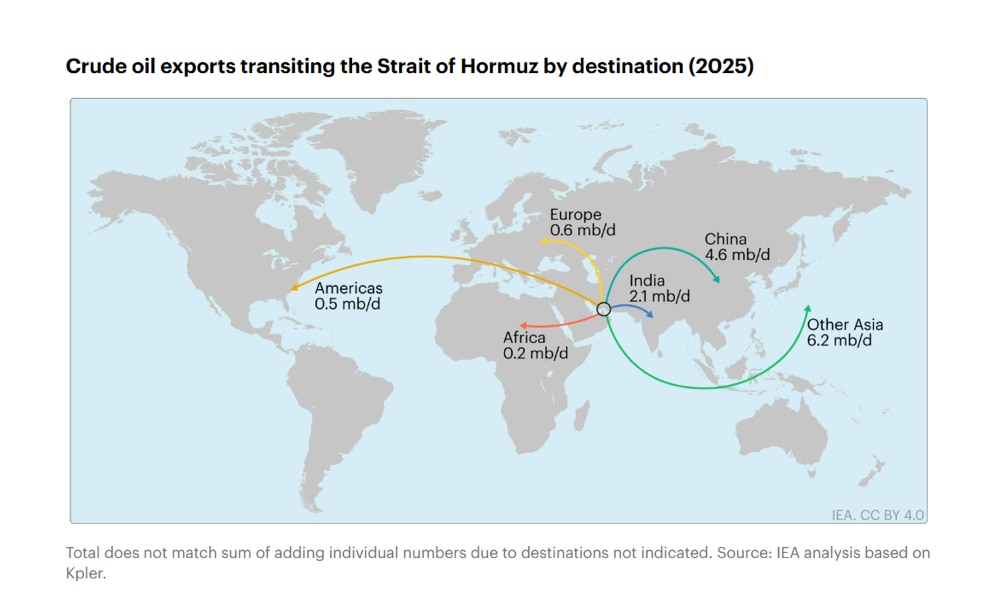

The Strait of Hormuz, a narrow waterway connecting the Persian Gulf to the Gulf of Oman, has become the pressure point through which Asia's energy security is being tested.

In late March, after war broke out in the Middle East, the Philippines declared a national energy emergency, exposing a broader vulnerability affecting the Asia-Pacific region. Other countries in the region, including Thailand, Malaysia, Viet Nam and Indonesia, followed with emergency energy conservation measures.

Together, these developments uncover a growing tension between immediate energy needs and long-term energy transition goals, raising questions about the direction of the region’s energy transition.

Why is the Strait of Hormuz a critical oil transit chokepoint for Asia?

Around 80% of the crude oil that passes through the Strait of Hormuz is destined for Asian markets, with China, India and Japan being the main importers. For ASEAN alone, 55% of crude oil imports originate from the Middle East, leaving up to 28% of the region's final energy consumption at risk of direct disruption. This concentration has created a direct shock to refiners, utilities and industrial sectors across the region. For net energy importers, such as the Philippines and Thailand, higher oil prices feed directly through into electricity costs, raising expenses across manufacturing, transport and households.

It has also had a major economic impact: fuel price spikes can translate to power outages, production slowdowns and household income squeezes within weeks. The result is an energy shock that is showing up in electricity bills, fuel queues and straining government budgets across the region. At the regional level, importing oil and gas at current prices is adding $3.36 billion per month to ASEAN's import bill, a 3.4% increase above 2026 budget expectations.

How is the current crisis creating critical vulnerabilities for Asia?

Asian markets are also the main destination of Qatari and UAE gas exports. In 2025, almost 90% of the total gas volumes exported via the Strait of Hormuz were destined for the Asian market, while the share for Europe was just over 10%. This exposure is amplified by limited alternative supply routes – in contrast to Europe, which diversified its gas import infrastructure following Russia’s invasion of Ukraine in 2022.

Bangladesh, Pakistan and India imported almost two-thirds of their LNG through the Strait in 2025, making them particularly vulnerable to any disruption in transit flows. Across ASEAN, around 17% of natural gas supply comes from the Middle East, translating to a 3% disruption in consumption, a figure that, while more contained than the oil shock, still carries significant consequences for power generation and industrial activity. In India, the exposure runs across both LNG – which powers grids and industry – and LPG, the bottled gas on which over 330 million households in India depend for cooking. With public-sector oil companies now racing to lock in 2.2 million tonnes of annual LPG supply from the United States, a crisis born in the Persian Gulf is quietly redrawing the map of India's long-term energy partnerships.

Are policymakers prioritizing short-term protection over long-term transition?

Geopolitical disruptions to fossil fuel supply chains produce a dual effect: reinforcing the strategic case for diversifying energy systems and accelerating domestic renewables, while, at the same time, increasing short-term reliance on fossil fuels. Rising political pressure to protect consumers is driving a resurgence in fossil fuel subsidies and reducing fiscal space for clean energy investment. Broad measures, such as fuel subsidies, tax reductions and price caps, can ease inflation temporarily, but they are fiscally costly, often regressive in distribution and difficult to phase out once implemented. Malaysia's monthly fuel subsidy bill, for example, has surged fivefold since the crisis began. The risk is not a short-term emissions bump, but the fact that emergency measures can become permanent fixtures, crowding out the very investments needed to prevent the next crisis.

Governments across Asia are combining price controls with supply-side interventions to manage the shock. In South Korea, authorities have imposed fuel price caps, extended fuel tax cuts and lifted restrictions on coal-fired generation. India has directed coal plants to operate at maximum capacity, leveraging domestic reserves to stabilize electricity supply. Bangladesh, Thailand and Viet Nam have also increased coal outputs as energy security concerns mount. Across the region, some countries have introduced four-day working weeks for civil servants and raised office temperature limits to curb electricity demand – measures that speak to the breadth and urgency of the supply squeeze.

The pattern is consistent: reach for what is available, affordable and controllable. Yet not all countries are equally exposed. Viet Nam's rapid expansion of solar generation in recent years has provided a meaningful buffer, illustrating that the countries that moved earliest on renewables are proving most resilient. Similarly, China appears to be somewhat shielded from Middle East conflict-driven price shocks by its significant energy reserves, diversified energy supply and rapidly expanding renewable energy sector, which together reduce its dependence on Middle Eastern oil. This lesson will not be lost on policymakers.

Across ASEAN, analysis suggests that replacing planned gas capacity with solar and storage solutions could save the region up to $4 billion by 2030 – a figure that takes on new significance when set against spiralling fossil fuel import bills.

How do recent disruptions in oil markets reinforce the case for clean fuels?

Clean fuels can enhance resilience to geopolitical shocks when they are produced from domestic resources, such as renewable electricity or local biogenetic feedstocks and residues. This is prompting governments across Asia and the EU to reassess biofuel blending mandates and broader clean-fuel strategies through an energy-security lens. In China, for instance, the top energy regulator has pledged to accelerate the development of its hydrogen industry and leverage cheaper inputs, such as homegrown wind and solar.

While infrastructure constraints remain, sustained volatility has historically accelerated structural shifts by mobilizing policy and investment. Continued instability could, therefore, reshape fuel economics and trade flows, strengthening the case for clean fuels, as explored in the World Economic Forum’s Future of Clean Fuels initiative. Analysis from the recently published Fuelling the Future Whitepaper shows that biofuels have already reduced transport fuel import dependence by 5–15% in several importing countries, illustrating their capacity to buffer external shocks.

The forces at play across Asia, including geopolitical exposure, fossil-fuel dependency and the pull of short-term fixes, are precisely what the forthcoming 2026 Energy Transition Index (ETI) captures in detail. The ETI offers a timely framework for understanding how countries are balancing security, affordability and sustainability and where the most ground remains to be covered.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

Middle East and North Africa

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Energy TransitionSee all

Ayla Majid

July 28, 2026