Which countries are ahead in the global autonomous vehicle race?

Personal vehicles are the largest autonomous vehicle market segment by volume. Image: REUTERS/Mike Blake/File Photo

- The US government recently announced proposals aimed at speeding up the development and deployment of autonomous vehicles.

- Are self-driving vehicles ready to take to the road?

- A new World Economic Forum white paper looks at the readiness of personal vehicles, robotaxis and autonomous trucks through the next decade.

The speed at which self-driving vehicles are likely to be rolled out in the US and UK has recently been announced by both governments. Last month, the US administration said it planned to speed up the rollout and use of self-driving vehicles. The proposals would see certain self-driving vehicles exempted from some safety requirements - for example, rearview mirrors - and changes to the rules around reporting of accidents and crashes.

It comes as the UK government pushes back the date it expects to approve fully self-driving cars from 2026 to the second half of 2027.

But what exactly are autonomous vehicles, which countries are leading the way – and what does the future hold?

What are autonomous vehicles?

The US National Highway Traffic Safety Administration (NHTSA) uses the term ‘automated driving systems’ when referring to types of vehicles where a traditional driver would no longer be required. These types of vehicles are also often referred to as automated vehicles, the NHTSA explains.

It adds that in following industry standards they don’t use the term ‘self-driving’ when discussing higher levels of automation. “This describes a vehicle's state of operation, but not necessarily its capabilities,” it explains.

Automation is, of course, a spectrum and as technology and regulations evolve, what’s available to consumers will also evolve. A recent World Economic Forum white paper, produced in collaboration with Boston Consulting Group, defines six levels of advanced driver assistance (ADAS) and autonomous driving (AD) systems, with only the highest two considered ‘autonomous’ within that framework.

Vehicles most likely to become autonomous

The white paper, Autonomous Vehicles: Timeline and Roadmap Ahead, identifies three key use cases for the years ahead: personal vehicles; robotaxis and roboshuttles; and autonomous trucks.

The authors explore the likely next stages of the three use cases’ development and evolution. Importantly, across the board, they stress that technological, regulatory and economic challenges mean adoption is set to be more gradual than was previously thought.

Personal vehicles

Personal vehicles are the largest autonomous vehicle market segment by volume. However, automation is set to be an incremental evolution rather than a revolution, finds the white paper.

Looking at the levels outlined in the graphic above, personal vehicles are likely to benefit from advanced assistance features, rather than full autonomy. Come 2030, technologies at the L2 and L2+ level are likely to be the most dominant in new cars.

“Drivers of most new cars will still be required to keep their hands on the steering wheel and their eyes on the road long after 2035,” the authors write. So, no kicking back in the back seat just yet, unfortunately.

The key reasons for this? Cost, regulation and market availability. Reaching L4 autonomy “remains significantly constrained by both technical and regulatory barriers”.

Robotaxis and roboshuttles

As a use case, these have already clocked some mileage, with deployments underway in a number of US and Chinese cities.

That’s not to say their further deployment isn’t without many of the same challenges as personal vehicles, as well as city-specific regulatory differences, complex operational requirements and significant investment needs.

Come 2035, the white paper expects fleets of robotaxis to operate at scale in 40 to 80 cities. China and the US are expected to dominate the rollout in cities, with Europe and the Middle East also emerging opportunities.

How is the World Economic Forum promoting sustainable and inclusive mobility systems?

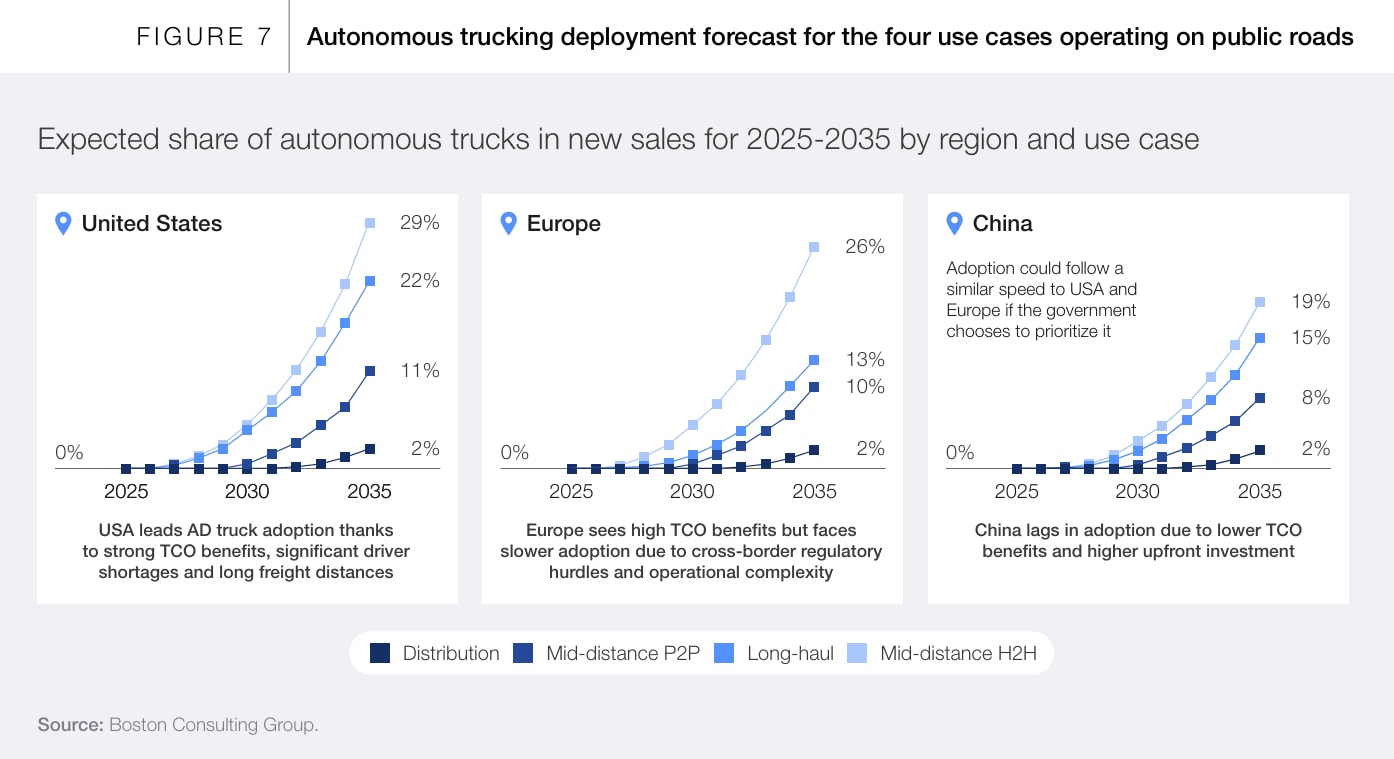

Autonomous trucks

Autonomous trucks are set to “transform logistics”, write the paper’s authors. Their development is already well underway, with testing and early commercial use in the US and China in particular.

There’s a significant economic case for them, driven by efficiency gains from 24/7 operations, tackling driver shortages and lower total cost of ownership. While deployment is set to vary based on specific use case, for mid-distance hub-to-hub routes, sales of new trucks in the US are expected to make up nearly 30% by 2035. Fixed highway routes enabling automated driving are key to this on these routes.

Once again, the US and Europe are set to be leading adopters, although the report cautions that a pan-European regulatory approach will be critical if the continent is to take full advantage.

The road ahead

As the data suggests, some key markets are set to dominate deployment in the years ahead, focused on the US, China and Europe. Equally, while all the hype might have been about self-driving cars, it is now the widespread use of robotaxis/shuttles and autonomous trucks that is closer to reality.

The white paper identifies five key dimensions that will influence these forecasts and the potential deployment and uptake of these vehicles:

- Consumer trust and interest

- Projected ADAS/AD prices and consumers’ willingness to pay

- Technological obstacles and the timeframe for overcoming them

- Current regulatory status and anticipated regulatory developments

- Ecosystem developments to support scaling.

If the potential of autonomous driving is to be met, coordination will be needed across multiple partners, from regulators to suppliers. “Autonomy is not a short-term race but a long-term transformation requiring sustained commitment and cross-sectoral cooperation,” the paper concludes.

Don't miss any update on this topic

Create a free account and access your personalized content collection with our latest publications and analyses.

License and Republishing

World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Stay up to date:

United States

Related topics:

Forum Stories newsletter

Bringing you weekly curated insights and analysis on the global issues that matter.

More on Energy TransitionSee all

Naoko Tochibayashi

June 12, 2026